tadamichi

I last wrote about the iShares 0-5 Years Investment Grade Corporate Bond ETF (NASDAQ:NASDAQ:SLQD) late last year. In that article, I argued that the fund’s safe holdings and good forward yield make it a reasonable investment opportunity, but only appropriate for more conservative investors. The fund has returned 8.3% since, outperforming relative to most high-quality bonds and fixed-income securities including t-bills. Returns were in-line with expectations, although nothing extraordinary.

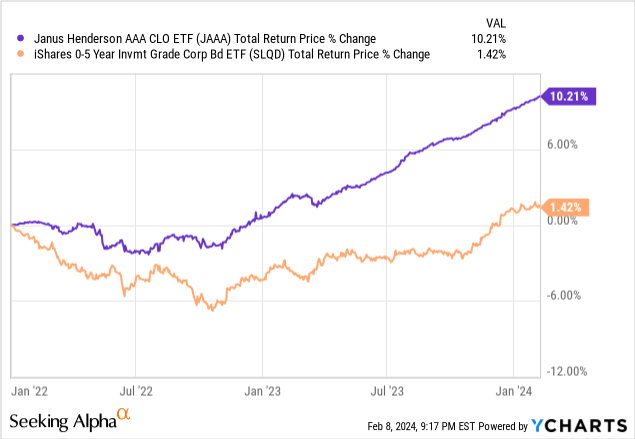

Right now, SLQD offers investors diversified exposure to high-quality, short-term bonds, a low 3.1% TTM yield, but a respectable 5.0% forward yield. Although SLQD remains a reasonably good investment opportunity for more conservative investors, I think there are stronger choices out there. Of these, the Janus Henderson AAA CLO ETF (JAAA) stands out.

JAAA offers investors diversified exposure to high-quality CLO tranches, has somewhat lower risk and volatility than SLQD and yields a bit more, with a 5.8% TTM yield and a 6.8% forward yield. SLQD is a fine choice, but JAAA seems broadly better.

SLQD – Basics

- Investment Manager: BlackRock

- Underlying Index: Markit iBoxx USD Liquid Investment Grade 0-5 Index

- Dividend Yield: 3.07%

- Expense Ratio: 0.06%

- Total Returns CAGR 10Y: 1.93%

SLQD – Overview and Analysis

Index and Portfolio

SLQD is a short-term investment-grade corporate bond index ETF, tracking the Markit iBoxx USD Liquid Investment Grade 0-5 Index. It is a simple index, including all dollar-denominated bonds with a maturity of at least five years. As with most indexes, applicable securities must also meet a basic set of inclusion criteria. There are issuer and security caps, meant to ensure a modicum of diversification.

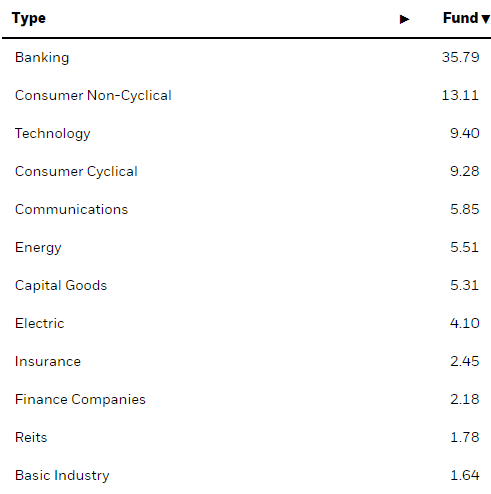

SLQD provides investors with diversified exposure to investment-grade corporate bonds, with investments in almost 2,500 securities from most relevant industries. It does not provide exposure to other high-quality sub-asset classes like MBS or t-bills, however.

SLQD

Credit Quality

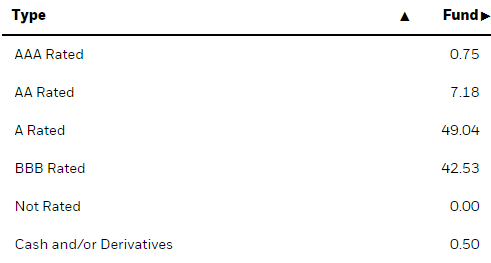

SLQD’s portfolio is comprised of reasonably safe, low-risk securities with strong credit ratings. Fund holdings have an average credit rating of A, indicative of issuers with solid financials, balance sheets, and current capacity to fulfill their financial obligations. Default rates are overwhelmingly low, even during adverse economic scenarios.

SLQD

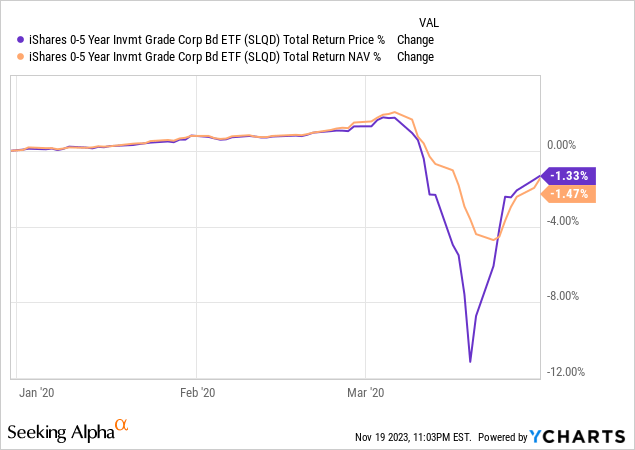

As credit quality is high, the fund tends to experience comparatively low losses during downturns and recessions. SLQD briefly suffered double-digit losses during early 2020, the onset of the coronavirus pandemic, significantly underperforming expectations. Losses were almost entirely due to widening discounts, with a 4.0% NAV drawdown, and 1.5% NAV losses during 1Q2020. ETFs rarely trade at significant discounts, although some did during the pandemic, a period of unprecedented market stress and volatility.

Data by YCharts

SLQD’s high-quality holdings will almost certainly suffer very low losses during any future downturn or recession. Discounts could always widen, as was the case in 1Q2020, but this is a genuinely rare occurrence for an ETF, and I don’t expect it to happen again.

SLQD’s credit quality is quite good, but lower than that of some of its peers. As mentioned previously, JAAA seems like a particularly strong fund in this space, with a portfolio focusing on AAA-rated CLO tranches. Credit quality is a bit higher, although both are comparatively safe, investment-grade funds.

JAAA

Interest Rate Risk and Duration

SLQD focuses on short-term bonds, with an average maturity of 2.3 years, duration of 2.1 years. Both figures are low on an absolute basis, and compared to most bonds and bond sub-asset classes.

Fund Filings – Chart by Author

Short-term bonds tends to outperform during periods of rising interest rates for two key reasons.

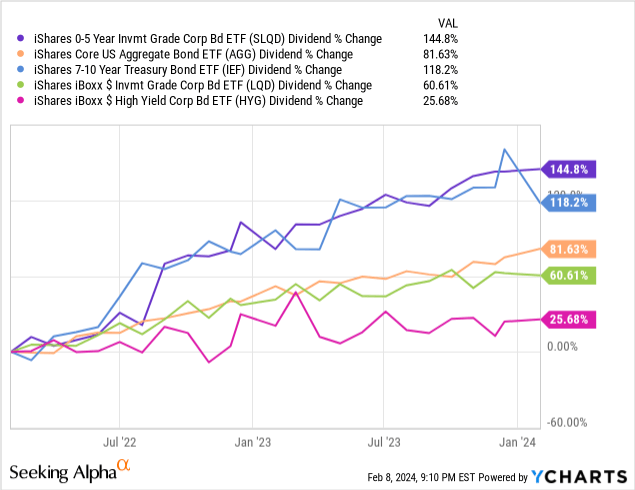

First, short-term bonds mature in a short amount of time, allowing investors to quickly replace their older, lower-yielding bonds with newer, higher-yielding alternatives when rates increase. Said process benefits bond funds too, and should lead to significant dividend growth for the same. SLQD’s dividends have more than doubled since early 2022, when the Fed started to hike, outpacing most of its peers.

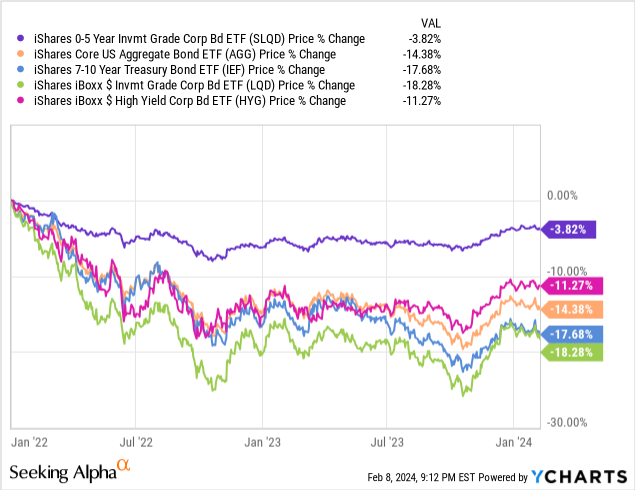

Second, and due to the above, short-term bonds tend to see much lower capital losses when interest rates decrease. As an example, SLQD’s share price is down 3.8% since early 2022, with most other bonds and bond sub-asset classes seeing much higher double-digit declines.

Low interest rate risk decreases portfolio risk and volatility and is an important benefit for SLQD and its shareholders.

On the other hand, low interest rate risk means lower gains and underperformance when rates decrease. Excluding the pandemic, rates last decreased during 2019, during which SLQD underperformed, as expected.

Data by YCharts

Considering the above, SLQD should underperform if rates were to significantly decrease in the near future. Right now, the market is pricing-in several rate cuts already, so these might not necessarily lead to underperformance. In other words, only fast, significant, higher-than-expected rate cuts would lead SLQD to underperform, in my opinion at least.

JAAA has even lower interest rate risk than SLQD, with an effective duration of 0.05 years, effectively equivalent to zero.

JAAA

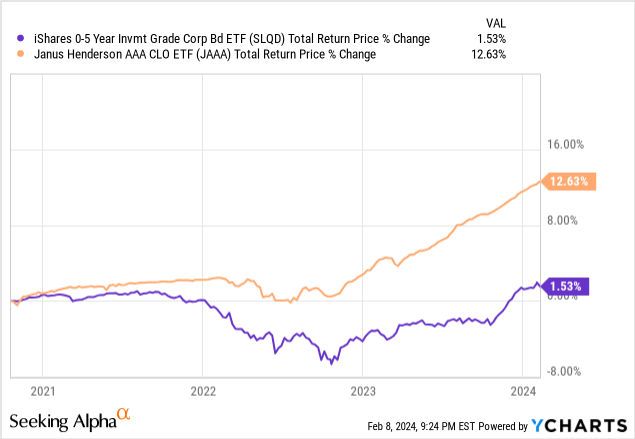

Due to the above, JAAA tends to outperform SLQD when rates decrease, as has been the case since early 2020.

Dividend Analysis

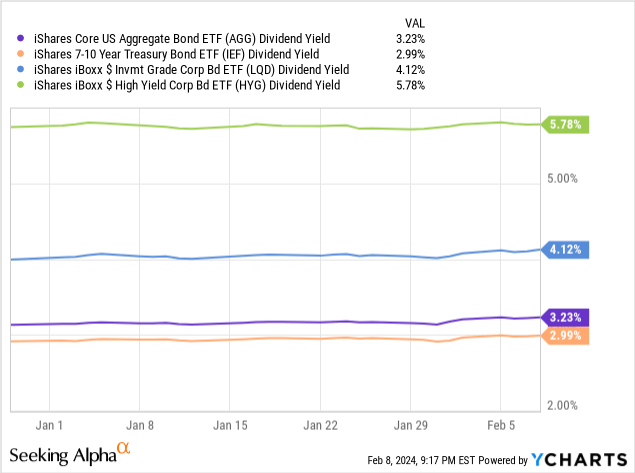

SLQD currently sports a 3.1% dividend yield, quite low on an absolute basis, and somewhere between average and below-average for a bond index ETF.

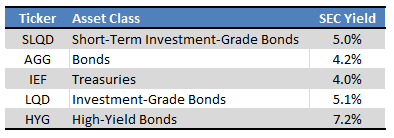

Although the figures above are accurate, they do not fully take into account recent Federal Reserve hikes. These have caused rates to spike across fixed-income asset classes, including the short-term investment-grade bonds held by SLQD. SEC yields are more forward-looking, standardized yield metrics, and, in my opinion, more indicative of the dividends that investors should expect moving forward. SQLD sports a respectable 5.0% SEC yield, somewhat higher than average.

Fund Filings – Table by Author

Barring any significant interest rate movement, SLQD’s yield should rise to 5.8% in the next two years or so. Fund dividends have risen by a lot already, although growth has been somewhat lower than I expected for a short-term bond fund. It has been two years since the Fed started to hike, and dividends have only like a third of the way, from 1.5% in early 2022, to 3.1% as of today. SLQD has an average maturity of 2.3 years, so dividend growth seems lower than expected. In any case, dividends have risen, and I expect further growth.

Seeking Alpha

SLQD’s dividends compare unfavorably to those of JAAA. JAAA has a much higher 5.8% dividend yield, 6.8% SEC yield, and has seen

Seeking Alpha

Performance Track-Record

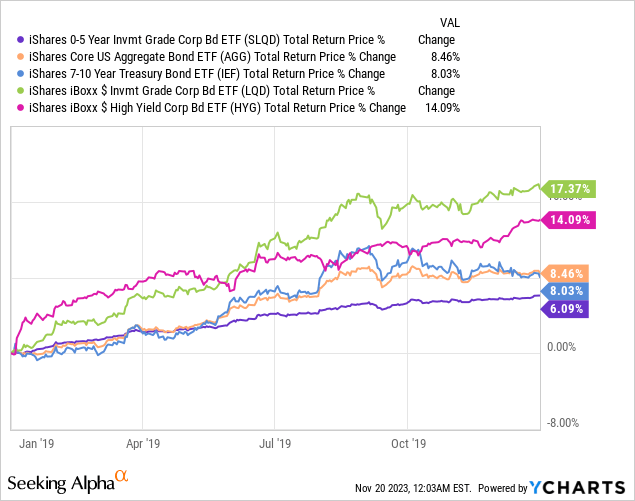

SLQD’s overall performance track-record is reasonably good, although nothing extraordinary. Recent returns are good, as rates have (somewhat) stabilized at a high level. The fund has outperformed recently, due to its low interest rate risk. Long-term returns are quite weak, however, as rates were much lower in the past.

Seeking Alpha – Table by Author

On a more negative note, the fund has moderately underperformed relative to JAAA since inception, and for most relevant time periods.

Which brings me to my next point.

Quick JAAA Comparison

I’ve been comparing SLQD to JAAA throughout this article, and it seems quite clear that JAAA is stronger in most areas, weaker in few.

JAAA has somewhat lower credit and interest rate risk, but a higher yield and stronger performance track-record. Risk-adjusted returns seem much stronger too. SLQD’s only advantage is its potential outperformance during a period of declining interest rates. Bear in mind, some rate cuts are priced-in already, and SLQD is a short-term bond fund, so don’t expect significant capital gains from lower rates. Dovish investors might prefer SLQD over JAAA, but for these investors going long-term bonds is a much better choice.

Overall, JAAA seems stronger than SLQD.

Conclusion

SLQD is an index ETF investing in short-term investment grade bonds. Although there is nothing inherently wrong with SLQD, it compares unfavorably to JAAA on most key metrics. As such, I would focus on JAAA over SLQD.