By David R. Guttery, RFC, RFS, CAM

President, Keystone Financial Group-Trussville AL

Within my last article, I offered my thoughts about the potential for changing economic seasons in 2024. I would like to emphasize though that these changes will likely develop in fits and starts.

David Guttery

Indeed, straight lines do not occur in nature. Let’s observe the weather that we have now for example. As we emerge from winter into spring, you know we’ll have a string of days where the temperature is in the mid 70’s, the sun is shining, and we begin to see green on the trees again. And then mother nature throws a 30-degree curve ball at us with a late season freeze.

We know that the Earth tilts 23 1⁄2 degrees on its axis. It is this tilt that provides our seasons. We are indeed moving toward the Summer Solstice. One late season freeze does not mean that we’re headed back into winter.

Likewise, emerging from economic winter into economic spring will also bring with it some metaphorical cold snaps along the way. In my opinion, I remain convinced that we are indeed emerging into a new, warmer economic season, and I believe there is plenty of data to support this conclusion.

So, being tactical in our approach to asset allocation, we have to be stoic and dispassionate as we evaluate these metrics and have the intestinal fortitude to proactively move on compelling data.

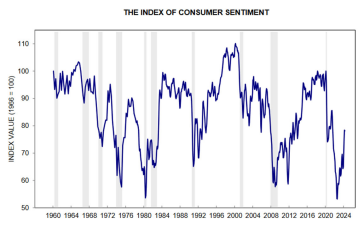

So, what’s compelling about these data metrics? Let’s begin with consumer confidence. In just the last few months, we’ve seen quite a rebound in the confidence of consumers, as evidenced by the University of Michigan consumer sentiment survey.

Within previous articles, I’ve observed that this metric hit an all-time record low reading in November of 2022. With inflation fresh off of a 40-year high, and personal income rising at a declining rate, it was easy to see why. We had never felt more dour about our capacity to spend than we did in November of 2022. We gradually, marginally, painfully emerged from that low point.

But notice that late in the prior year, we had begun to see increasingly higher readings for this metric. Indeed, in December, January, and again in February, we saw the three best months for metric since July of 2021. So, attitudes toward consumption are changing in a

positive way, and quickly.

Why might this be happening? Well, we felt dour in 2022 because our capacity to spend was under inflationary duress.

Why might this be happening? Well, we felt dour in 2022 because our capacity to spend was under inflationary duress.

Today, it appears that the rate of inflationary change has nearly returned to pre-pandemic levels. According to the Department of Labor, the year over year change in personal income has been higher than that of the rate of inflation, and so our capacity to spend has been

increasingly positive since November of 2022.

Discretionary income has been increasingly plentiful as well, and hence why we’re observing patterns of consumption improving.

Aside from sequentially higher retail sales reports, we’re also beginning to see a discernible shift in the ISM Manufacturing Index.

The ISM manufacturing index had been in freefall since March of 2021 until the beginning of the fourth quarter last year. Manufacturers didn’t just decide to stop making things. They responded to you not buying as many things as inflation hit a 40-year high. That in my

opinion gave rise to the recent crisis driven, rapid adoption of technology and the emergence of the magnificent seven stocks last year.

We’ll save that for another article. For now, notice that this trend came to an end in the fourth quarter of last year, and has seemingly reversed. Now, for the first time in well over a year, the index is above 50 which indicates expansion. Clearly, the consumer is buying more things now. This is important because consumption is 70% of Gross Domestic Product, and observing these points of data, you can see how they’re beginning to daisy chain together, and in my opinion, they’re pointing to much better outcome than we had anticipated even just one year ago. We must be stoic in our resolve to proactively manage portfolios in a tactical manner as we observe

this changing data.

Observing market behavior as an indicator as well. We call that stochastic analysis. So, when you hear in the media that markets are bouncing off of strength, or running into resistance, it is to Bollinger Bands that reference is being drawn.

Observing market behavior as an indicator as well. We call that stochastic analysis. So, when you hear in the media that markets are bouncing off of strength, or running into resistance, it is to Bollinger Bands that reference is being drawn.

On the 20th of November, it appeared that the 50 day and the 200 day moving averages were converging within the same cone, so on its

surface, this suggested that the first quarter of 2024 might be very interesting to watch.

On the 1st of December though, we received the minutes of a Federal Open Market Committee meeting, and in my opinion, we heard the same message from the Fed for a 13th month in a row. Over the previous year, markets didn’t metaphorically blink, still reluctant to fully embrace the Fed following the most aggressive removal of accommodation in 45 years. But on this day, the market closed up 580 points. We broke what had been the upper level of resistance. Statisticians tell us that if you breach a barrier, higher or lower, close above or below that level, and continue the trend, then there is a statistically high probability that you’ll re-set that barrier ten to fifteen percent higher or lower than the previously breached level.

Well, here we are today. We’re still searching for what has yet to become that new upper-level band of resistance. So, to your point, yes, I can point to a stochastic analysis of the market to suggest that we are indeed seeing patterns of behavior seemingly changing in a positive manner for the first time, really since the pandemic.

So, in closing, I’d like to offer this high-level advice about how you should approach this year as investors. Be this guy.

So, in closing, I’d like to offer this high-level advice about how you should approach this year as investors. Be this guy.

Stay away from sensationalism and hyperbole. Remain focused on that which can be quantified and find the stoic disposition to act upon data when it begins to point in a certain direction. Remain focused on the fruition of planning goals, and not necessarily on the red or green arrows of the day. Most of all, be patient. Yes, I believe we’re headed for the summer solstice, but you know, August doesn’t immediately follow April. This will unfold gradually over time, and across fits and starts as you put it at the beginning of this video. Remain patiently focused on the bigger picture, be tactical in your approach to asset allocation, while keeping your intestinal fortitude intact. That’s how we get through periods of disproportionate upheaval.

(*) David R. Guttery, RFC, RFS, CAM, is a financial advisor, and has been in practice for 32 years, and is the President of Keystone Financial Group in Trussville. David offers products and services using the following business names: Keystone Financial Group – insurance and financial services | Ameritas Investment Company, LLC (AIC), Member FINRA / SIPC – securities and investments | Ameritas Advisory Services – investment advisory services. AIC and AAS are not affiliated with Keystone Financial Group. Information provided is gathered from sources believed to be reliable; however, we cannot guarantee their accuracy. This information should not be interpreted as a recommendation to buy or sell any security. Past performance is not an indicator of future results. Examples are for illustrative purposes only and should not be considered representative of any investment. Investments involve risks, including loss of principal.