Investors should look for broken stocks, not broken companies. That’s one of my favorite investment rules, and successfully following it can make you a lot of money. So, which label applies to coffee chain giant Starbucks (NASDAQ: SBUX)?

The stock has suffered an extended slide and is over 40% off its former high after a poor reception to its fiscal second-quarter earnings report. The current drop is the worst since the financial crisis in 2008.

There’s no doubt Starbucks is struggling, but there are some essential facts to know before you write the company off. In fact, Starbucks could be a buy-and-hold forever stock, despite its current headaches.

Starbucks’ struggles aren’t unique

A glance at Starbucks’ fiscal 2024 Q2 results tells a pretty quick and convincing story. The number of companywide transactions slipped 6% year over year in the quarter, and international sales, where China is a big part of the company’s growth strategy, fell 6%. Management dramatically lowered its guidance for full-year revenue growth from between 7% and 10% to the low single-digit range.

The coffee chain appears to be cracking in the face of macroeconomic uncertainty. During the earnings call, CEO Laxman Narasimhan noted, “In a number of key markets, we continue to feel the impact of a more cautious consumer, particularly with our more occasional customer. And a deteriorating economic outlook has weighed on customer traffic, an impact felt broadly across the industry.”

Fellow consumer-facing brand McDonald’s also missed analysts’ earnings estimates for its most recent quarter. Management similarly spoke about how consumers are pulling back on their spending.

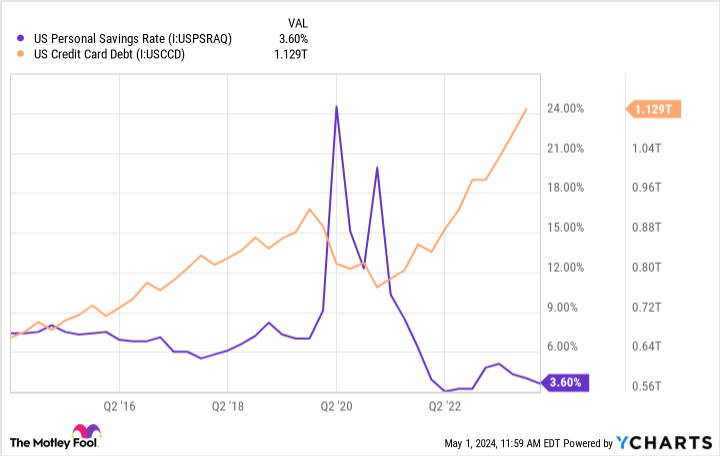

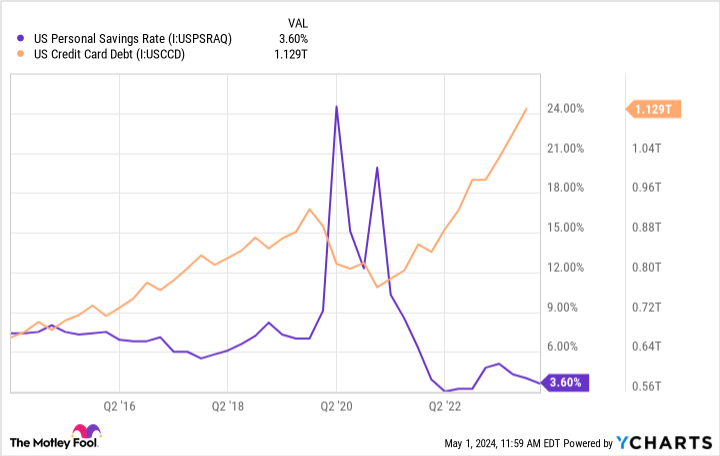

A meal or coffee on the go is a luxury many people will give up as finances get tight. Consumer credit card debt is at an all-time high, and household savings rates are near decade lows. Meanwhile, inflation has been stubborn in recent months, supporting the notion that people are struggling to make ends meet.

The good news is that this isn’t an indictment of Starbucks as a business or brand — people are closing their wallets across the board. This temporary storm should pass as the economic cycle turns and consumers get back on their feet.

Focus on the fundamentals

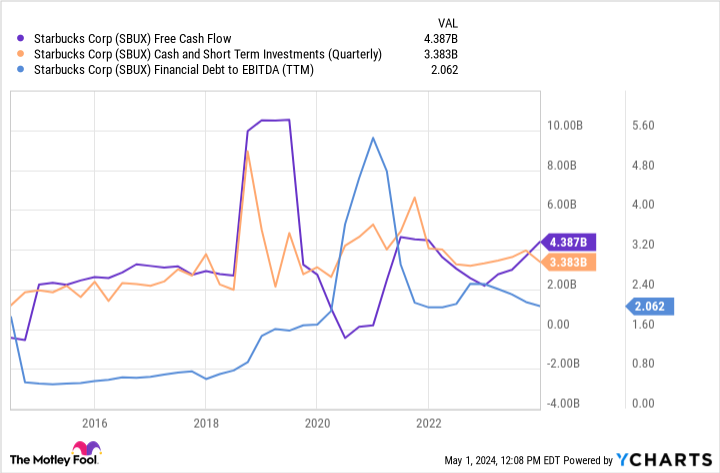

Investors should be aware of these headwinds but keep their eye on Starbucks’ fundamentals. This is where the business shines. Remember that revenue should still grow this year, even if it’s not by as much as initially expected. Starbucks also grew its U.S. rewards program 6% year over year to 32.8 million members last quarter. The company is a financial stalwart with over $3 billion in cash on its balance sheet and a leverage ratio of just 2 times EBITDA.

Don’t forget the company’s ability to return cash to shareholders. Starbucks is a solid dividend growth stock — the company has raised its dividend for 14 consecutive years, while its payout ratio sits at a healthy 63%. Meanwhile, the company has repurchased enough stock to lower its share count 6% over the past five years, boosting earnings per share.

Starbucks might temporarily feel consumers pulling back, but the business is still fantastic.

An attractive price thanks to the drop

Great companies are rarely cheap, which is partly why investors should look closely at blue chip stocks like Starbucks when they stumble. It could be a rare buying opportunity. Starbucks trades at a forward price-to-earnings (P/E) of 22 after falling 41% from its previous high.

Analysts believe the company will grow earnings an average of about 15% annually over the next three to five years. For 22 times earnings, investors can get double-digit earnings growth, a growing dividend that yields 3%, and a financially stable business that has endured multiple downturns throughout its history.

Consumers are struggling right now, but that won’t last forever. Starbucks’ discounted valuation makes for an excellent starting point for solid long-term returns.

Should you invest $1,000 in Starbucks right now?

Before you buy stock in Starbucks, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Starbucks wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $544,015!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 30, 2024

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Starbucks. The Motley Fool has a disclosure policy.

1 Magnificent S&P 500 Dividend Stock Down 41% to Buy and Hold Forever was originally published by The Motley Fool