Houston Chronicle/Hearst Newspapers via Getty Images/Hearst Newspapers via Getty Images

Homebuilder stocks have been among the top-performing names in the S&P 500 since the summer of 2022. The SPDR S&P Homebuilders ETF (XHB) has returned nearly 80% in the past 20 months while the iShares U.S. Home Construction ETF (ITB) has almost doubled in that stretch.

But with mortgage rates back above 7% given the most recent jump up in interest rates and with growing signs that the consumer is hitting the pause button, companies involved in the home construction business could face new headwinds as 2024 rolls on.

I have a hold rating on Lennar Corporation (NYSE:LEN) ahead of its March earnings date. I see the stock as reasonably valued today, perhaps a touch to the expensive side, but with flat EPS growth expected in 2024. What‘s more, technical momentum has taken a leg lower.

Homebuilder ETFs Soar, Sharply Outpacing the S&P 500

Stockcharts.com

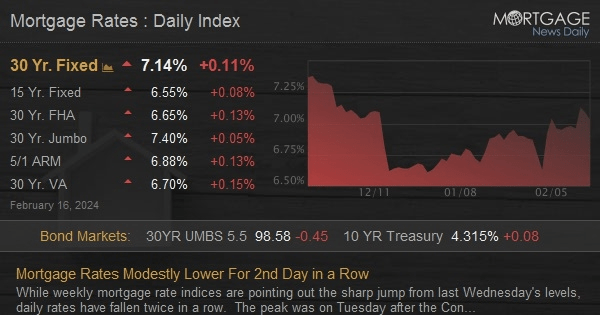

Mortgage Rates Jump to Fresh Highs Since Last November

Mortgage News Daily

According to Bank of America Global Research, Lennar is the second largest public homebuilder by closings in the US. LEN is positioned in 21 states in 49 markets targeting first-time, move-up, and active-adult buyers. Lennar reports its results under five distinct operating regions: East, Central, Texas, West, and Other. The company also owns a financial services business.

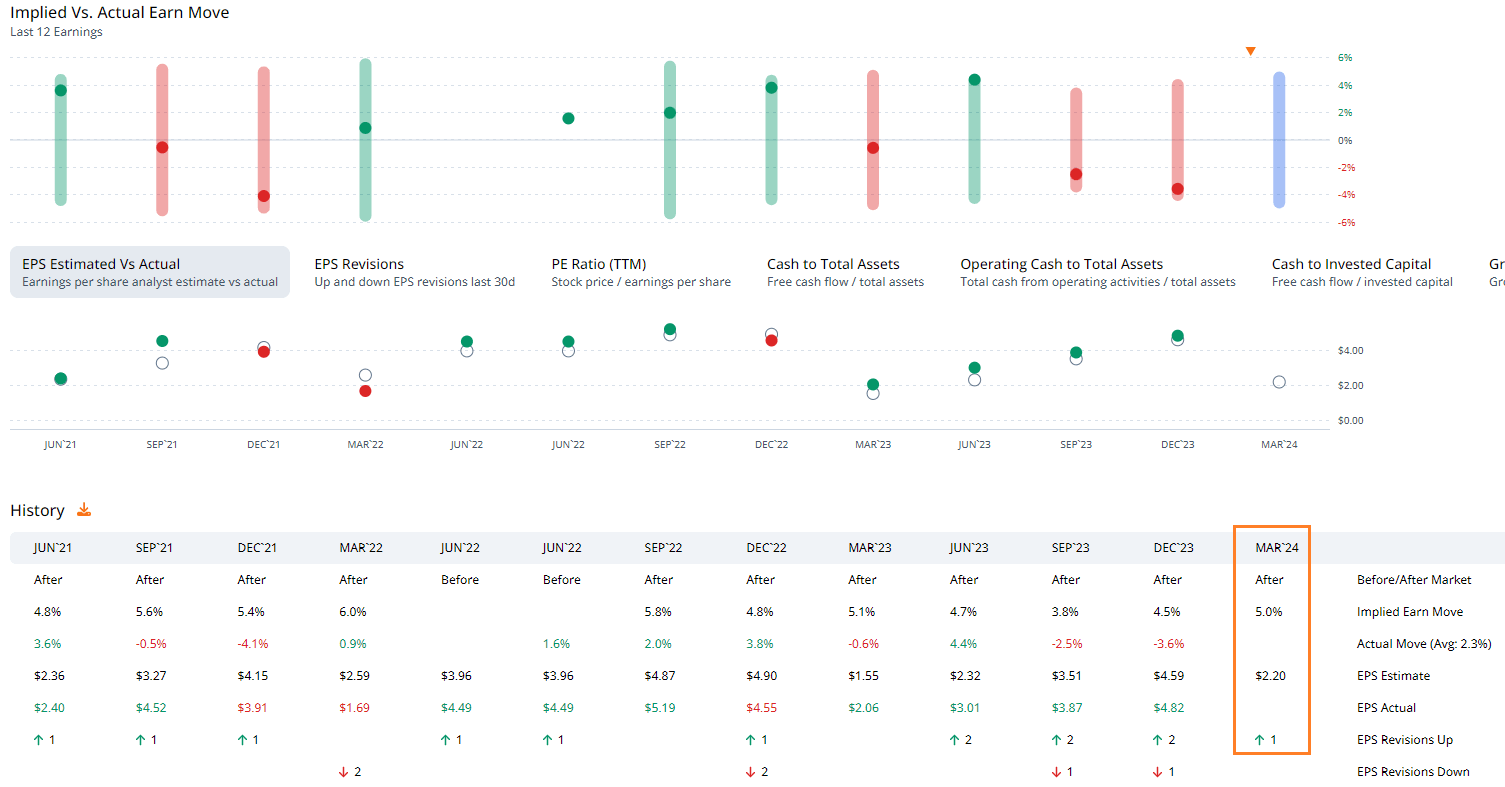

Lennar reports Q1 results in a few weeks, and the options market has priced in a sizable 5.0% earnings-related stock price swing when analyzing the at-the-money straddle expiring soonest after the reporting event. Analysts expect $2.21 of normalized EPS for the quarter that just ended, which would be a modest increase from $2.06 of operating per-share profits earned in the same period a year ago.

Despite higher mortgage rates last year, the firm’s dynamic pricing strategy helped to boost net orders by more than 30% by the end of 2024. Be sure to monitor gross margins and its average selling price trends in the upcoming report – its management team noted potential headwinds in its gross margin for the Q1 2024 period.

Lennar: A 5% Stock Price Swing Priced Into the Q1 2024 Report, Four Straight Bottom-Line Beats

ORATS

On valuation, analysts at BofA see earnings rising 7% this year and then accelerating into and through 2025. Operating EPS may then top $17 by 2026. But Seeking Alpha’s consensus earnings numbers are less sanguine; just $14 of per-share profits are expected this year but then a strong low-double-digit profitability bounce back is forecast for the out year while Lennar likely grows its top line in the mid-single digits.

With a healthy buyback program in place, Lennar raised its dividend payout from $1.50 annually to $2 earlier this year while the company’s free cash flow yield may dip from the currently high 11% mark.

Lennar: Earnings, Valuation, Dividend Yield, Free Cash Flow Forecasts

BofA Global Research

If we assume non-GAAP EPS of $14.50 over the next 12 months (about the current consensus) and apply a 10 earnings multiple (between its 5-year average and the sector median), then shares should trade near $145. Lennar also trades at a 20% premium to its 5-year historical price-to-book ratio, a decent valuation gauge for homebuilders.

Lennar Trades at a Valuation Premium to Most 5-Year Averages

Seeking Alpha

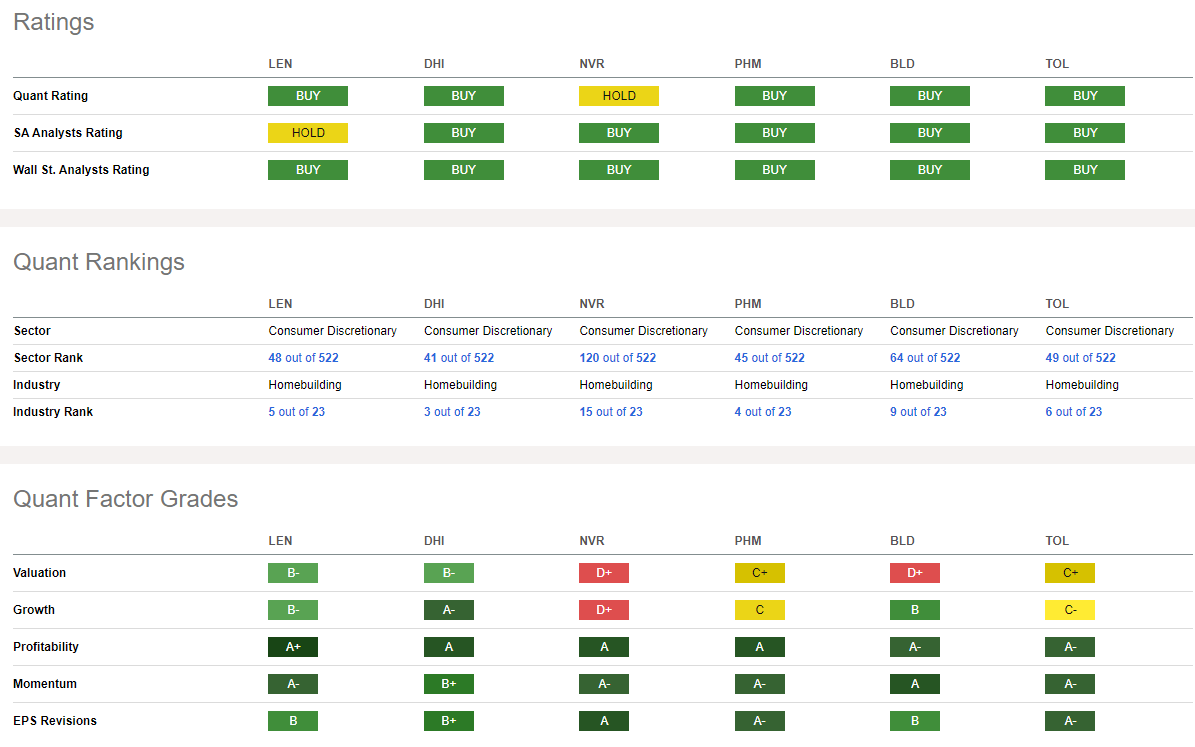

Compared to its peers, LEN features solid quant rankings across the board. The valuation appears attractive while its growth trajectory has been strong, but much will depend on how 2024 unfolds given the expected flat YoY earnings growth rate. Still, profitability trends have been stout thanks to industry tailwinds in 2023, but worsening housing affordability after a protracted period of rising rates is a key risk when looking forward.

Share-price momentum is robust at first blush, but I will note risks on the chart later in the article. Finally, EPS revisions have been mixed over the past three months, with about an even split of earnings upgrades to downgrades.

Competitor Analysis

Seeking Alpha

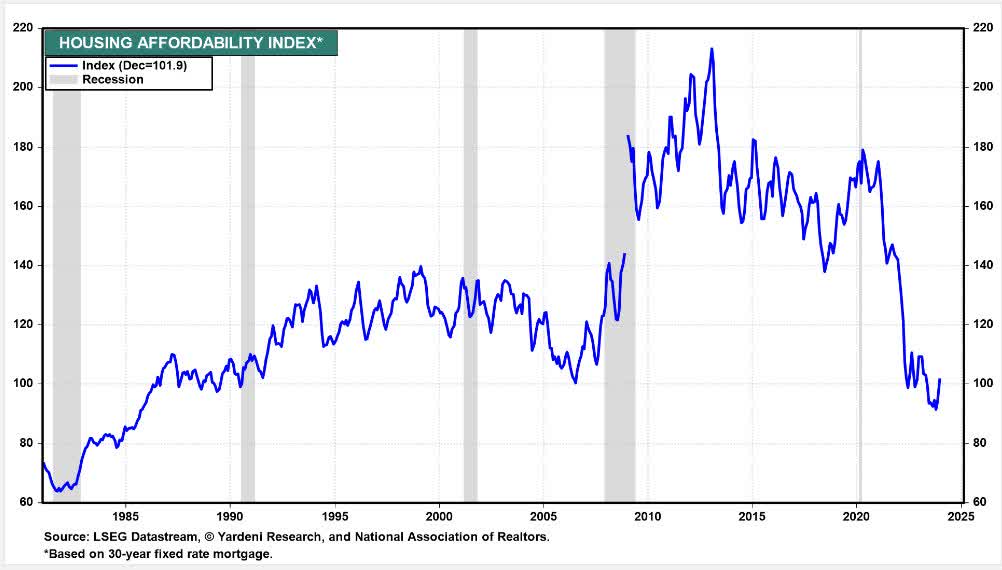

US Housing Affordability Remains Historically Weak

Yardeni Research

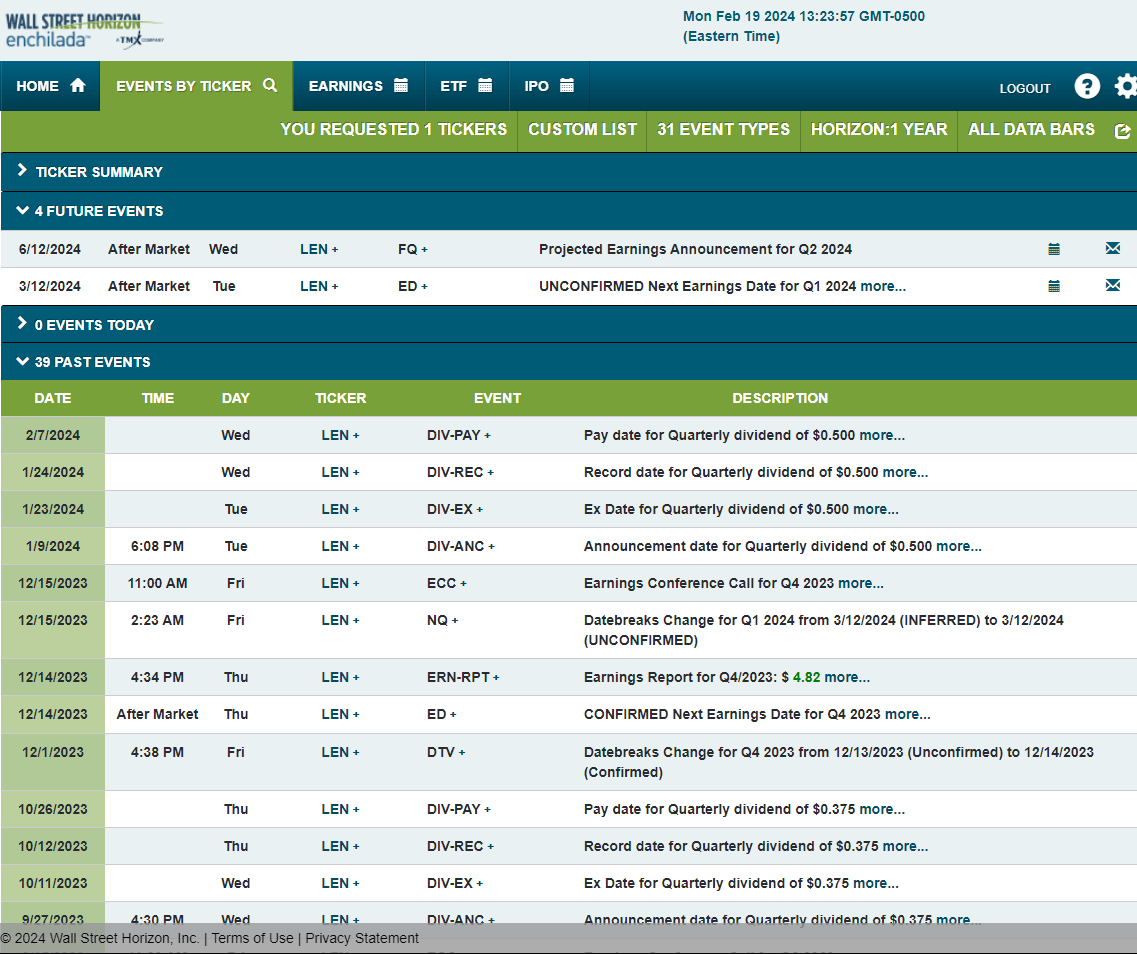

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q1 2024 earnings date of Tuesday, March 12 AMC. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

LEN has undoubtedly been a massive winner in the Consumer Discretionary sector over the past handful of quarters, key momentum risks have emerged, though. Notice in the chart below that the stock’s RSI momentum gauge, a measure of how strong a stock’s recent closes are relative to historical closes, has turned softer. When we see a series of lower highs in the RSI indicators as price creeps up, that is considered a bearish momentum divergence, implying that price will soon falter.

Making that bearish case even stronger is that the latest price advance following the late October through early December surge has been unimpressive. The rising 50-day moving average could act as critical support, while shares are highly extended from the long-term 200-day moving average. A few notable prices that could act as support are (1) the July 2023 high at $133, (2) an old price gap from November last year at $122, and (3) the late 2021 peak of $118.

Overall, given waning momentum, I would be cautious about entering a long position today.

LEN: Bearish RSI Momentum Divergence, Shares Vulnerable to a Pullback

Stockcharts.com

The Bottom Line

I have a hold rating on Lennar. Shares appear near fair value compared to historical metrics while momentum on the chart has declined markedly in the last several weeks.