Ulrike Schmitt-Hartmann

Introduction

Many readers and investors here on Seeking Alpha are probably experienced enough to remain cautious when they see a company paying large dividends at a cheap valuation. But what about those that don’t know? I always think of that when constructing my articles. I was once that guy that chased yields and only looked at the surface and ignored the why. I think about those investors, but maybe it’s the fact that I did 21 years in the military and in my job field I was used to taking care of younger sailors.

Those sailors typically ranged from 18 – 20 years old. And I often played more than their boss; I was their brother, financial advisor, and even a father figure for some. Those reading this who spent time in the military likely know what I’m talking about. And in this article I discuss that although Saratoga Investment Corp (NYSE:SAR) pays a large dividend, investors may want to proceed with caution.

Company Profile

For those unfamiliar with Saratoga Investment Corp, they are a business development company that provides capital to middle-market companies in the U.S. For starters, the BDC is externally-managed by Saratoga Investment Advisors and at the end of their latest Q3 had $1.11 billion in Assets Under Management. Most of their investments were located in the Southeastern part of the United States with 27.7%. The Midwest makes up the second largest portion at 22.1%. Their portfolio is invested in a wide array of industries at 43 with the top two being Healthcare Software & IT Services.

SAR investor presentation

Dividend Coverage

As a collector of dividends, SAR immediately jumped out at me for their near 13% dividend yield. But as a long-term buy-and-hold investor, I always remain cautious. For short-term investors who prefer to capture dividends, Saratoga Investment Corp may be the company you want to buy currently. Moreover, the BDC recently increased the dividend by 1% to $0.73. This marked the 5th increase they conducted in roughly the past year, raising it from $0.69 in the first quarter of 2023.

And during their FY ’24 Q3 earnings this past January, this was well-covered with net investment income. The BDC brought in NII of $1.01 missing analysts’ estimates by $0.03. But they managed to beat on total investment income by roughly a half a million. TII came in at $36.34 million for the quarter. And while total investment income grew quarter-over-quarter from $35.51 million, net investment income declined slightly from $1.08. However, this still more than covered the quarterly dividend of $0.73.

And despite earnings for the next quarter expected to decline by analysts’ estimates to $0.96 when the BDC reports next month, this still covers the current dividend. This would represent a year-over-year decline from $0.98 in Q4 ’23. I expect NII in a range of $0.96 – $1.00 for the BDC.

Seeking Alpha

Dilution

Now that we’ve talked about their dividend coverage and the reason why most investors are interested in the BDC in the first place, let’s get into reasons to be cautious. The company had been repurchasing shares in prior quarters but in the latest Q3 did not purchase any additional shares. In fact, they actually diluted shareholders and this negatively impacted their NII, a reason for the decline. This resulted in a $0.07 dilution from the increased weighted average shares outstanding from recent ATM equity issuances.

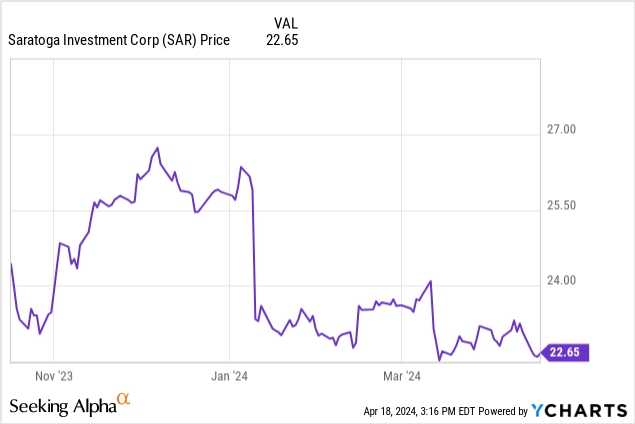

At the end of the quarter shares outstanding increased to 13.1 million, up from 12.2 million in the prior quarter. And although most know BDCs issue shares to raise capital, similarly to REITs, this impacts the company’s financials and NAV growth. In turn, this could also negatively impact the share price. You can see from the chart SAR is down from roughly $27 in the past 6 months to the current price of $22.64 at the time of writing.

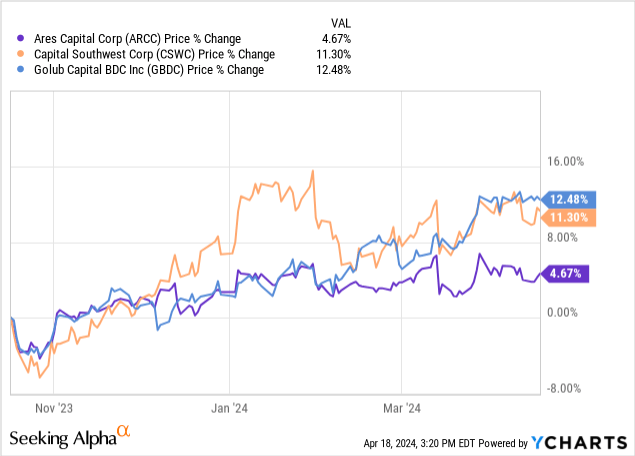

This is in comparison to other BDC peers who’ve seen their share prices appreciate in the past 6 months. One reason for the drop is the BDC’s leverage.

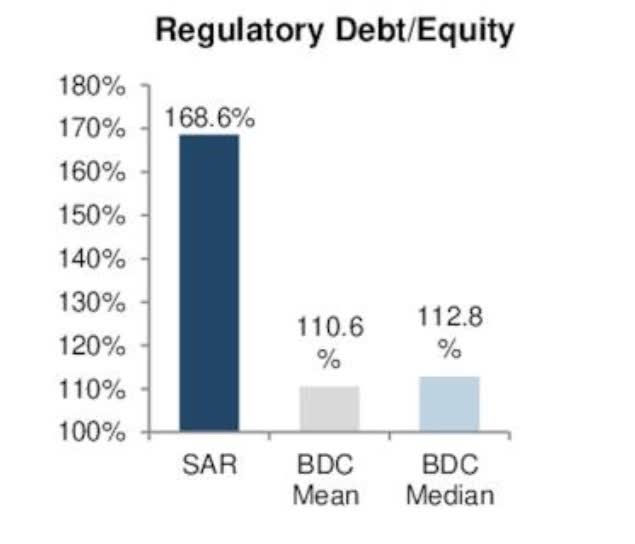

Currently, Saratoga has more debt than any peer in the sector with a debt-to-equity ratio well above the sector median. And with interest rates likely to remain higher for longer, this will only impact the BDC negatively. Right now is the time for companies to be deleveraging and improving their balance sheets. This not only provides their management with financial flexibility, but it gives investors a warm and fuzzy about their quality as well.

SAR investor presentation

Portfolio Quality

This also raises questions about their portfolio quality. One thing I liked is that they are defensively-positioned with 86% of their loans in first-lien. And this increased from 82% year-over-year. But non-accruals also rose over the same period. At quarter’s end SAR had 3 companies on non-accrual status, up from 1 in Q3 ’23. These accounted for 2.6% at fair value and 6% at cost. This is in comparison to peers Ares Capital (ARCC) who saw their non-accruals decline year-over-year from 1.7% to 1.3%.

Golub Capital (GBDC), another externally-managed BDC managed to decrease theirs for four straight quarters to just 1.1%. These accounted for 1.7% & 1.1% of cost and fair value. So, while peers have been reducing non-accruals year-over-year, Saratoga Investment Corp saw theirs increase. And if interest rates stay higher for longer, this will likely continue to rise further in the coming quarters. This along with their leverage is something I’ll be keeping a close eye on in the upcoming quarter next month.

Discount To NAV

Along with a spike in non-accruals, SAR also saw their NAV decline for four straight quarters. At the end of fiscal year ’23 SAR’s NAV was $29.18, representing a 6% decline. And seeing by the previous chart the share price has followed suite. At the current price, Saratoga trades at more than a 17% discount.

This is higher than the average discount of roughly 9%, so the BDC looks attractive currently. Both ARCC and GBDC trade at premiums of roughly 6% & 10% above their NAVs. But for reasons discussed in this article, SAR’s discount is warranted. And the share price could continue to fall if the BDC disappoints on upcoming earnings next month. Most analysts rate them a hold currently and I have to say I agree.

Author creation

Bottom Line

Although Saratoga Investment Corp offers a nice double-digit yield that’s currently well-covered by their net investment income, the BDC has some things they need to get control of in the coming quarters like their non-accruals. And with interest rates likely to remain higher for longer, this could place further downward pressure on their borrowers, causing this to rise further.

If so, their share price will likely decline as investors remain skeptical of their portfolio quality. Despite raising their dividend for 5 straight quarters, SAR remains a speculative investment for buy-and-hold investors in my opinion. Until I see some healthy NAV growth and a decline in non-accruals, I rate Saratoga Investment Corp a hold.