As baby boomers age, an inheritance wave dubbed the “great wealth transfer” is underway. What’s also ahead: a great debt transfer that will have to be managed by younger generations of Americans.

More than 46% of Americans expect to transfer debt on death to their loved ones, according to a survey by PolicyGenius. The average American household owes $10,000 in credit card debt, $58,957 in student loan debt, $241,840 in mortgage debt, and $22,612 in auto loans.

“Debt does not miraculously disappear when someone passes away, and any outstanding debt is paid out of assets like property, retirement accounts, and bank accounts,” Rosalyn Glenn, a financial planner for Prudential, told Yahoo Finance. “If you have assets, your debt can be transferred at death, and if you don’t have a plan for managing the debt, you leave your family at risk.”

As many make New Year’s resolutions about their health, it is a good time to check the state of your wealth — especially life insurance coverage — so instead of transferring debt to loved ones, your legacy is one of financial stewardship and wealth building.

“Unfortunately, there have been cases where families were displaced because of the loss of income and the inability of the surviving spouse to maintain the mortgage on a single income,” Glenn said.

Life insurance to mitigate transferring debt

Among the share of Americans who expect to leave debt behind when they die, 21% do not have life insurance, PolicyGenius found.

“One of the advantages of life insurance is it provides security in case a loved one dies and leaves you responsible to pay any jointly owned debt, such as a mortgage,” Shardéa Ages, a certified financial planner at Collective Wealth Partners, told Yahoo Finance. “And the best part is that life insurance proceeds are tax-free, in most cases.”

When it comes to student loan debt, much depends on whether the debt is federal versus private loans.

“Federal student loans are forgiven upon the death of the borrower, but some types of student loans issued by private lenders can be passed onto loved ones upon the death of the borrower, especially if the loan was co-signed,” Jessica Ruggles, corporate vice president of financial wellness at New York Life, told Yahoo Finance.

Disparities in wealth — and debt

The PolicyGenius study found that households with more than $150,000 in income had more debt than lower-income households, but higher-income households were better prepared to help loved ones pay off those debts. Only 13% in the higher income group had no life insurance, compared to 31% of lower income households.

The study also found racial disparities in debt, which contribute to the racial wealth gap, noting “Black and Hispanic Americans have a harder time accessing credit to make larger purchases, like real estate, that can help them build wealth and pass it down to future generations.”

Homeownership and life insurance proceeds are generally how most people pass on generational wealth to family members.

Black homeownership stands at 45.5%, and during the housing pandemic boom many Black homeowners missed out on the refinance opportunities to access equity and lost equity on home sales due to appraisal bias.

Hispanic homeownership is slightly higher at 48.6%, but still lags behind white homeownership at 74%.

Many Black and Hispanic households are also missing out when it comes to life insurance.

Around 56% of Black Americans have life insurance, but many are underinsured, meaning their benefits are not enough to replace income or provide wealth transfers across generations due a misunderstanding of how life insurance works and a mistrust of the industry at large.

Only 42% of Hispanics have a life insurance policy, with trust issues, language barriers, and cultural differences keeping Hispanics from getting life insurance, a critical cash infusion that could help close the wealth gap in the Hispanic community.

Adding to the problem is a lack of representation among financial planning professionals: Only 1.8% of certified financial planners (CFPs) are Black and 2.7% are Hispanic.

Life insurance protection during life

Although most conversations about life insurance center around death, some life insurance policies have benefits that can be used during the lifetime of the policyholder.

“Life insurance is for the living too,” Glenn said.

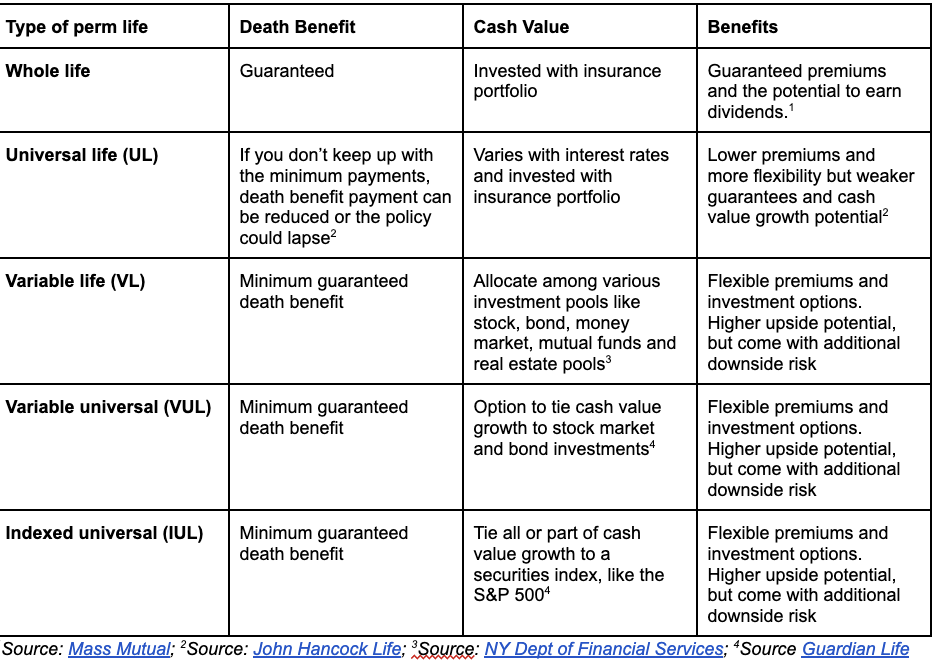

Unlike term life insurance, a permanent life insurance policy lasts your lifetime and earns tax-deferred cash value in addition to the death benefit. The cash value can be used during the policyholder’s lifetime in the form of a loan or withdrawal.

More Americans are tapping their permanent life insurance policies to help them weather inflation and avoid drawing on retirement accounts.

Financial planners commonly recommend a combination of term life and permanent life insurance policies.

Read more: Your step-by-step guide to filing a life insurance claim

It is important to have regular check-ins on your financial health, adjusting your financial plans with life changes such as births, deaths, divorce, and health challenges.

Ronda is a personal finance senior reporter for Yahoo Finance and attorney with experience in law, insurance, education, and government. Follow her on X @writesronda