David Ramos

In the ever-evolving landscape of technology, few names have carried as much historical weight as International Business Machines Corporation (NYSE:IBM). However, behind its legacy and stature hides a company that has recently grappled with leveraging potential from seismic shifts in the tech industry, including cloud computing and AI, struggling to keep pace with more agile, innovative counterparts like Google (GOOG) and Microsoft (MSFT).

Trading at an implied 2024 EV/EBIT of around 18x, paired with negative fundamental and competitive momentum, I view IBM as overvalued and not suited for growth investment. According to my EPS projections for the company through 2025, in combination with a 9% cost of equity and a 3% terminal growth rate, IBM shares should be fairly valued at around $134. With neither IBM’s momentum in business fundamentals nor valuation being supportive for an investment, I view the company as a “Sell”.

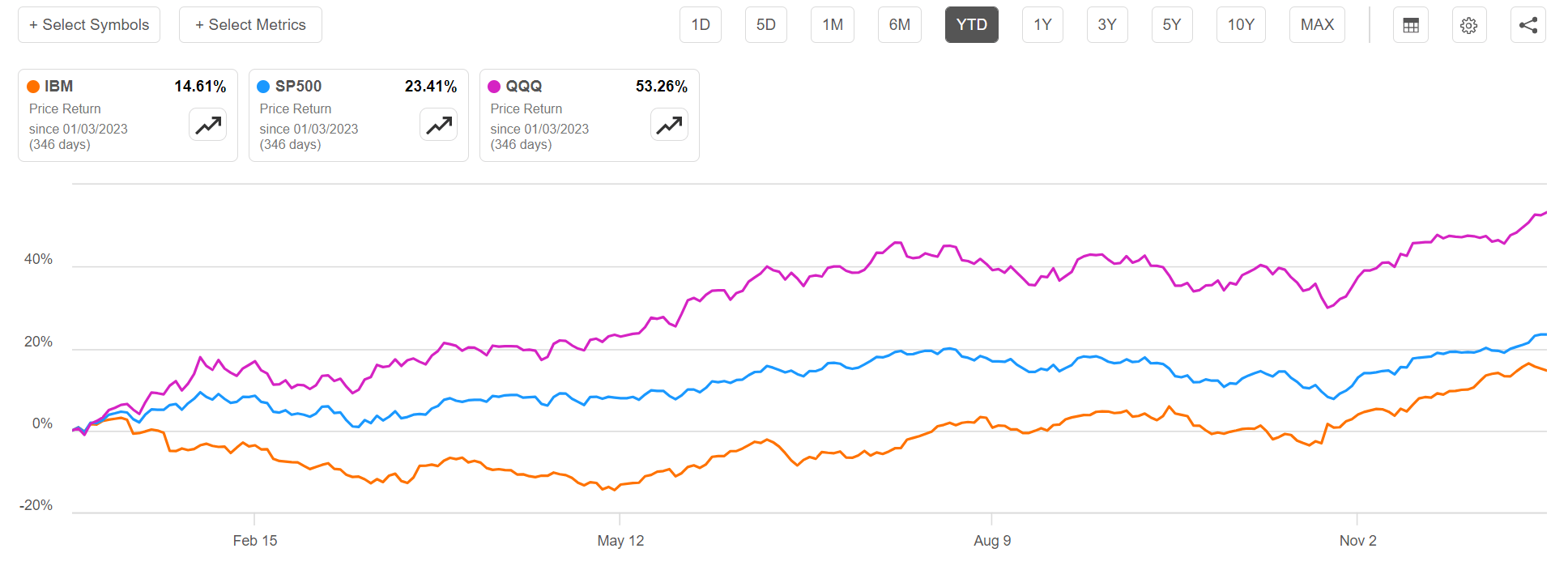

For context, IBM stock has underperformed the broad equities market YTD, especially when compared to the “Tech” benchmark. Since the start of the year, IBM shares are up less than 15%, compared to a gain of approximately 23% for the S&P 500 (SP500) and a gain of close to 53% for the Nasdaq tech-heavy Nasdaq 100 (QQQ).

Seeking Alpha

Steady Revenue Loss And Earnings Contraction

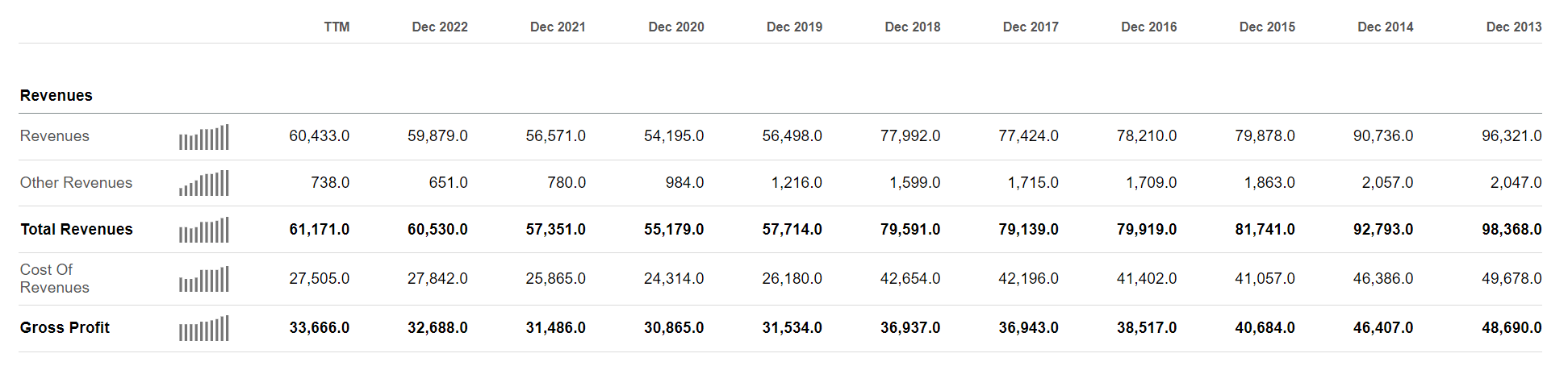

Reflecting on IBM’s historical performance, I cannot help thinking about the famous Warren Buffett quote: “Time is the friend of the wonderful company, the enemy of the mediocre.” During the past decade, IBM has lost about one-third of its top line, with revenues falling from $96 billion in FY 2013 to $60.4 billion for the trailing twelve months, a negative CAGR of about 4.5%.

Seeking Alpha

The loss of top line is especially negative in the context of the company’s active M&A activity during the discussed period:

-

In 2013, SoftLayer Technologies: Acquired for approximately $2 billion, SoftLayer formed the backbone of IBM’s cloud infrastructure services, strengthening its cloud computing offerings.

-

Also in 2013, Trusteer: Acquired for an estimated $1 billion, Trusteer’s cybersecurity technology was integrated into IBM’s security solutions to bolster protection against fraud and cyber threats for financial institutions.

-

In 2015, Cleversafe: IBM acquired Cleversafe to enhance its cloud storage solutions. The acquisition price was approximately $1.3 billion.

-

In 2016, Truven Health Analytics: IBM acquired Truven Health Analytics for around $2.6 billion, focusing on healthcare data analytics to bolster insights for healthcare organizations.

- In 2019, Red Hat: Acquired for approximately $34 billion, this marked IBM’s significant move into the hybrid cloud market, leveraging Red Hat’s expertise in open-source software and cloud technologies.

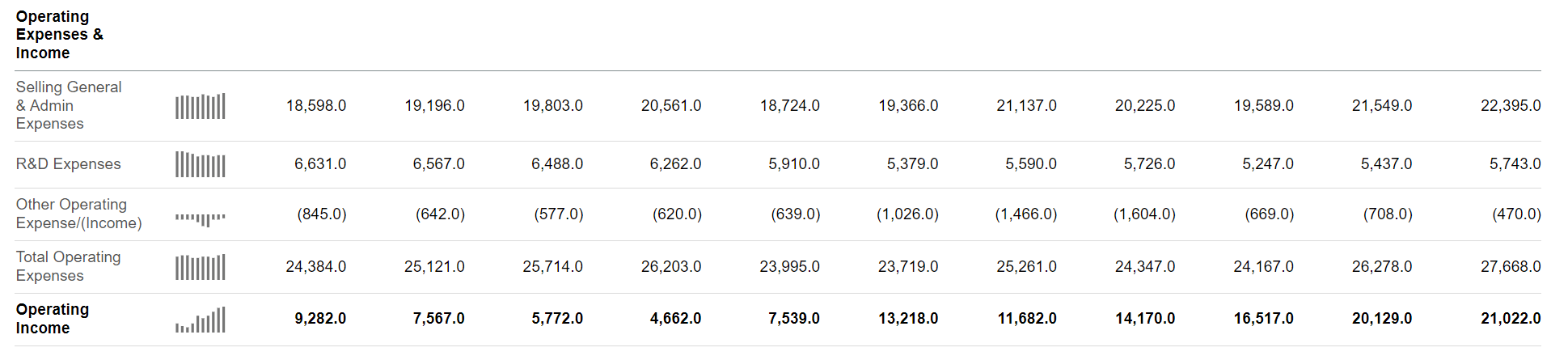

The loss of top line is also reflected in earnings. Over the past decade, IBM’s operating profit contracted to $9.2 billion for the trailing twelve months, compared to $21 billion achieved in FY 2013 (-8% CAGR).

Seeking Alpha

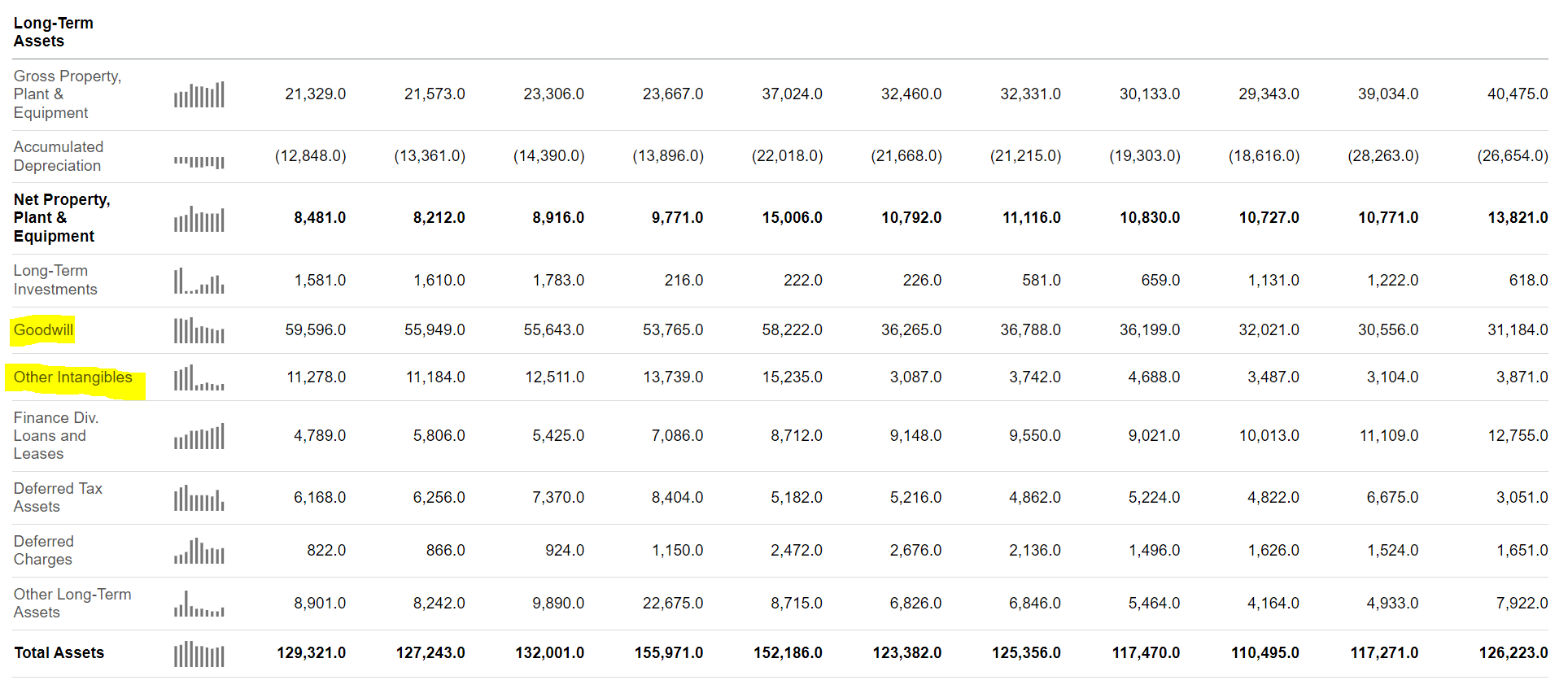

Meanwhile, IBM’s net debt increased from $28.7 billion in 2013 to $47.5 billion as of Q3 2023. The total balance sheet grew from $126.2 billion to $129.3 billion, with outsized growth attributed to Goodwill and Other Intangibles.

In other words, IBM is consuming more capital without increasing earrings – almost the picture-book definition of a bad business, in my opinion.

Seeking Alpha

Low Competitiveness Suggests Continued Underperformance

IBM’s fundamental performance has been catalysed by several challenges that unfortunately do not appear to be fading away anytime soon. Firstly, I point out that IBM has historically been relatively slow in adapting to market trends. And this is not just a question of ambition or management. In fact, while the company has made efforts to pivot toward growth areas like cloud computing and AI, the company has faced challenges in attracting equally-competitive human capital and partnership opportunities as Microsoft or Google. Moreover, investors should consider that IBM’s legacy business is anchored on hardware and on-premise enterprise software, a backdrop that is less nimble and agile to adapt to the changing, cloud-based software landscape. This challenge is compounded by intense competition from super-successful tech players. Lastly, some market participants have frequently criticized IBM for execution issues in implementing its strategic initiatives such as delays or inefficiencies in integrating acquisitions, transforming business models, or delivering on growth promises that have affected investor confidence.

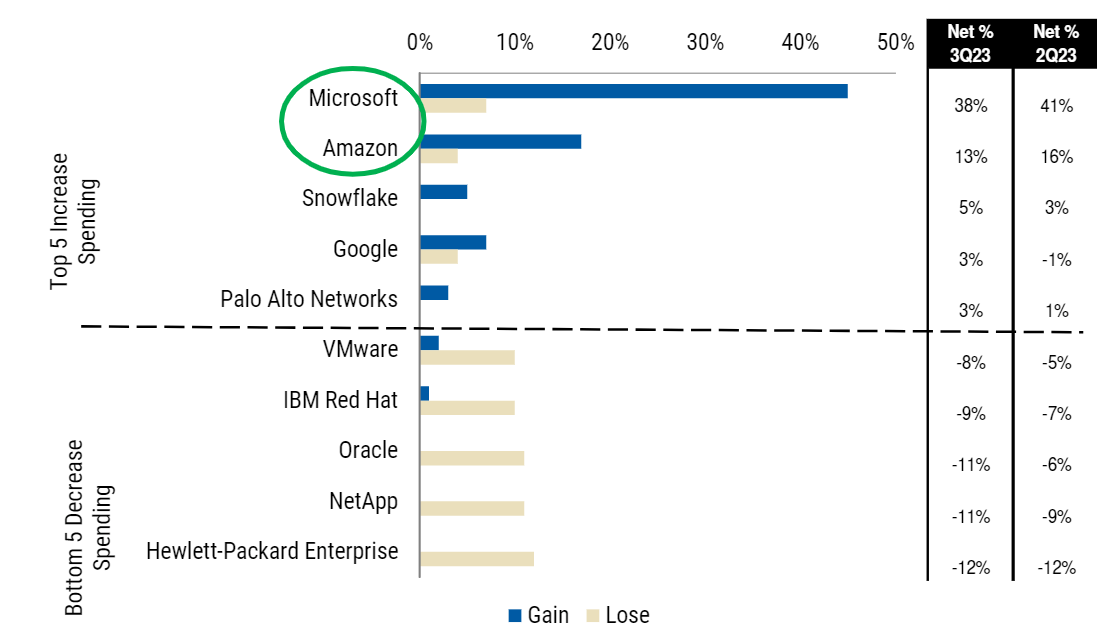

Admittedly, IBM has undergone quite a significant business shift recently, especially after the Kyndryl spin-off, directing its attention toward two primary growth drivers: Hybrid Cloud and AI. This strategic transformation positions IBM to achieve its long-term financial goals, with a substantial 75% of its revenue now stemming from Software and Consulting. That said, however, IBM still remains a structural loser vs Microsoft, Amazon, Google, and other tech giants. According to Morgan Stanley’s 3Q23 CIO Survey (dated October 9th), the U.S. most important technology-related decision makers expect that their spending on IBM’s Red Hat (cloud) will decrease about 9% over the next 3 years.

Morgan Stanley

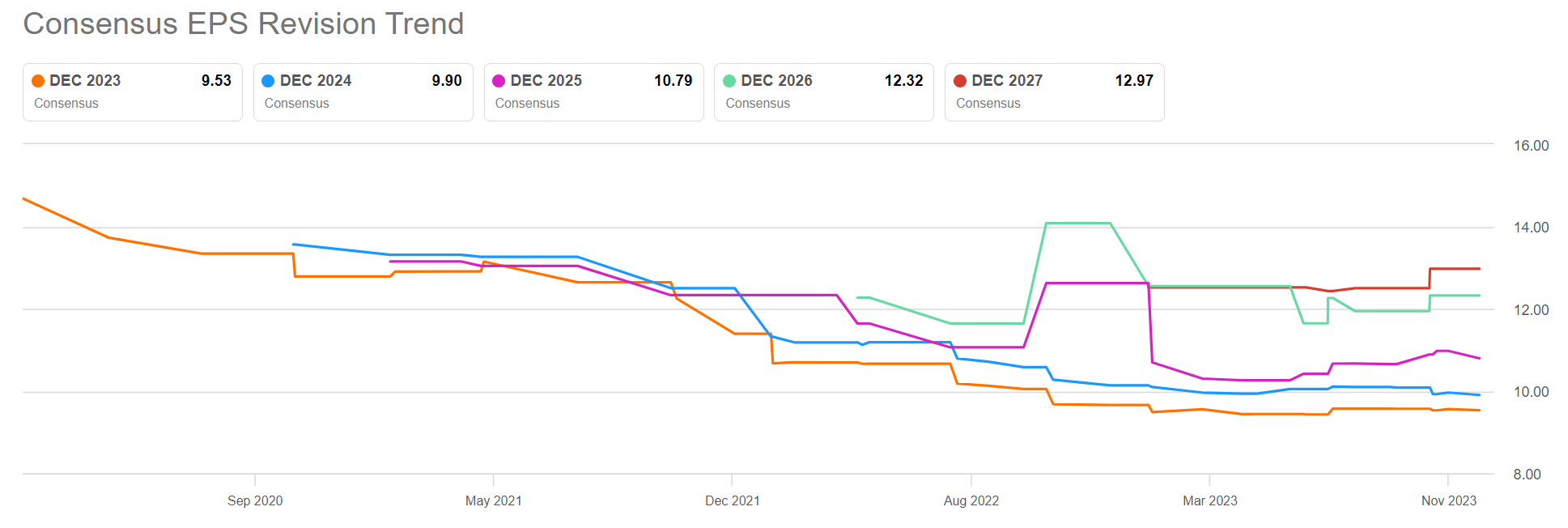

All that said, IBM is seeing negative momentum on consensus EPS expectations, with earnings estimates trending downward for over 3 years now.

Seeking Alpha

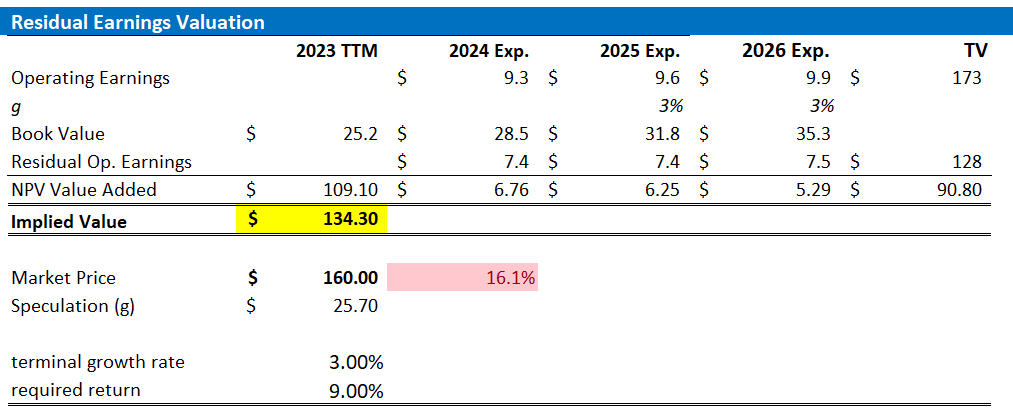

Valuation: Set TP At $134/Share

In my opinion, companies with steady and relatively predictable business fundamentals like IBM are quite easily and precisely valued with a residual earnings model, which anchors on the idea that a valuation should equal a business’ discounted future earnings after capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

With regard to my IBM stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal till 2026. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor on IBM’s cost of equity at 9%, which is approximately in line with the CAPM framework.

- For the terminal growth rate after 2025, I apply 3%, which is about 25-50 basis points above the estimated nominal global GDP growth. The growth premium should reflect the elevated potential for technology businesses in general. At the same time, knowing that IBM has a history to underperform the tech industry, I don’t want to be too optimistic in my post-2026 outlook.

Given these assumptions, I calculate a base-case target price for IBM stock of about $134/share.

Analyst Consensus; Company Financials; Author’s Calculations

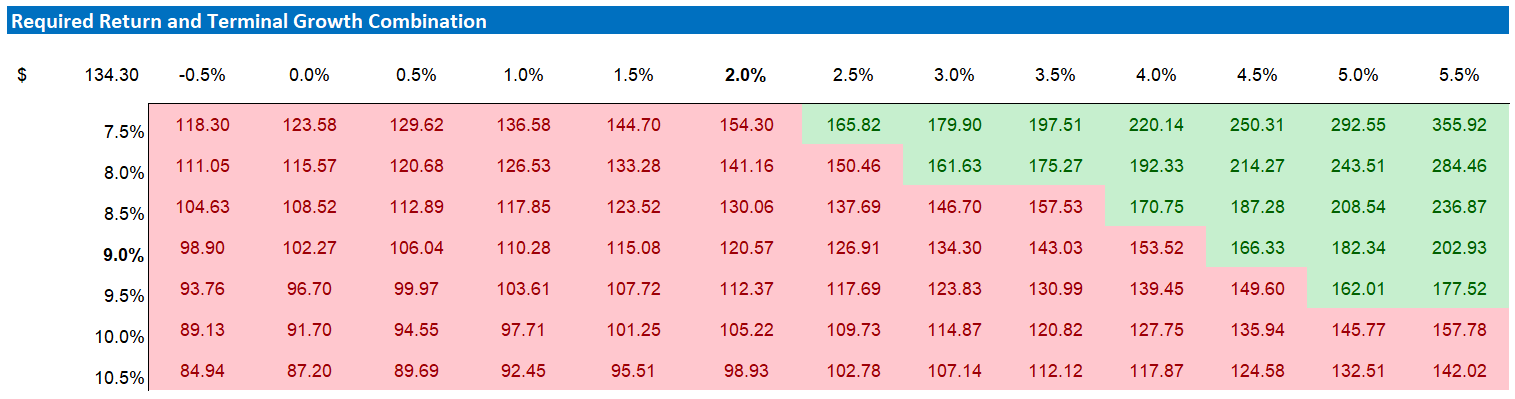

As I argued that my estimates for growth and equity charges may be conservative, I acknowledge that investors may hold varying assumptions regarding these rates. Therefore, I’ve included a sensitivity table to test different scenarios and assumptions. See below.

Analyst Consensus; Company Financials; Author’s Calculations

Upside Risks

I am bearish on IBM stock. However, there may be a few “upside risks” that may render IBM’s negative momentum and valuation less notable. Specifically, I highlight that a strengthening global GDP outlook could stimulate increased IT spending, especially in segments like Consulting and Software, exerting upward pressure on consensus EPS estimations and bolstering IBM’s financial outlook. Moreover, while I do not think IBM has significant potential for industry-leading innovation and software commercialization, IBM’s ongoing product transition toward cloud and AI may nevertheless present an opportunity for R&D upside and renewed customer interest.

Investor Takeaway

IBM has struggled to leverage potential from shifts in the tech industry, falling behind and losing share vs. more agile competitors like Google and Microsoft. As a consequence, the company has experienced steady revenue loss and earnings contraction over the past decade, despite active M&A activity.

With challenged fundamentals, trading at an implied 2024 EV/EBIT of around 18x, I view IBM as overvalued. According to my EPS projections for the company through the next 3 years, paired with a 9% cost of equity and a 3% terminal growth rate, IBM shares should be fairly valued at around $134. “Sell”.