Mark Wilson

Investment Thesis

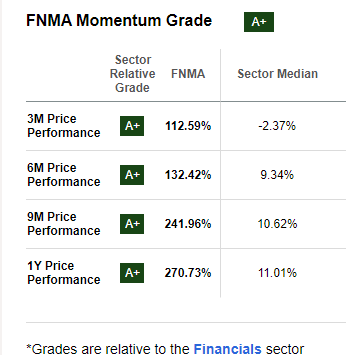

Federal National Mortgage Association (OTCQB:FNMA) is a government-sponsored enterprise that provides financing for mortgages in the US. Its stock is up by about 271% outpacing the S&P 500 by a margin of about 239%.

Seeking Alpha

From a technical standpoint, I am bullish on this stock because it just rebounded on its support level and it has a significant runway before hitting its resistance zones. I believe its upside potential is backed by its unique business model which I believe positions this company strategically for growth. Additionally, the company’s recent strategic initiatives such as the new leadership appointment and selling of non-performing loans in my view are growth catalysts. For these reasons, I am optimistic about this stock and as such I recommend it to potential investors.

Technical View: Dissecting The Price Chart

Before advancing to fundamentals, let’s study the price chart and see what there is for us as investors. Firstly, I will look at the support and resistance zones. Based on the price chart, this stock bounced strongly on its major support at about $0.4 which had occurred after a breakout below the previous support zone of $1.49. At its current price, the stock appears to be in a strong upward trajectory as indicated by its momentum metrics below.

Seeking Alpha

Given this strong momentum, I don’t see a potential retest on the support at around $0.4. As a result, I anticipate that this stock is strongly approaching its resistance levels at $3.27 and $4.22, respectively, as shown below. These two support levels are my price targets for this stock.

Trading View

In order to get a clear direction, let’s dive deeper and look at other indicators. To begin with, this stock is trading above its 50-day, 100-day, and 200-day moving averages – an indication that it is bullish in the short, medium, and long-term horizons. To solidify the upward trajectory, a bullish crossover between the 50-day and 100-day MAs occurred in January 2024 meaning that the uptrend is very strong.

Market Screener

Further, looking at the Bollinger bands, the price is above the middle line and almost breaking above the upper Bollinger band – an indication that this stock is in bullish momentum. Notably, there is a significant divergence between the lower and upper Bollinger bands, which shows how strong the bullish trend is.

Market Screener

In a nutshell, FNMA is currently in a strong upward momentum with clear resistance zones at $3.27 and $4.22 which happen to be my price targets. Given this background, a buy decision is justified.

FNMA Business Model: A Unique Growth Catalyst

This company operates under a unique business model as a government-sponsored enterprise [GSE] in the US. Its model involves expanding the secondary mortgage market by offering security to mortgage loans to mortgage-backed securities [MBS]. This approach aids in providing liquidity, stability, and affordability to the housing and mortgage sector in the US. I believe so because it purchases mortgage loans from lenders consequently freeing up capital for them to issue more housing loans. It is a system that aims at widening home ownership and making affordable housing more accessible.

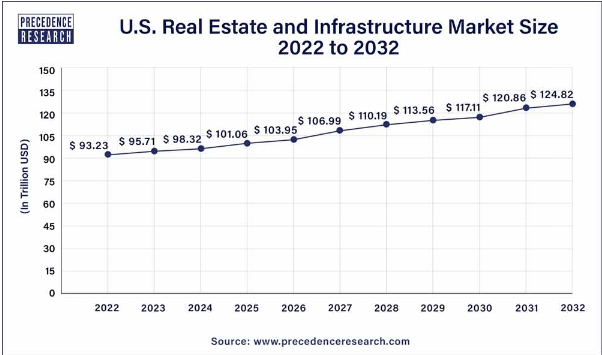

Given this model, I find this company in a prime position to grow in the future due to several reasons. First, its role in the mortgage financing system positions it to benefit from the overall growth of the housing market. According to Precedence Research, the US real estate and infrastructure market is projected to grow at a CAGR of 3% between 2023 and 2032 – something I believe to catalyze this company’s growth.

Precedence Research

I expect this company to leverage on this overall housing market growth given the projected growth in global asset-backed securities which is expected to grow by a CAGR of 7.8% between 2024 and 2030.

Verified Market Growth

Further, its model allows for innovation which I believe will also serve as a growth catalyst. For instance, On March 1, 2023, the company in its Selling Notice [SEL-2023-02] introduced updated QC requirements. The update entailed enhanced pre-funding and post-closing policies which were aimed at increasing the integrity of the mortgage process and stability of the housing market.

For example, the time frame for the post-closing QC cycles was shortened from 120 days to 90 days. In addition, the company enhanced the reporting requirements by stating that lenders must complete a minimum number of pre-funding reviews monthly and that the total number of loans to be reviewed should be either 10% of the prior month’s total closings or 750 loans. With these innovations, it means that with the reduced QC time frame, any issues can be identified and addressed faster – something that will help in maintaining the overall health of the housing financing system. Further, the enhanced reporting requirements will ensure a consistent and adequate number of loans is reviewed – something which will offer a more comprehensive overview of the lenders’ portfolio and thus help in promoting a high standard of loan quality.

The other aspect of its business model that I believe will translate into solid growth is its ability to manage economic cycles. The company’s business model carries with it to ensure a smooth flow of credit irrespective of the economic condition courtesy of its mortgage purchases ensuring a steady growth in the housing market.

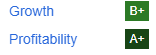

Given this background, I believe the only way to support this business model is through reflecting on its financial performance. With that in mind, FNMA has trailing revenue of $31.9 billion marking a YoY growth rate of 30.19%, and a net income of$17.4 billion, marking a YoY growth rate of 34.71%. Given this solid financial performance, the company has attractive factor grades both for growth and profitability – something I believe vindicates the company’s business model.

Seeking Alpha

Most interestingly, its business model is protected by unique legislation such as the Federal National Mortgage Charter Act, which establishes the company as a key player in the secondary mortgage market. The act ensures that FNMA operates with a degree of financial autonomy.

Strategic Initiatives

Besides its unique business model, FNMA has adopted strategic measures which I find very promising. The first initiative is the sale of non-performing loans. On March 12, 2024, the company announced the outcome of its 23rd non-performing loan sale transaction. The sale which was announced on February 8th, 2024 included the sale of 1,581 deeply delinquent loans totaling $235.8 million in UPB. The winning bidder is VWH Capital Management, LP.

This strategic move is a good decision because it has several benefits among them being the reduced portfolio risk. Through this sale, the company reduces the size of the retained mortgage portfolio therefore decreasing the exposure to loans that are not generating regular payments. The other benefit is compliance with conservatorship goals. This goal entails the reduction of the number of seriously delinquent loans and meeting portfolio reduction targets as stipulated in the Federal Housing Finance Agency goal.

The other strategic initiative is the appointment of Peter Akwaboah as the chief operating officer. I firmly believe this was an excellent move given Peter’s experience and expertise. With nearly three decades of experience in the financial services industry, Peter brings with him a lot of experience and expertise. Just to highlight his background, he has a solid focus on technology and operation having served as the COO for Technology and the Head of Innovation at Morgan Stanley. In addition, his ability to leverage opportunities as demonstrated by his involvement in a $3 billion bond sale for the government of Ghana when he was at Morgan Stanley is undisputable. Most interestingly, his diverse background ranging from roles at Deutsche Bank, KPMG and IBM not forgetting his philanthropic work is indicative of a well-rounded leader who can bring holistic leadership to this company.

In summary, Peter’s experience in conjunction with his strategic and innovative mindset paints him as a promising leader who can drive this company to greater heights.

Risks

Despite my bullish stance on this stock, it has its inherent risks which investors should be aware of. Firstly, its unique model as a GSE is subject to future government housing finance reforms which translate to some level of uncertainty. In addition, FNMA is subject to market shocks due to the cyclical nature of the real estate market something that can affect its financial performance during recessions.

Conclusion

In conclusion, FNMA is currently on a solid upward trajectory backed by solid fundamentals. I am optimistic that the upward trend will be sustained until the stock hits its resistance levels. For these reasons, I recommend this stock to potential investors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.