Qin PinLi/iStock via Getty Images

Dear readers/followers,

Last time around when I wrote about Simon Property Group (NYSE:SPG) stock, I considered the company a “BUY”. I’ve also invested in the company and hold a stake for over a year now, with a very good annualized RoR.

Now, however, the company has reached a bit of a “level” where we will want to see if there’s further upside to be had. And as you can tell from the title here, I consider that not to be the case, necessarily. In this article, we’ll look at what sort of returns you can expect for the next few years if the valuations hold and are not outperformed.

At $150/share or above, SPG trades at a valuation of above 13.5x P/AFFO. This might not sound like much for an A-rated business – and from one perspective, it’s not – but when you look at what the company is expecting, you start to see why it might not outperform.

Let’s look at the up- and the downside of Simon Property Group as of 2024 and up until 2026E as things look today.

Simon Property Group – What to like and dislike about the company at this time

This company requires little introduction – it’s one of the world’s companies most premiere and well-known mall REITS. Simon Property Group has been an integral part of my portfolio for several years, in fact since COVID-19 and since I bought Simon Property Group at below $80/share. My YoC for the original parts of my position is well over 8% at this point, and the RoR at this point, inclusive of dividends, is triple digits.

So how could I look at this company and say that I’m considering my position and looking to potentially divest here?

We’ve been very clear on the prospects we view for this REIT. There have been no fundamental signs of decline in this REIT even during COVID, that would justify the deepest troughs this company went through. In every consecutive 2023 quarter, metrics and results have steadily improved or at the very least not declined significantly, despite the inputs and trends that some contributors and analysts point to. (Source: Simon Property IR)

4Q23 was only the latest in a long line of good results. In fact, the results were beyond merely good in some ways. 4Q23 also coincided with the company’s 30th anniversary, and the results were suitably excellent.

By this I mean that SPG generated a record-level FFO of $4.7B, executed on another 18M sqft of leases, delivered over 10 projects, and completed several major financing transactions, reinforcing the company’s already-excellent and A-rated balance sheet.

On a full-year basis, the company grew its results/net income on a YoY basis, almost up 50 cents per share. FFO was up more than 50 cents on that per share basis, with NOI increasing up to close to 5% YoY. SPG continued at, for a mall REIT, very attractive levels of occupancy, increasing almost a full percent to 94.9% – a superb level really by any measure for this sort of company. (Source: Simon Property IR)

Additionally, they did not do this by cutting rents. The company’s base minimum rent was $56.82, compared to $55.13, marking a 3.1% increase. Nothing close to inflation, but still a solid level as I see it.

And perhaps more importantly, to investors like myself, the company increased its common share dividend yet again, an 8.3% increase of $1.95 for the first quarter.

To be clear, those are amazing results, and Simon has been an amazing ride. If you look at where many of us at iREIT invested, when the company was beaten down (I actually took some profits in 2021, as I have said in previous articles, and bought more when the company dropped), we’re now moving back up to a rather interesting level of valuation.

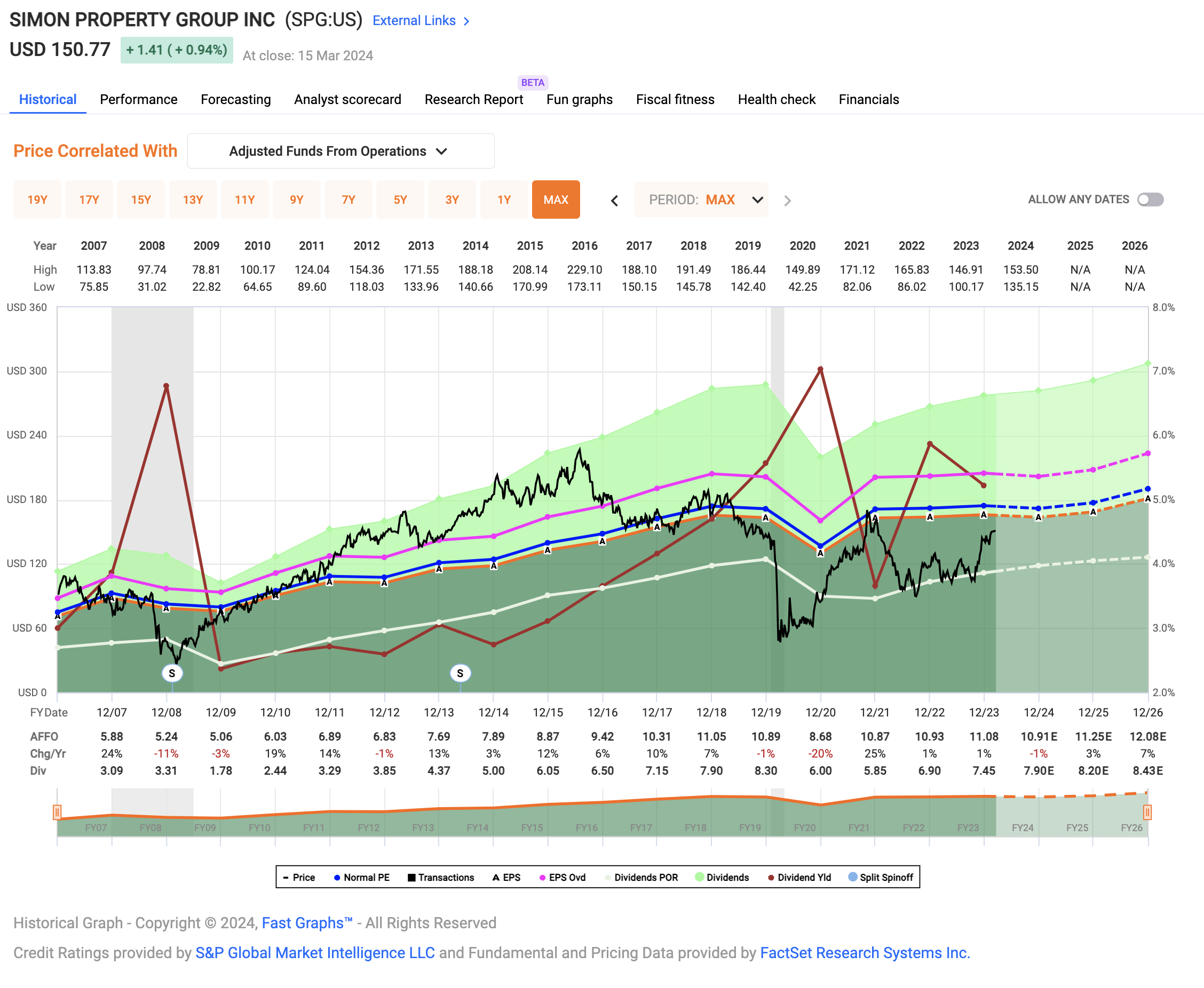

Simon Property Group Valuation (F.A.S.T graphs)

As always, it highlights the crucial lessons of value – buying what you buy at the right value to position yourself for conservative growth. In this case, that is something I have done. As you can see though, the company is moving back to levels of valuation which would seem close to the 20-year average we’re seeing here.

Such moves are always a great time to revisit your stake and make sure that it does in fact still meet your investment requirements.

It’s my personal stance that no investment you hold should be “sacred”. Every investment should have an entry and an exit – not just an entry. Otherwise, you’ll repeat the mistakes some investors make in holding their stakes through a bubble and not realizing profits. This of course needs to be weighted against wanting to keep your “winners”.

My approach to this is valuation, and while I cannot claim success in every investment in this way, Simon Property Group is a very good example where this has worked out extremely well for me.

I also state clearly in this article, that while I do consider Simon Property Group an extremely attractive business with a great business model and excellent fundamentals (and superb management for that matter), I do consider the company here to start reaching levels where your targets should be “checked”.

Why do I think that this is the case, exactly?

Because despite not believing in magical share price levels, I do believe that crossing the $150/share mark, which Simon has very recently done, is a very important milestone – both for prospective investors and for already-existing owners of the company’s shares.

The current dividend yield for the company comes to 5.1%. That is no longer market beating – most of the qualitative triple-nets yield more and trade at significantly lower multiples than SPG does (more on that in a bit). Furthermore, I also believe the triple-net model, depending on the specifics of the asset portfolio, to be safer and more qualitative than straight Retail/Mall REIT space – and despite SPG’s fortress-like characteristics, this also includes Simon Property Group.

My interest is growing my capital at above-market rates with above-market safety where this is possible. I won’t hide the fact that I sometimes take what I would consider far more elevated risks (15-18% of my portfolio), but Lion’s share of my portfolio is aimed at extremely conservative and qualitative businesses I have owned for years at this point.

Let’s look at what makes SPG a candidate that you should consider in a lot of ways here.

Simon Property Group – The valuation has crossed a threshold.

To be clear, I am in no way claiming that SPG is a “bad business” here. I wouldn’t be invested in it if that was the case. I am saying that at over 13.5x P/AFFO, the company is no longer as interesting to me, given that AFFO growth over the past 9-10 years has averaged less than 2% (Source: FactSet).

A company that grows only at 2% AFFO per year but trades at less than 5x P/AFFO with Simon Property Group’s fundamentals and yields, to me is an undeniable “BUY”. While this sounds outlandish, this is exactly where SPG traded during the worst of its trough.

That’s when I bought much of my current stake.

However, now the price has changed, and what was attractive at below $60/share is not attractive at above $150/share.

SPG is set to continue to grow – slightly. I don’t hold any fears that the company’s business model will somehow be invalidated by e-commerce, as some believe, or that the company will somehow see some catastrophic drop-off. I believe SPG’s management has navigated these waters to clearly prevent that.

At the same time, it cannot be hidden that the company going forward, is likely to grow far less.

How can I say this?

Because this is the company’s own estimate.

SPG is forecasting its 2024E FFO and net income to drop. Not by that much – but 1-3% in the low/high estimates as of the beginning of the year. This won’t affect the company’s attractive dividend, but it should affect the valuation we apply to the business.

So, what in layman’s terms, “is my problem”?

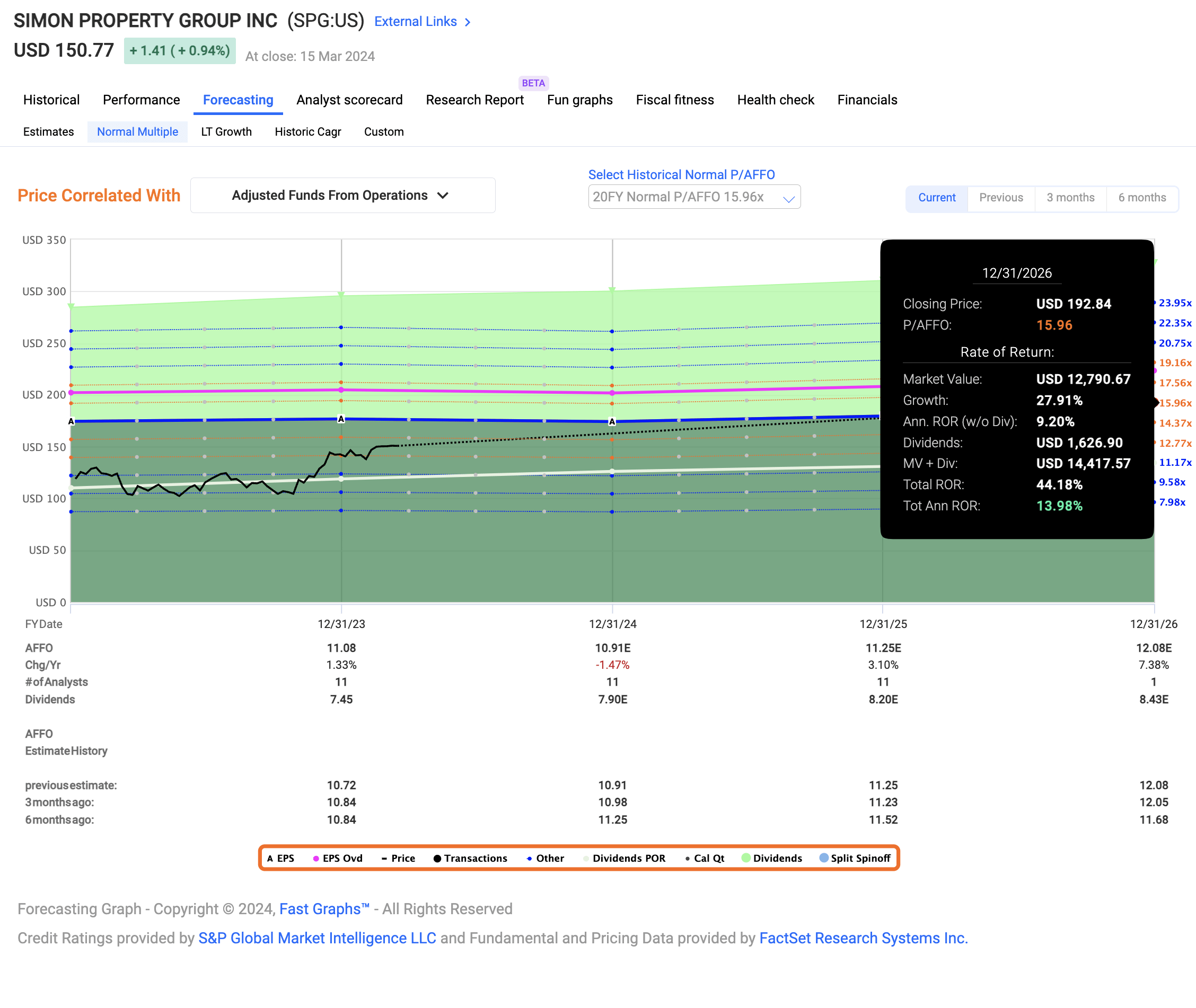

If we forecast SPG at a 20-year average, there is no problem. That average comes to almost 16 times adjusted funds from operations and if you believe that SPG should trade at such a multiple, the upside here is significant – still almost 15% per year inclusive of dividends, and that with A-rated safety. No issue, if that’s your estimate.

F.A.S.T Graphs SPG Upside (FactSet)

My issue is that this is an extremely bullish forecast, given that the company is unlikely to see the same sort of future AFFO growth that it saw during that period. In fact, if we average out the past 5-8 years, we instead get an FFO of 12-13.5x. That gives us an annualized RoR of less than 6% on the low side, with dividends, and around 8.3% annualized at the higher 13.5x P/AFFO point.

That’s not even double digits – and that includes not only the 5.17% dividend but also a 3.1% 2025E growth and a 2026E growth estimate of almost 7.5% – which I believe to be rather bullish as well.

You can see why I may be somewhat doubtful about, first of all, the company’s ability to reach higher based on these growth estimates, but even if they were, the attractiveness of those targets and estimates if they actually do.

As I see it, no matter how you slice it, this company is no longer, and not at this time, worth anywhere close to above $200/share. I would stick to my conservative PT of $130/share, say that the company should be considered a candidate for rotation at $150/share, and become a strong or very strong buy at below $110/share, or specifically in the double digits.

At this time though, I may actually go ahead and rotate more of my position in SPG. There are better alternatives for investing out there.

This is one of the few rating changes I publish here – but given the size of my SPG position, it’s an important one.

Thesis

- Simon Property Group is without a doubt one of the most premiere and attractive retail/mall REITS out there. My view is that the safety of SPG, combined with the excellent yield, which is higher than many other, less safe businesses, makes for a real upside conservative PT. I’m never as quick to shift my PTs as some analysts are. That is unless there is a very good reason for it.

- You cannot, I believe, equate today’s SPG to the SPG of pre-COVID. The growth rates and rental growth rates simply are no longer there. That means the company can be bought at above-average yields and reversal upsides, but you should avoid it, or at least be careful, at times when a flat growth estimate to a conservative valuation point to potential lower-than-average rates of return.

- As things stand now, I believe that the inflection point is at around $130/share. That means that below $130/share, I believe the company is “fair game”. But now the company is above $150/share, and at that level, I believe there is a real chance for market underperformance.

- For that reason, I elect to change my rating to “HOLD” here.

- I may even sell/rotate more of my SPG position in the coming week/s and apply that capital elsewhere.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

As things stand now, the company does not fulfill my cheapness or upside requirements. For that reason, it’s a “HOLD” here.