ALLVISIONN/iStock via Getty Images

Investors who read my articles are likely aware of my skepticism toward “investment products” that offer double-digit yields, particularly “buy-write” or “option strategy” ETFs and closed-end funds. The issue with these funds is not necessarily that their strategy is bad or meritless but that they are so often marketed to individual retired investors who are naturally attracted to high-income funds. The allure of a 20% yielding ETF is very high today as many individual investors look for ways to earn an improved income.

One example of growing popularity is the iShares 20+ Year Treasury Bond BuyWrite Strategy ETF (BATS:TLTW), which has a 19.3% TTM yield. Many investors and analysts have a bullish outlook on the fund simply due to its high yield, overlooking many of its problems. For one, stating that an option ETF pays a yield is incorrect. Mostly, it is not an actual dividend from both an SEC and tax standpoint but a return of capital, sometimes called a “distribution yield.” Investors in buy-write strategy funds should expect to lose their initial capital unless they consistently reinvest those capital distributions.

I will do what I can to explain this issue in depth so that those interested in TLTW and similar funds can approach it with knowledge. Option-oriented funds have unique risks and rewards. In some instances, TLTW could provide alpha over other strategies. However, viewing TLTW as an income generator is inaccurate in all cases. I am sure my view will be met with controversy from those who do not understand TLTW’s mechanics. I aim to educate, not offend, but if the option strategy’s mechanics cannot be understood, it is probably best to avoid it.

TLTW’s Dividend is 3.5%, Not 19%

According to the SEC’s definition of a dividend, TLTW pays a 3.52% dividend yield. That is based on its accurate yield after its 35 bps expense ratio. Luckily, TLTW has a lower expense ratio than many option-focused ETFs.

Social media and stock market websites following TLTW are riddled with articles titled “Look at this 20% yielder!” This is not one of those articles. All distributions after ~3.5% are returns of capital, not dividends, stemming from premiums from selling one-month at-the-money call options on the iShares 20+ Year Treasury Bond ETF (TLT).

Note, I’ve read some comments on other TLTW articles with readers stating that a “30-day SEC yield” is just the one-month yield (implying TLTW’s yield is 12 X 3.5%). That is not definitively true. The “30-day SEC yield measures the yield over the past 30 days and annualizes the figure.

Buying a call option allows the owner to buy TLT at a specified price for a small fee (a premium). In this case, the seller (you as a TLTW owner) agrees to sell TLT at (or near) its current price within one month. Thus, if TLT shoots up in value by then, you’ll sell it at a discount. Conversely, if TLT declines, the option buyer would have no reason to exercise, leaving you with a premium and the same underlying asset.

Indeed, TLTW’s premium returns seem like income. Many retail-oriented “market professionals” have popularized option selling as an income-generating method. When done strategically, option selling can be an alpha-generating approach, but it is not income-generating.

The reason is simple. Over time, TLT will naturally rise and fall. TLTW owners will take the loss when it falls, but when it rises, TLTW owners will not take the appreciation. The premium exists to offset this imbalance. However, if the premium is treated as “income” and spent, TLTW will naturally decline. Since TLTW pays out its premiums, it will lose all of its value someday. I do not say that as a speculation but as a theoretical principle based on simple math and statistics. If TLT was in a prolonged bull market forever or stagnant with minimal MoM volatility, TLTW could retain its value, but such does not occur, particularly for bonds.

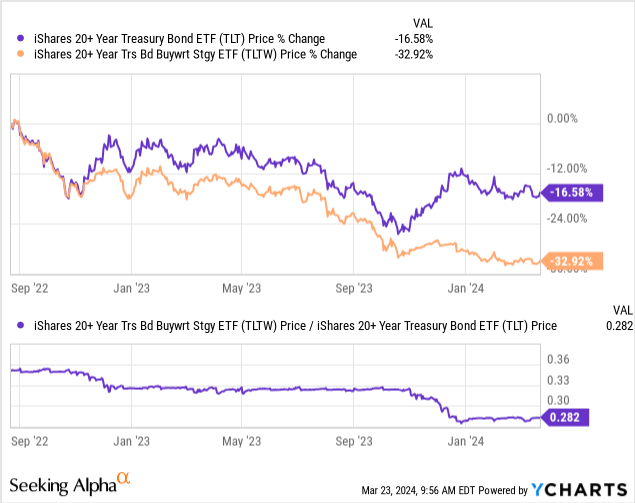

TLTW is not old and has only been traded since the fall of 2022. However, this principle is already evident in its performance record. TLTW and its underlying TLT perform the same during flat or bear markets, but TLTW underperforms significantly during TLT’s rallies. See below:

So, TLTW is exposed to the same risks as TLT but not the same rewards. As a bond fund, particularly one exposed to high-duration risk assets, TLT will naturally fluctuate dramatically in price as interest rates rise and fall. TLTW will cover the losses for TLT because owning covered calls provides an upside with defined losses but not the benefits during recoveries.

Thus, TLTW will “stair step” downward into oblivion, similar to leveraged ETFs that decay over time but with differing mechanics. Covered call strategies are new, becoming very popular over the past five years during a volatile but overall mild market period. That is to say, aside from bonds in early 2022 (which TLTW, fortunately, missed out on), there have been no significant and prolonged market declines since ~2008 (2020 being large, but not prolonged).

Owners in TLTW are, fundamentally, insurance providers who offer TLT call option buyers upside potential without risk for a premium. Accordingly, I believe option strategy ETF investors fundamentally misunderstand the risks they’re taking if treating premiums as income. The best analogy would be if your home insurance agent used your premium payments as personal income instead of putting it in a secured fund (to be used by you in the future). Of course, that is called “premium diversion” in insurance fraud, highlighting the flaw in this approach.

How To Make TLTW’s Strategy Work

To me, the issue with TLTW is not the fund itself but how it is marketed to retired income-oriented investors. In this case, it is not iShares mismarketing its product but people on investment forums and so-called “market professionals” who either do not understand options or are vying for attention from retired individual investors.

I am certain many readers fall into that category. To them, I say TLTW can have merit, but only when not treated as an income generator. You will lose your initial capital investment if you wish to use TLTW as an income vehicle. Most likely, you’d also be better off parking your savings in a 5% FDIC-insured account and withdrawing it as you need. That is effectively the same approach (return of capital) without TLTW’s other risks. Fundamentally, TLTW’s yield is below that of a short-term Treasury bond or high-yield savings account because the yield curve is inverted, meaning 20+ year yields are considerably below the short-term rate.

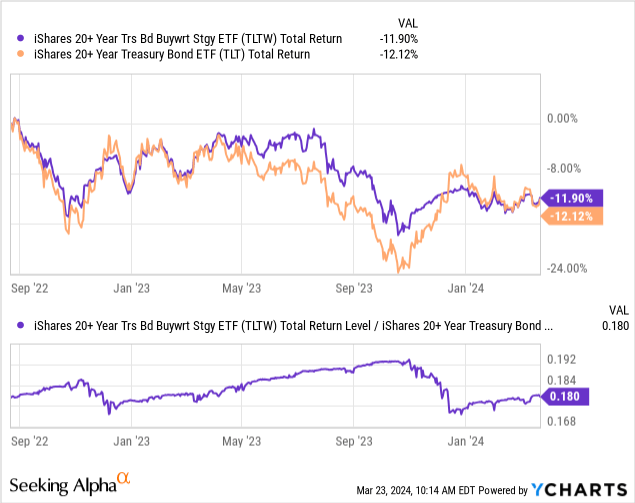

So, let’s assume that you take all of the premium distributions from TLTW and reinvest them back into the fund. This is a significantly more wise approach because it appropriately treats premiums as capital instead of “income.” We can model the returns of that strategy by considering the “total returns” of both TLT and TLTW, which are based on reinvested dividends. See below:

Clearly, we can see that, with dividend reinvestment, TLTW and TLT have almost the same performance record. The net total return for each is about -12% since TLTW’s inception. That would be positive in normal periods, but this is a very volatile bond era due to the monetary system crisis at the Federal Reserve.

Moving to the lower chart above, which depicts the ratio of each’s total returns, we can see how exactly TLTW may generate either negative or positive returns relative to the underlying TLT. We see the same pattern of relative underperformance during bond market rallies due to TLTW conferring gains to counterparties. However, we can also see that TLTW will usually outperform TLT consistently during stagnant or bear markets for TLT.

Realistically, you do not want to own TLTW during a bond bear market because the overall losses are similar; however, TLTW gets a small buffer due to its premiums. The best time to own TLTW is when you expect stagnation. For example, from January to August last year, TLT was in a tight trading range, allowing TLTW owners to earn a steady premium.

Of course, all of that outperformance was inevitably returned to the market once the range broke, demonstrating the market efficiency of options. Not all options are market-efficient, but the Treasury market is the most significant and most liquid of all global assets. Where liquidity is high, market efficiency will usually be too.

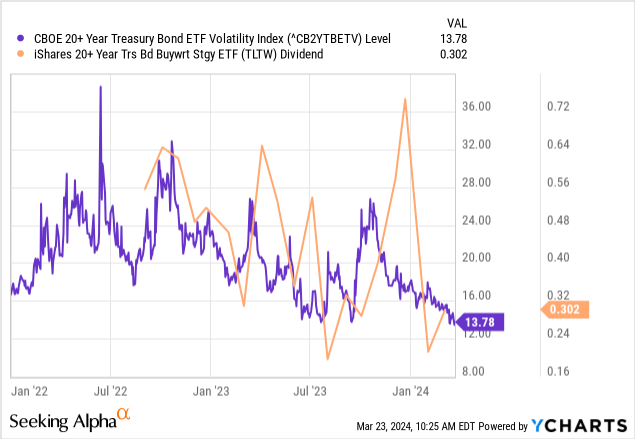

TLTW’s dividend is tied to expected volatility on long-term Treasury bonds. This is measured through the CBOE’s “VIX” index for 20+ year Treasury bonds. There is a notable correlation between this index and TLTW’s dividend.

When the bond market’s expected volatility increases, TLTW will earn a higher premium return rate to offset the risk of relative losses. There is some difference between TLTW’s dividend and the long-term bond volatility index because TLTW has discretion in how dividends are returned. However, for the most part, this index is a live measure of TLTW’s profitability.

Theoretically, the ideal time to buy TLTW is when the long-term bond volatility index is high (above 20) and you expect volatility to decline. In those instances, TLTW would be earning a higher premium than its risk, allowing for the creation of actual income.

Of course, outside of specific situations, I doubt that strategy is feasible because of market efficiency. Based on my experience, the long-term bond market is somewhat inefficient because QE, QT, and rate changes from the Federal Reserve push around its price. However, options are priced with relatively robust statistical models, so the only consistent way to profit from them is likely in less liquid or niche stock options where institutional money can’t fit. Thus, smaller traders can earn a profit by providing liquidity. Of course, that approach can also be dangerous if not done by a very knowledgeable speculator.

The Bottom Line

In no instances should TLTW be viewed as a long-term income investment. In my view, most option ETFs will not exist five to ten years from now, and there may be some legal questions or complaints regarding fiduciary responsibilities in how these funds are marketed to investors. My opinion on this is shared by many who understand the basics of options. But, to my surprise, so much of the internet is riddled with misinformation regarding buywrite option ETFs.

Remember, if you’re a retired individual investor, your time and money are worth a lot to some, and not all in this industry necessarily care for fiduciary responsibility. In this case, it is the “suitability standard” that I feel often disregarded, as those who understand basic option mechanics should know that option selling is not a feasible long-term income approach.

I will gamble that someone will comment, saying, “Well, I’ve made over this much in income since I bought it!” To that, I say that unless you bought it around November of last year, your net total return after capital changes is negative or very low. Further, I will gamble that any gains since November will be returned to the market unless those premiums are reinvested.

That warning aside, I am also bearish on TLTW for other reasons. As detailed earlier, TLTW outperforms during periods of high expected bond volatility compared to low realized volatility (i.e., flat markets). For example, if we see TLT crash, it may be wise to buy TLTW after it has rebounded for a month or two. Today, the bond market’s expected volatility is the lowest since 2021. For reasons explained in “BND: Avoid Bonds As Service Inflation Rebounds To 8%,” I think TLT’s volatility is about to pick up again, meaning TLTW will not earn sufficiently high premiums to offset losses.

Further, it may be that TLT rebounds if inflation falls, for example, in a shock recession. In that instance, TLTW’s absolute performance would be flat, but it would not earn the upside of TLT, causing it to underperform. Thus, I believe TLTW is very likely to underperform the underlying TLT regardless of TLT’s overall direction, given I expect TLT will be more volatile than its options market is accounting for.