(Bloomberg) — US stocks were poised to open lower after last week’s strong rally as investors assessed the outlook for corporate earnings ahead of key data from the US that may give further clues on the Federal Reserve’s policy path.

Most Read from Bloomberg

Futures on the S&P 500 slipped after Wall Street’s best weekly performance this year. The Stoxx Europe 600 index dipped following nine straight weeks of gains, the longest run in 12 years. Treasury yields ticked higher and the Bloomberg dollar spot index was slightly lower.

Traders are in wait-and-see mode ahead of a busy week of economic data that will include the Fed’s preferred inflation gauge due Friday, when many markets will be closed for a holiday. While conviction has grown that the Fed will cut rates this year following dovish comments by Chair Jerome Powell last week, investors are becoming uneasy about stock valuations after the recent rally.

“When upward catalysts get rare and valuations are rich, risks become visible,” said Jeanne Asseraf-Bitton, head of research and strategy at BFT IM in Paris. “The coming weeks will be more complicated.”

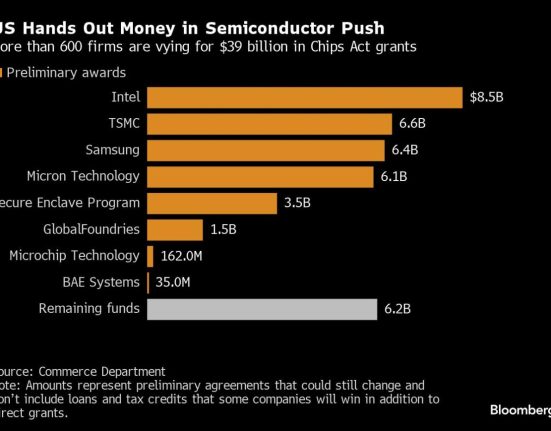

In US premarket trading, Intel Corp. and Advanced Micro Devices Inc. declined after a Financial Times report said China was seeking to limit the use of US-made chips in government computers. United Airlines Holdings Inc shares fell as US aviation authorities mull measures to curb growth at the carrier following a series of safety incidents.

Even after this year’s gains, European equity valuations are not yet over-stretched, according to Goldman Sachs Group Inc. strategists who forecast the Stoxx Europe 600 could still rise about 6% over the next 12 months.

Shares in European defense firms rose following a terrorist attack in Moscow on Friday evening that killed at least 137 people, in an assault claimed by the Islamic State. Dassault Aviation SA climbed 4.5% and Rheinmetall AG was up 3.6%. Swedish landlord SBB jumped after buying back a batch of bonds at a 60% discount, while Direct Line Insurance Group Plc plunged after Ageas said on Friday it won’t make a third takeover offer.

Muted Asia

Asia saw a muted session, led by a drop in Japanese equities following currency warnings by a top official. The yuan climbed amid signs of support from monetary authorities. A regional equity gauge slipped for a second session, with Japan’s Topix index among the worst performers. South Korea’s Kospi index also declined, while Australian shares inched higher.

The offshore yuan rose as the dollar weakened and China’s central bank set a stronger-than-expected daily reference rate. The gap between the yuan’s daily fixing versus estimates was the widest since November, while Bloomberg calculations indicated the People’s Bank of China injected a net 40 billion yuan ($5.56 billion) in open market operations.

Chinese Premier Li Qiang had earlier downplayed investor concerns of challenges facing the economy, saying Beijing was stepping up policy support to spur growth and systemic risks are being addressed. Chinese and Hong Kong stocks edged lower.

In commodities, oil gained on escalating geopolitical unrest following attacks in Russia, as well as positive commentary about the outlook for commodities. Gold was little changed, while iron ore held its largest weekly advance in six months.

Bitcoin rose, boosting shares in cryptocurrency-related stocks in US premarket trading.

Key events this week:

-

Bank of England policymaker Catherine Mann speaks, Monday

-

US new home sales, Monday

-

Fed’s Austan Goolsbee, Lisa Cook, Raphael Bostic speak, Monday

-

ECB chief economist Philip Lane appearance, Tuesday

-

US durable goods, Conference Board consumer confidence, Tuesday

-

Australia CPI, Wednesday

-

Bank of Japan board member Noaki Tamura speaks, Wednesday

-

China industrial profits, Wednesday

-

Bank of Communications, Agricultural Bank of China, China Merchants Bank report earnings, Wednesday

-

Eurozone economic, consumer confidence, Wednesday

-

Bank of England issues financial policy committee minutes, Wednesday

-

Fed’s Christopher Waller speaks, Wednesday

-

Germany unemployment, Thursday

-

UK GDP revision, Thursday

-

US University of Michigan consumer sentiment, initial jobless claims, GDP, Thursday

-

Japan unemployment, Tokyo CPI, Friday

-

France CPI, Friday

-

US personal income and spending, wholesale inventories, Friday

-

Exchanges closed in US and many other countries in observance of Good Friday holiday, Friday

-

Fed’s Jerome Powell, Mary Daly speak, Friday

Some of the main moves in markets:

Stocks

-

S&P 500 futures fell 0.2% as of 6:32 a.m. New York time

-

Nasdaq 100 futures fell 0.3%

-

Futures on the Dow Jones Industrial Average fell 0.2%

-

The Stoxx Europe 600 fell 0.2%

-

The MSCI World index fell 0.1%

-

S&P 500 futures fell 0.2%

-

Nasdaq 100 futures fell 0.3%

-

The MSCI Asia Pacific Index fell 0.5%

-

The MSCI Emerging Markets Index fell 0.3%

Currencies

-

The Bloomberg Dollar Spot Index fell 0.1%

-

The euro was little changed at $1.0818

-

The British pound rose 0.1% to $1.2617

-

The Japanese yen was little changed at 151.33 per dollar

-

The offshore yuan rose 0.3% to 7.2508 per dollar

Cryptocurrencies

-

Bitcoin rose 1.5% to $67,150.3

-

Ether rose 1.5% to $3,465.12

Bonds

-

The yield on 10-year Treasuries advanced three basis points to 4.23%

-

Germany’s 10-year yield advanced two basis points to 2.34%

-

Britain’s 10-year yield advanced three basis points to 3.96%

Commodities

-

West Texas Intermediate crude rose 0.8% to $81.27 a barrel

-

Spot gold rose 0.1% to $2,168.60 an ounce

This story was produced with the assistance of Bloomberg Automation.

–With assistance from Richard Henderson, Julien Ponthus and Michael Msika.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.