Klaus Vedfelt

Thesis

BlackRock (BLK) is usually a ‘gorilla’ in any niche of the finance industry it enters. Surprisingly, however, its foray into CLO ETFs has been lackluster to say the least, despite robust fundamental returns and composition for its flagship ETF, the BlackRock AAA CLO ETF (NASDAQ:CLOA).

We have covered this name before when it came to market, and are revisiting it now almost a year after, given the substantial change in landscape since issuance. In our initial coverage, we explained the structure of the CLO market and the seniority of AAA tranches, highlighting the very low credit risk undertaken by market participants who invest in AAA CLOs. Unlike AAA CDOs, the CLO asset class has experienced only a handful of defaults since inception at the AAA level, proving its mettle and the robustness of first lien senior secured loans in the capital structure of a company.

In this article, we are going to revisit the name in light of the explosive growth in its competitor Janus Henderson AAA CLO ETF (JAAA), and the re-emergence of the higher for longer theme in the Fed Funds market.

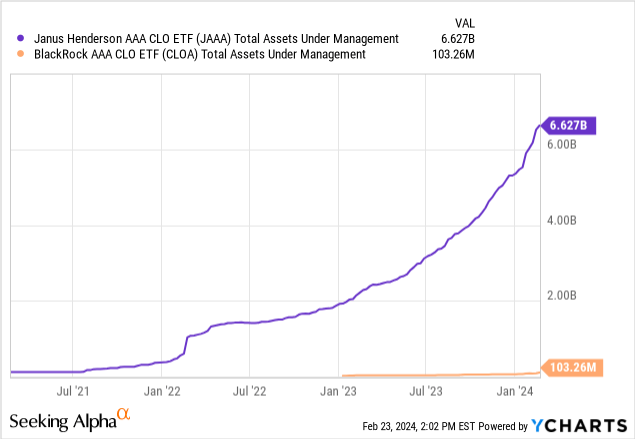

Explosive growth for JAAA, while CLOA has been static

It is surprising to witness BlackRock trailing so much in an asset class which is becoming mainstream:

Since it was launched in the beginning of 2023, CLOA has not been able to drum-up a lot of interest, all while JAAA has seen its assets triple, now recording an astounding $6.6 billion in assets under management.

Again, we are a bit surprised by this state, since BlackRock has shown again and again that as a premiere global asset manager, it gets significant investor interest and assets into the funds it issues. One can just look at the newly launched Bitcoin ETFs and see how fund flows behaved for the BlackRock product. Not for CLOA, though. Not yet.

AAA CLOs are not fungible, but many are very similar

While AAA CLOs are not fungible (i.e., all the same), they do exhibit very closely correlated characteristics at the AAA tranche. Those characteristics are subordination, break-even default rates, collateral composition (in broad strokes) and vintage.

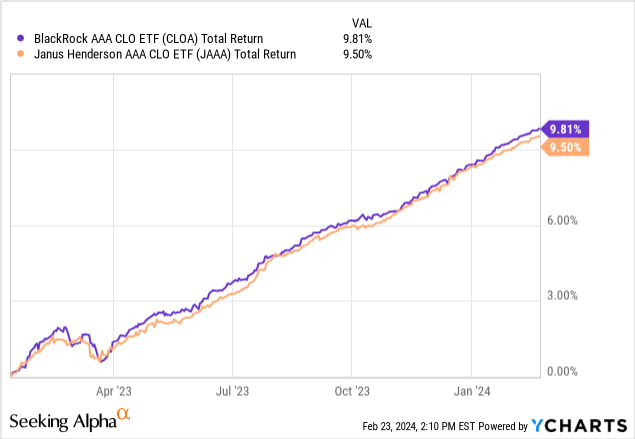

CLOA has exhibited a total return since issuance which is very competitive when compared to JAAA:

CLOA has posted a total return of 9.8% since issuance, slightly higher than the one recorded for JAAA. The numbers are very closely aligned, with similar drawdown profiles, which speak to the way CLO AAA performs in general.

While JAAA is an actively managed ETF, CLOA is an index fund, aiming to track the J.P. Morgan CLOIE AAA Index. As we can see from the above chart, the two strategies are very closely aligned, and we believe we won’t see much of a difference unless we have a significant recession which would bring high default rates and a true differentiation in collateral pools utilized for the CLO vehicles.

CLOA has lower fees

BlackRock is a behemoth in the asset management space, with a very robust research and trading platform, which usually helps BlackRock funds in charging lower fees. It is the case here as well, with CLOA charging only 20 bps versus 22 bps for JAAA. The figures are very similar, so we are not going to split hairs here, however CLOA is very competitive in terms of management fees for this product.

Kindly keep in mind that competing products, such as short duration corporate bond funds, can exhibit expense ratios anywhere from 30 bps to 45 bps, even after waivers are factored in:

- the PIMCO Enhanced Short Maturity Active Exchange-Traded Fund ETF (MINT) charges 0.35%

- the First Trust Enhanced Short Maturity ETF (FTSM) charges 0.45%

Valuation is compelling

Rather than go through the AAA CLO structure, which we did in our original article covering this name, we are going to focus on the reasons underlying the compelling valuation for this asset class in the current macro environment.

AAA CLOs are a floating rate asset, meaning they pay a spread over SOFR, and thus are a preferred asset class while rates are high:

Fund Details (Fund Website)

The fund has a 30-day SEC yield of 6.54%, with an option adjusted spread of 127 bps. Spreads are what investors get paid over risk-free rates, and BlackRock defines this metric as such:

The weighted average incremental yield earned over similar duration US Treasuries, measured in basis points (one basis point is equivalent to 0.01% or 0.0001). This metric considers the likelihood that bonds will be called or prepaid before the scheduled maturity date.

You are therefore getting paid 1.27% over treasuries in order to take risk in a low volatility asset class that as per the Seeking Alpha platform ‘Risk‘ tab, has a standard deviation of only 1.4%, and an annualized volatility of 1.39%. These are extremely favorable metrics for a 6.54% all-in yield.

The largest portion of the fund SEC yield is provided by risk-free rates. As long as Fed Funds stay high, CLOA will provide very appealing total returns. What we have seen in the past weeks is a sudden shift to less cuts priced for 2024, with the first rate cut now penciled in for June. This translates into an environment of ‘higher for longer’, which makes floating rate assets very attractive. Depending on the number of cuts to be taken in 2024, we are of the opinion that CLOA will end up providing a total return of over 6% for 2024, with de-minimis volatility.

A retail investor interested in floating rate assets with very little credit risk would do well to look at funds such as CLOA, since they represent a smart way to monetize the current floating rate environment.

Although spreads have retraced since their wides, the low fund duration of only 0.16 years translates into the very low observed volatility even when there is a market risk-off event. If we do end up with an ‘immaculate landing’ as the equities markets are seemingly pricing, expect further spread tightening towards the 120 bps historic ‘normalized’ environment level.

Conclusion

CLOA is an AAA CLO exchange-traded fund from BlackRock. Unlike other funds from the behemoth asset manager, CLOA has failed to gain much traction since inception in the beginning of 2023. While witnessing an explosive growth in AUM for its competitor JAAA, CLOA has kept its assets at the $100 million mark. With the market now pricing ‘higher for longer’ in rates, and CLOA benchmarking very favorably from a total return perspective against JAAA, we think investors would be well served to have a second look at this forgotten CLO ETF from BlackRock.