Shares of proteomics innovator Quantum-Si (QSI -11.45%) had a wild 2023. The start-up enables cutting-edge research into the world of proteins, which can hold the key to developing advanced healthcare treatments and broadening our understanding of biology at large.

Shares shot higher in July when famed tech investor Cathie Wood started buying the stock again. Wood’s Ark Genomic Revolution ETF owns nearly 12% of Quantum-Si as of this writing.

Proteomics is still early in commercial development. But it’s promising enough that medical instrumentation and services giant Thermo Fisher Scientific (TMO -0.40%) is acquiring another proteomics equipment start-up, Olink (OLK -0.16%), for $3.1 billion. The offer was announced in October, a few months after Wood’s latest Quantum-Si stock purchase, and was a 74% premium to where Olink was trading prior to the deal announcement.

Following a precipitous fall after the Cathie Wood hype wore off, Quantum-Si stock has been showing signs of life again in recent months. Quantum-Si’s affordable semiconductor-based proteomics system certainly seems to hold key technological advantages over anything else commercially available right now. And increasing distribution of its “Platinum” benchtop protein sequencing device holds promise.

However, at this juncture, and for most retail investors, Olink acquirer Thermo Fisher is a better long-term investment than Quantum-Si.

Quantum-Si’s current disadvantage

To illustrate the long uphill battle Quantum-Si has ahead of it, look no further than the top-line financials. In Q3 2023, the company logged just $223,000 in sales. Given that each of its benchtop proteomics systems costs roughly $70,000, it only sold a few of them last quarter.

And as I wrote over the summer, the backlog of orders looks meager for now too. As of the end of September, the backlog was just approximately $100,000; not much different from where it was at the end of the prior quarter. Perhaps Quantum-Si’s new distribution agreements will help ramp up potential customer interest, with a “full commercial launch” anticipated later in 2024.

In the meantime, Quantum-Si continues to burn through cash. Net losses totaled $74 million in the first nine months of 2023, or negative $69 million on an adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) basis. Management has stated that the nearly $275 million in cash and short-term investments should keep Quantum-Si’s development moving forward “into 2026.”

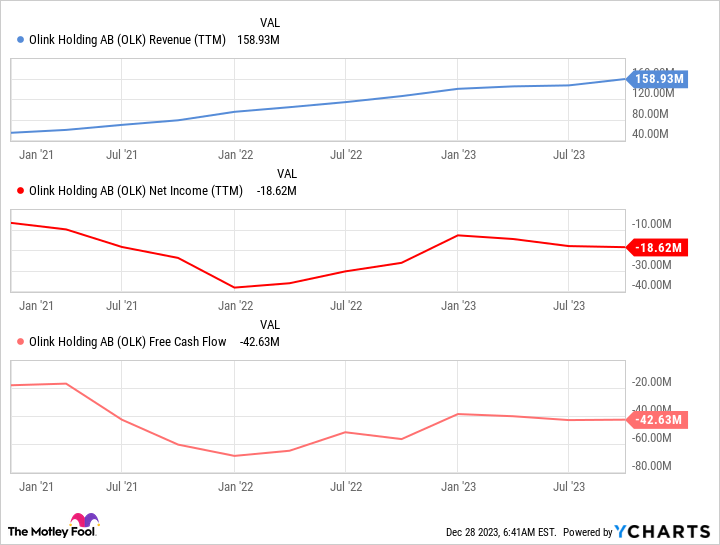

Olink also has limited sales and is losing money too — both on a GAAP and free-cash-flow basis.

Data by YCharts.

However, parent-to-be Thermo Fisher is a highly profitable giant and has deep pockets. Olink will need cash to fuel its future potential in proteomics, and Thermo Fisher can deliver. At some point, unless the sales outlook dramatically changes, Quantum-Si will be in need of some outside cash infusion.

What should investors do?

For some investors looking for a more speculative but only potentially high-reward stock, Quantum-Si does hold promise. But the research-based ecosystem surrounding proteomics will need to be expanded for a bigger payoff to eventually be realized, and that could take time — time that Quantum-Si may or may not have, given its tenuous financials at the moment.

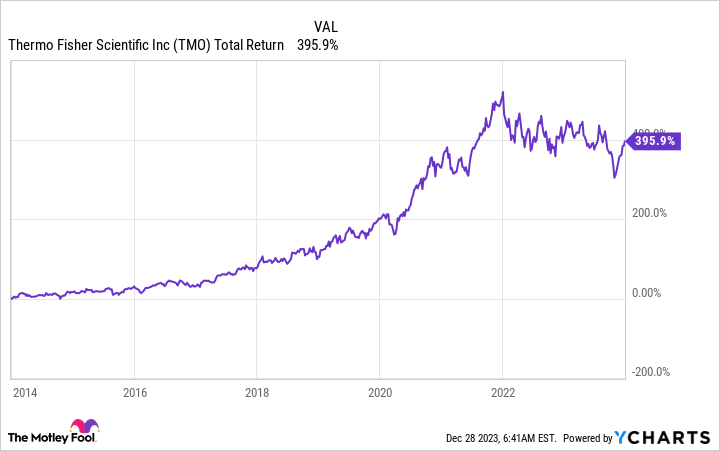

For investors looking for a more surefire long-term return, Thermo Fisher-plus-Olink checks off some key boxes. The combined business is profitable, Thermo Fisher pays a dividend, and it has a long track record of slower-but-steady returns for shareholders (as measured by total return, which combines stock price appreciation with reinvested dividends).

Data by YCharts.

For most retail investors, Quantum-Si should be viewed as little more than a speculative bet. An investment into its stock, if any, should reflect that. Olink’s acquirer Thermo Fisher is a better healthcare, life sciences, and proteomics stock investment right now.

Nicholas Rossolillo and his clients have no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Thermo Fisher Scientific. The Motley Fool has a disclosure policy.