maybefalse

There is strong sentiment around Alibaba Group Holding (NYSE:BABA) right now. While many Seeking Alpha analysts suggest that the stock is a Buy, I’m hesitant because of the growth rates that may struggle to get back to prior levels after a significant slowdown. Seeking Alpha’s Ratings Summary designates a Hold to the stock, and I think this is more reasonable given the growth risk.

Operations

T-Head, which is Alibaba’s chip design subsidiary, has introduced a RISC-V-based controller IC for solid-state drives called the ‘Zhenyue 510’ chip. Its purpose is to enhance performance in Alibaba Cloud’s data centers and is useful for AI training, digital transactions, and data analysis. This shift to chip design protects the firm from risks associated with U.S. export controls and also improves efficiency for the company related to data tasks.

The organization has also seen critical leadership changes with the intent of making its e-commerce operations more technology-intensive. For example, it distributes traffic through algorithms in a manner similar to peer PDD Holdings (PDD), in an effort to reduce operating costs for merchants. The company has recently lost its position as the leading e-commerce operator to Pinduoduo. Amidst the leadership reshuffle, a complete restructuring into six independent groups has been announced. Yet, the restructuring efforts related to the cloud operations and Hema Fresh, its grocery business, have been suspended.

Growth Concerns

While the company has a strong history of high growth, it has struggled in recent years to maintain its past performance. This comes at a time when the general Chinese economy has also seen a significant slowdown. The establishment of the National Financial Regulatory Administration in 2023, taking over from the China Banking and Insurance Regulatory Commission, has raised regulatory scrutiny, and the Chinese government has been directly influencing major companies away from a market-driven direction. There is also significant geopolitical risk, primarily surrounding Taiwan, but also in wider economic competition with the U.S. that is affecting investor sentiment in Chinese companies.

Alibaba has suffered from net income challenges since mid-2021 and with revenue difficulties since early 2022:

Author, Using Seeking Alpha

Recently, the company’s earnings have been much more favorable, and the stock price has remained largely flat, indicating a potential opportunity for value investors looking to capitalize on what could be a turnaround moment for a laggard few years.

Seeking Alpha

The question remains as to whether the company can continue to increase these reported earnings at the rate it has since September 2022 and whether the revenue growth can find new momentum.

In an effort to drive revenue growth, the company is ramping up cloud services generally, including the Hanguang 800 neural processing unit for AI and the Yitian 710 Arm-based CPU for the cloud. A focus on e-commerce and AI is seeing Taobao and Tmall, the firm’s largest revenue sources, implement new technologies with a ‘user-first’ strategy. Their advertising platform, called Wanxiangtai Unbounded, is also implementing AI with high adoption rates among merchants. The firm’s Cloud Intelligence Group is investing significantly in generative AI, upgrading its large language model, and attracting AI talent to bolster its competitiveness. This is a challenge that is increasingly important as major rival Amazon.com (AMZN) has such an intense investment in advanced technology with AWS.

The firm’s international operations, including Lazada and AliExpress, saw a leap of 73% in revenue year-over-year, with improved margins at Lazada and Trendyol. The company is investing in new ventures like Miravia in Spain and further improving the existing AliExpress Choice. Efforts like this cater to new markets and bolster revenue growth opportunities. AI will largely help the firm’s margins in the long term, and improvements in Cainiao, Alibaba’s logistics arm, are contributing to strong growth in quarterly revenue and improving margin outlooks.

Valuation

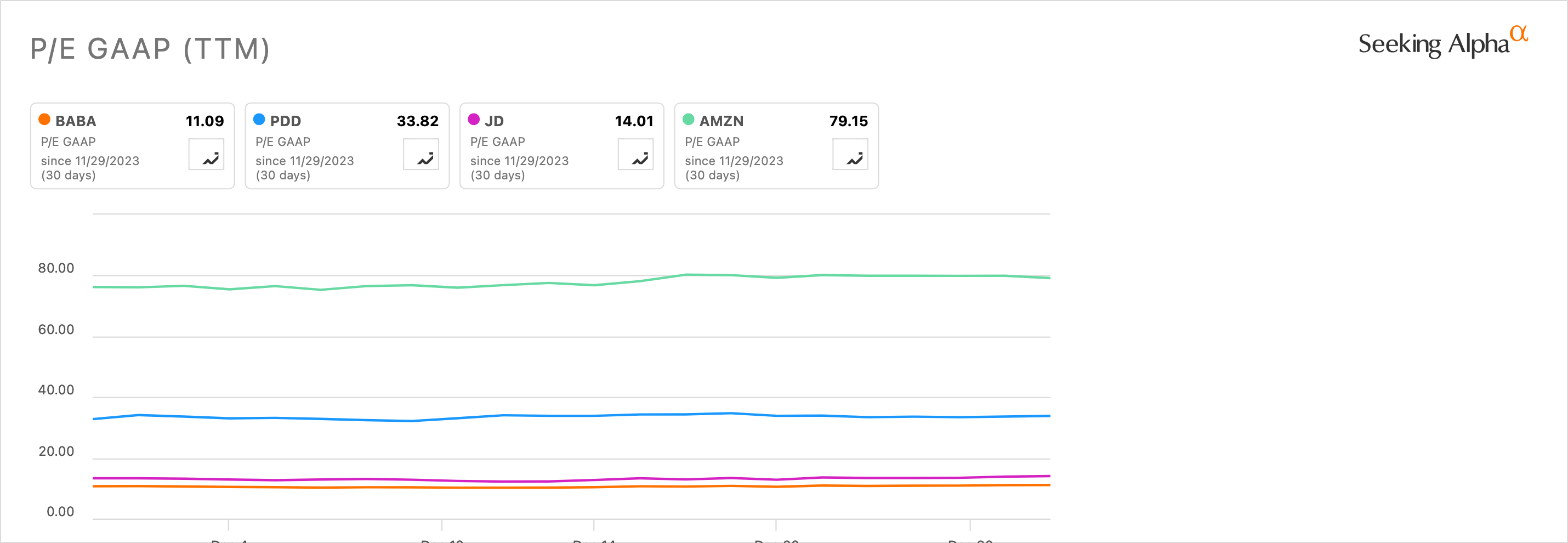

I believe the company’s valuation is its strongest point. I can also compare this to peers to get a closer look at the significant opportunity here in Chinese marketplace stocks in general.

Author, Using Seeking Alpha

Alibaba, on the P/E ratio front, is the cheapest of the three main Chinese marketplace peers and also immensely cheaper than Amazon in the U.S.

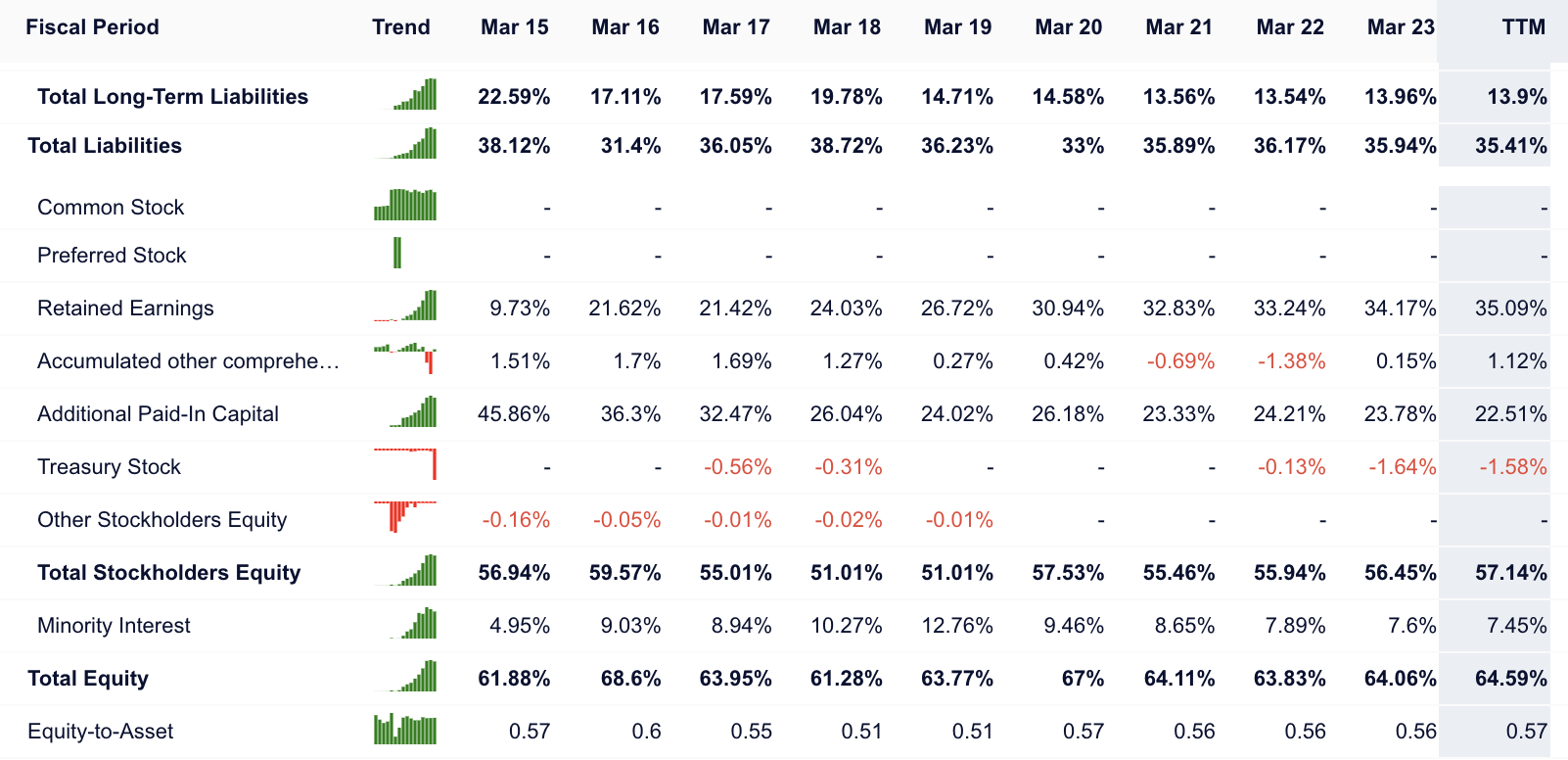

A stable balance sheet, including relatively static total equity and liabilities percentages as far back as 2015, also presents favor for the stock’s valuation, as no major debt concerns reveal a value trap of sorts.

GuruFocus

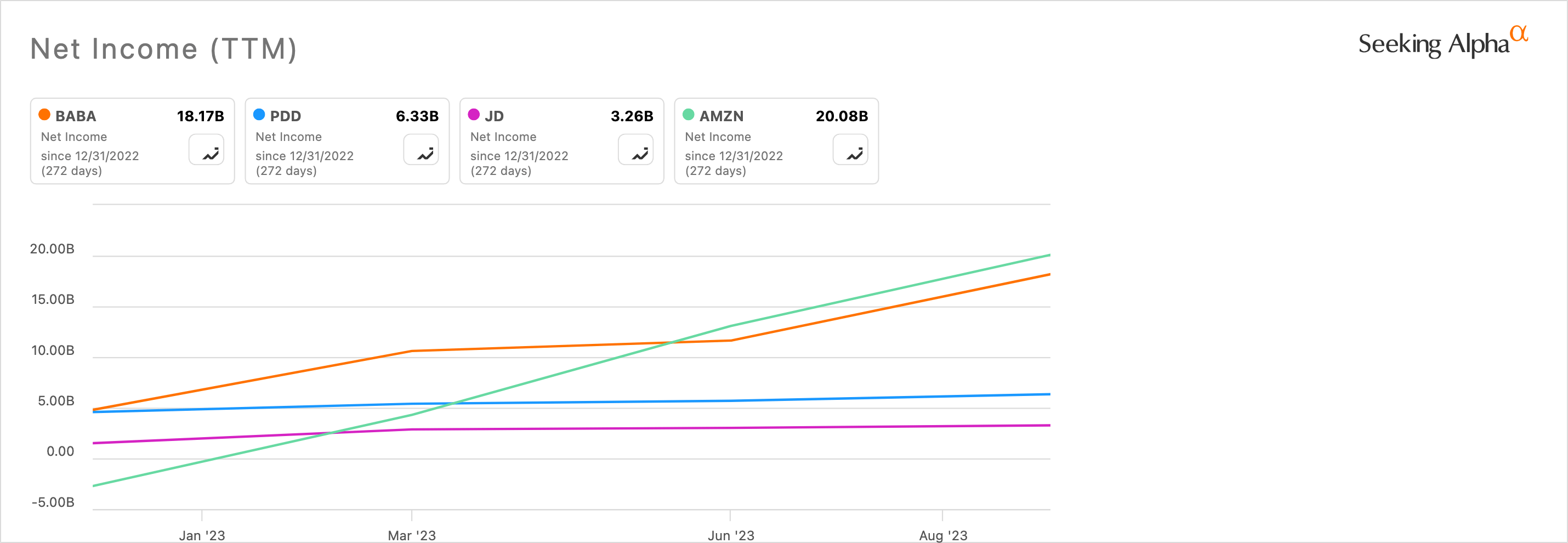

Alibaba also well outperforms its peers with net income in the range of Amazon.com, leading to positive sentiment in terms of the current stock price being a significant value opportunity.

Author, Using Seeking Alpha

Risks

While growth concerns remain my largest risk for an investment in Alibaba, there are some other considerations I believe need to be addressed before considering an investment.

Macroeconomic risks related to the Chinese economy are important to consider, and adverse market conditions, including the regulatory and governmental interventions mentioned above, could significantly impact investment in Alibaba.

In addition, the restructuring efforts have seen serious delays, and sentiment is growing that the company’s strategy changes may not be going as planned. Its cloud unit spin-off was in response to U.S. restrictions on semiconductor chip exports, but the cloud plans have not gone ahead.

Conclusion

In my opinion, I think there are better options for investors to consider, and while I believe the stock is a value opportunity, I personally wouldn’t buy it. If I had bought it recently, I would hold it for longer for tax reasons to get the investment returns I believe are reasonable to expect based on the undervaluation and growth strategies underway.