China’s calmest offshore credit market in years will be tested in coming months by maturities at major developers and ongoing weakness in the property market.

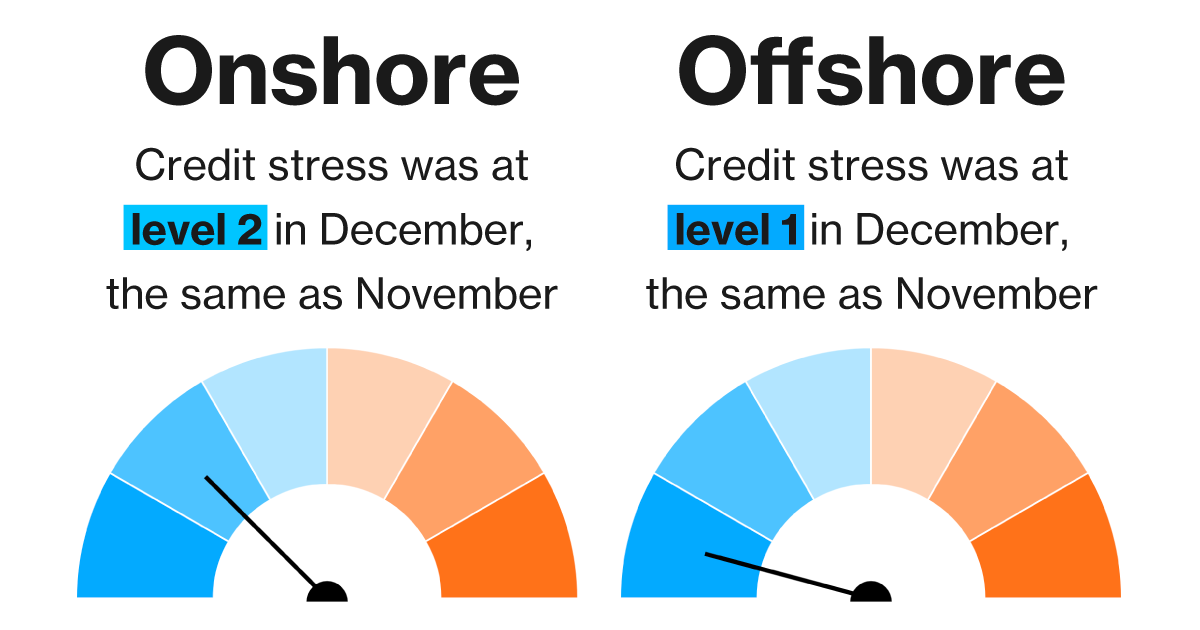

A gauge of credit stress in the nation’s offshore bond market held at 1 in December, according to Bloomberg’s China Credit Tracker, matching November’s reading which was the lowest since the series started in May 2021. A similar index for onshore credit stayed at 2.

The gauge indicates rising degrees of financial strain via a band from 1 to 6.

China’s major developers have a total of $10.5 billion in bonds coming due in the second quarter alone, according to data compiled by Bloomberg. That is up from $7.6 billion in the first three months of the year.

“The pressure spots appear to be in the second quarter,” HSBC Holdings Plc credit analysts Keith Chan and Cathy Cheng wrote in a research note last month. Among the companies to watch are the country’s 10th-largest developer Gemdale Properties and Investment Corp., which has 3.5 billion yuan ($488 million) of maturing bonds in May and June, they said.

Developer Sino-Ocean Group Holding Ltd. told some bondholders it plans to extend all its local yuan bonds outstanding, including pushing back maturities of four notes by up to 30 months, people involved in the private conversations told Bloomberg this week.

The real estate crisis may still have a long way to run. The value of new home sales among the 100 biggest developers slid 34.6% in December from a year earlier, larger than November’s 29.6% drop, data from China Real Estate Information Corp. showed last month.

“There’s a risk that the 2024 physical market could remain tepid due to supply from pre-owned apartments and subdued household income expectations,” said Chris Li, a credit analyst at BNP Paribas in Hong Kong. “If that happens, some private developers may be crowded out again.”

On the positive side, the authorities have stepped up measures to support the industry in recent months, including relaxing home-buying curbs in major cities and creating a draft list of struggling real estate developers eligible for bank support. More good news emerged this month when China Vanke Co. and Longfor Group Holdings Ltd. briefed investors about plans to repay maturing debt.

A Bloomberg index of Chinese junk dollar bonds, dominated by developers and excluding defaulted securities, is on course for a fifth month of gains, which would be the longest winning streak since August 2020.

Beijing, Guangdong Have the Most Local Defaulted Notes

Note: Map shows mainland China’s local note market. Source: Bloomberg

A number of recent state-guaranteed bond sales by private developers have also supported sentiment, namely Longfor, Seazen Group Ltd. and Radiance Holdings Group Co., the HSBC analysts wrote in their note.

Tracking Payment Deadlines

Monthly bond maturities for Chinese firms that face debt-repayment tests

Some investors meanwhile are starting to position for a potentially faster-than-expected rebound in the housing market. Loomis Sayles & Co.’s fund manager Matt Eagan, whose jointly-managed fund beat 97% of its peers last year, said the sector looks to have bottomed and investors who wait too long may miss out on the rebound.

“It’s bottomed here but it’s still got a long way to go to recover,” Eagan said in an interview last month. “Before it was easy to say: ‘I’m not even going to pay attention to it because it’s just a one-way bet down,’” but that’s no longer the case, he said.