Best Personal Loan Rates Of 2025

BEST LOW-RATE LOAN FOR CO-SIGNED LOANS

Upgrade

Editor’s Take

Upgrade is an online lender that offers personal loans and other financial products to borrowers with bad credit.

Why We Like It

Upgrade lets prospective borrowers apply with a co-applicant, making it easier to qualify for its lowest advertised interest rates.

What We Don’t Like

Borrowers pay origination fees between 1.85% and 9.99% of the total loan amount, increasing the overall cost of borrowing.

Who It’s Best For

Upgrade personal loans are best for borrowers looking to apply for a personal loan with a co-applicant.

Consumer Sentiment Index

Pros & Cons

- Fair credit accepted

- Rate discounts for using autopay and for using loans to pay off existing debt

- Free credit health monitoring

- Origination fees

- Potentially high interest rates

Details

Eligibility

- Minimum credit score: 620620

- Co-applicants: Permitted

- Direct pays third-party creditors: Yes

Customer service

We called Upgrade to gauge the responsiveness of its customer service team and found it to be one of the most responsive lenders on our list. While we waited just over one minute for their team to answer our call—which is not the fastest time—they were transparent and knowledgeable about Upgrade’s loans.

We received information on loan amounts, required documentation, interest rate ranges, approval speed, fees and various perks, like hardship programs and autopay discounts. The representative also confirmed that they report payments to credit bureaus.

Personal loans made through Upgrade feature Annual Percentage Rates (APRs) of 7.99%-35.99%. All personal loans have a 1.85% to 9.99% origination fee, which is deducted from the loan proceeds. Lowest rates require Autopay and paying off a portion of existing debt directly. Loans feature repayment terms of 24 to 84 months. For example, if you receive a $10,000 loan with a 36-month term and a 17.59% APR (which includes a 13.94% yearly interest rate and a 5% one-time origination fee), you would receive $9,500 in your account and would have a required monthly payment of $341.48. Over the life of the loan, your payments would total $12,293.46. The APR on your loan may be higher or lower and your loan offers may not have multiple term lengths available. Actual rate depends on credit score, credit usage history, loan term, and other factors. Late payments or subsequent charges and fees may increase the cost of your fixed-rate loan. There is no fee or penalty for repaying a loan early. Personal loans issued by Upgrade’s bank partners. Information on Upgrade’s bank partners can be found at https://www.upgrade.com/bank-partners/.

BEST LOW-RATE LOAN FOR QUICK FUNDING

LightStream

APR range

6.49% to 25.29%

with autopay

6.49% to 25.29%

with autopay

Editor’s Take

In addition to low interest rates, LightStream offers personal loans from $5,000 to $100,000 with fast funding.

Why We Like It

LightStream’s loan application process can be completed online with funds available as soon as the same day of approval.

What We Don’t Like

LightStream’s personal loans start at $5,000, which is a higher minimum loan amount than what many competitors offer.

Who It’s Best For

LightStream personal loans are best for borrowers who need a large loan and fast access to funds.

Consumer Sentiment Index

Pros & Cons

- No origination fee

- Rate discounts for using autopay

- High loan amounts and extended terms

- No feature to direct pay creditors

- No option to prequalify without a hard inquiry

Details

Eligibility

- Minimum credit score: 660

- Co-applicants: Permitted

- Direct pays third-party creditors: No

Customer service

We tried to call LightStream to test the quality of its customer service, but they don’t provide a customer service number. If you want to reach their customer service team, you must contact them via email. Its email support is available Monday through Friday, 9:30 am to 7 pm and Saturday, 12 to 4 pm ET.

BEST LOW-RATE LOAN FROM A TRADITIONAL BANK

U.S. Bank

APR range

7.99% to 24.99%

with autopay

Loan amounts

$1,000 to $50,000 for existing U.S. Bank customers and up to $25,000 for new customers

Depends on the area you live in

7.99% to 24.99%

with autopay

$1,000 to $50,000 for existing U.S. Bank customers and up to $25,000 for new customers

Depends on the area you live in

Editor’s Take

As a traditional financial institution, U.S. Bank offers personal loans available online and through its more than 2,000 branches in 26 states.

Why We Like It

U.S. Bank offers high maximum loan amounts and lengthy repayment terms to current customers.

What We Don’t Like

Prospective borrowers must have a credit score of 720, and fewer borrowing options are available to those without a U.S. Bank account.

Who It’s Best For

U.S. Bank personal loans are best for current customers, as having a checking account with the bank allows borrowers to access higher borrowing amounts and longer repayment terms.

Consumer Sentiment Index

Pros & Cons

- No origination fees or late fees

- Low interest rates

- Rate discounts for using autopay

- Strong credit necessary

- Doesn’t directly pay third-party creditors

Details

Eligibility

- Minimum credit score: 720

- Co-signers: Permitted

- Direct pays third-party creditors: No

Customer service

We called U.S. Bank’s customer service team to test its quality. Compared to other lenders on our list, we waited the second longest for our call to be answered—two minutes and one second. Although the representative was friendly and transparent, they provided most of the information through a sales pitch, which may be unsettling to some prospective borrowers.

U.S. Bank was one of few lenders that provided a specific interest rate based on loan details we provided. While the rep didn’t ask for a credit score to provide the interest rate, you need a score of at least 720 to qualify. The lender’s website discloses you need a score of at least 800 to access the lowest rates.

BEST LOW-RATE LOAN FOR LIMITED CREDIT HISTORY

Upstart

Editor’s Take

As an AI-based lending platform, Upstart offers loans based on non-traditional lending standards like education and employment.

Why We Like It

Upstart’s minimum credit score requirement of 620 makes it an accessible option to borrowers with bad or thin credit.

What We Don’t Like

Upstart charges borrowers origination fees between 0% and up to 12% of the total loan amount, which is higher than other lenders.

Who It’s Best For

Upstart personal loans are best for borrowers who have limited credit history and want small personal loans.

Consumer Sentiment Index

Pros & Cons

- Accessible to borrowers with no credit history

- Prequalification with a soft credit check

- Ability to choose a custom payment date

- Charges an origination fee up to 12% of the loan amount

- No co-signer option

- Only offers three- or five-years terms

Details

Eligibility

- Minimum credit score. 620

- Minimum income. No minimum but must have a source of income

- Co-signers. Not permitted

- Co-borrowers. Not permitted

Customer service

We tested Upstart’s customer service quality to evaluate its helpfulness. Through our research, we found Upstart’s team was one of the fastest to answer, as we waited only 39 seconds. However, once connected, the representative was vague. While they disclosed general loan details like loan amounts, fees and interest rate ranges, they were unclear about documentation requirements and approval times.

BEST LOW-RATE LOAN FOR DEBT CONSOLIDATION

Discover

Editor’s Take

Discover personal loans are available from $2,500 to $40,000 and come with terms between three and seven years.

Why We Like It

Not only can borrowers use Discover personal loans to consolidate multiple debts, but the lender can also send loan proceeds directly to creditors.

What We Don’t Like

Discover doesn’t provide a rate discount for autopay and sets a high minimum credit score requirement of 660 .

Who It’s Best For

Discover’s personal loans are best for borrowers who want to reduce their interest costs with a debt consolidation loan.

Pros & Cons

- No origination fees

- Low interest rates

- Direct creditor payoff with debt consolidation loans

- No interest rate discount for automatic payments

- No co-signers or co-borrowers accepted

- Good credit needed to qualify

Details

Eligibility:

- Minimum credit score required. 660

- Minimum annual income. $25,000

- Co-borrowers. Not permitted

- Co-signers. Not permitted

It’s no surprise that Discover personal loans are popular. Discover was the original rewards credit card with a large, diverse customer base. It utilizes its app and website to make the application process easy (especially for existing customers). In some cases, the funds are available the next day. Discover doesn’t have an application fee and is flexible with repayment options. The entire process is consistent with the brand and experience Discover’s customers are familiar with.

— Herman Thompson, Jr., advisory board member

BEST LOW-RATE LOAN FOR FAIR CREDIT

LendingPoint

APR range

7.99% to 35.99%

with autopay

7.99% to 35.99%

with autopay

Editor’s Take

LendingPoint is an online lender that offers personal loans for a range of purposes with low minimum APRs.

Why We Like It

LendingPoint personal loans are available to borrowers with credit scores of 600 or higher.

What We Don’t Like

LendingPoint charge’s high maximum APRs and origination fees up to 10%, which comes out of the loan amount.

Who It’s Best For

LendingPoint is best for borrowers with bad to fair credit or those who can qualify for the lowest advertised rates.

Consumer Sentiment Index

Pros & Cons

- Quick funding

- Low credit score requirements

- No prepayment penalty

- Origination fee up to 10%

- Co-signers or joint loans not permitted

- Not available in Nevada and West Virginia

Details

Eligibility:

- Minimum credit score. 600

- Minimum annual income. $35,000

- Co-signers. Not permitted

Customer service

After testing and evaluating LendingPoint’s customer service, we found it to be one of the most helpful and transparent lenders on our list after waiting only 46 seconds to be connected to a representative. The customer service representative we spoke with shared an in-depth perspective of their loan offers, including information about loan amounts, eligibility requirements, how interest rates are determined and prequalification.

LendingPoint’s team also disclosed late fees but didn’t confirm origination fees. While customer service didn’t share this information wasn’t, the lender discloses a fee of up to 10% on its website. LendingPoint was also one of few lenders that shared how they report payments to credit bureaus, which it typically does at the start of the month.

BEST LOW-RATE LOAN FOR LARGE AMOUNTS

Wells Fargo

APR range

6.99% to 24.49%

with autopay discount

6.99% to 24.49%

with autopay discount

Editor’s Take

Wells Fargo is a solid option for customers with an established relationship with the bank, thanks to high maximum loan amounts and a relationship discount.

Why We Like It

Wells Fargo offers fixed-rate personal loans between $3,000 to $100,000 and repayment terms from one to seven years.

What We Don’t Like

Only current Wells Fargo customers can apply for a personal loan online. Likewise, the 0.25% autopay discount is only available to current customers.

Who It’s Best For

Wells Fargo personal loans are a good choice for borrowers who need access to large loans, as personal loans are available up to $100,000.

Consumer Sentiment Index

Pros & Cons

- Can receive funds as soon as the next business day

- 0.25% autopay discount

- No origination fees or prepayment penalty

- Must have a Wells Fargo checking account to receive autopay discount

- New Wells Fargo customers must visit a branch to apply

- No option to prequalify

Details

Overview: Wells Fargo offers fixed-rate personal loans with limits between $3,000 to $100,000 and repayment terms from 12 to 84 months. Although Wells Fargo is available to anyone in the United States, only current Wells Fargo customers will be able to apply online.

New customers will need to visit a branch location. Wells Fargo does not have branch locations in Indiana, Kentucky, Louisiana, Ohio, Oklahoma, Maine, Massachusetts, Michigan, Missouri, New Hampshire, Vermont or West Virginia.

Eligibility:

- Minimum credit score. Does not disclose

- Minimum income. Does not disclose

- Co-borrowers. Not permitted

Loan uses:

- Debt consolidation

- Home improvement

- Medical bills

BEST LOW-RATE LOAN FOR WELL-QUALIFIED APPLICANTS

American Express® Personal Loans

Editor’s Take

In addition to its credit card options, American Express offers cardholders personal loans from $3,500 to $40,000.

Why We Like It

American Express personal loans charge APRs between 5.91% to 17.97%—which is lower than most competitors.

What We Don’t Like

Minimum and maximum loan amounts are less flexible than some competitors and may lead to borrowing more than necessary.

Who It’s Best For

American Express personal loans are best for borrowers who can qualify for the lowest advertised rates.

Pros & Cons

- Low advertised APRs

- No origination fees

- Quick loan decision

- Can’t change payment due date

- Only available to current cardmembers

- Doesn’t allow co-signers or co-applicants

Details

Eligibility:

- Minimum credit score required. Does not disclose

- Minimum annual income. Does not disclose

- Co-borrowers. Not permitted

- Co-signers. Not permitted

Compare the Best Personal Loan Rates

The above personal loan rates and details are accurate as of March 3, 2025. While we update this information regularly, the annual percentage rates (APRs) and loan details may have changed since the page was last updated. Keep in mind, some lenders make specific rates and terms available only for certain loan purposes. Be sure to confirm available APR ranges and loan details, based on your desired loan purpose, with your lender before applying.

Tips for Comparing Personal Loan Rates

In general, annual percentage rates (APRs) vary by lender and depend on several factors, including the applicant’s creditworthiness. However, there are several things you can do to access the lowest rate possible when applying for a personal loan. Consider these factors when comparing personal loan rates:

Credit score and eligibility requirements.

Average borrower rates.

Loan amounts and repayment terms.

Additional costs.

-Colin Beresford, Deputy Editor Personal & Business Loans

What Is a Personal Loan?

A personal loan is a type of financing that lets borrowers access cash for a wide range of personal uses, including home improvements, auto repairs and unanticipated expenses. Loan amounts and repayment terms vary by lender, but the best personal loans typically range from $1,000 to $100,000 with some starting as low as $250. In general, loan repayment terms extend from one to seven years.

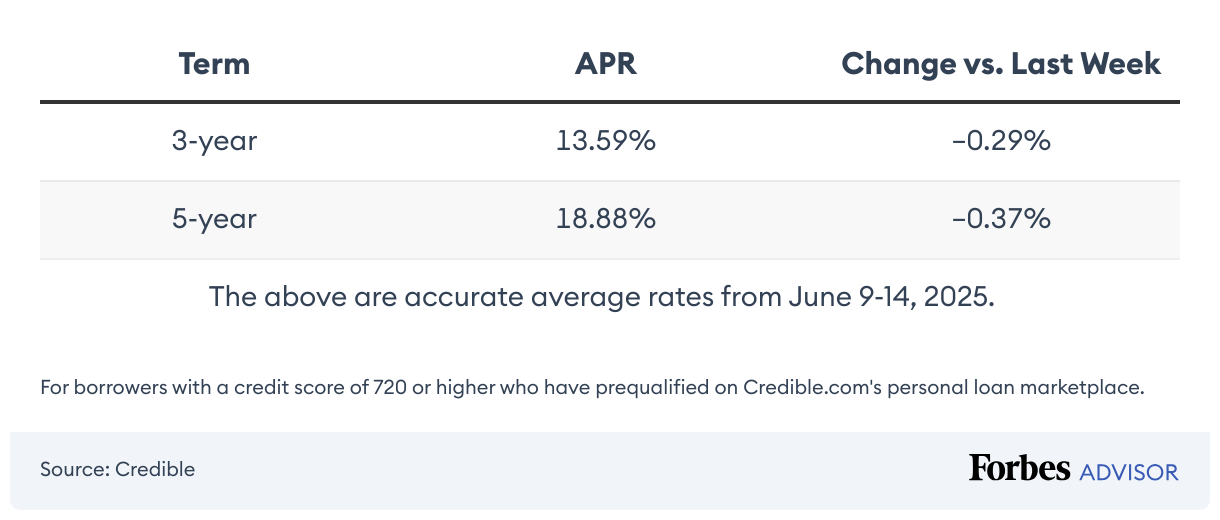

Current Personal Loan Interest Rates

Personal Loan Rates Over Time

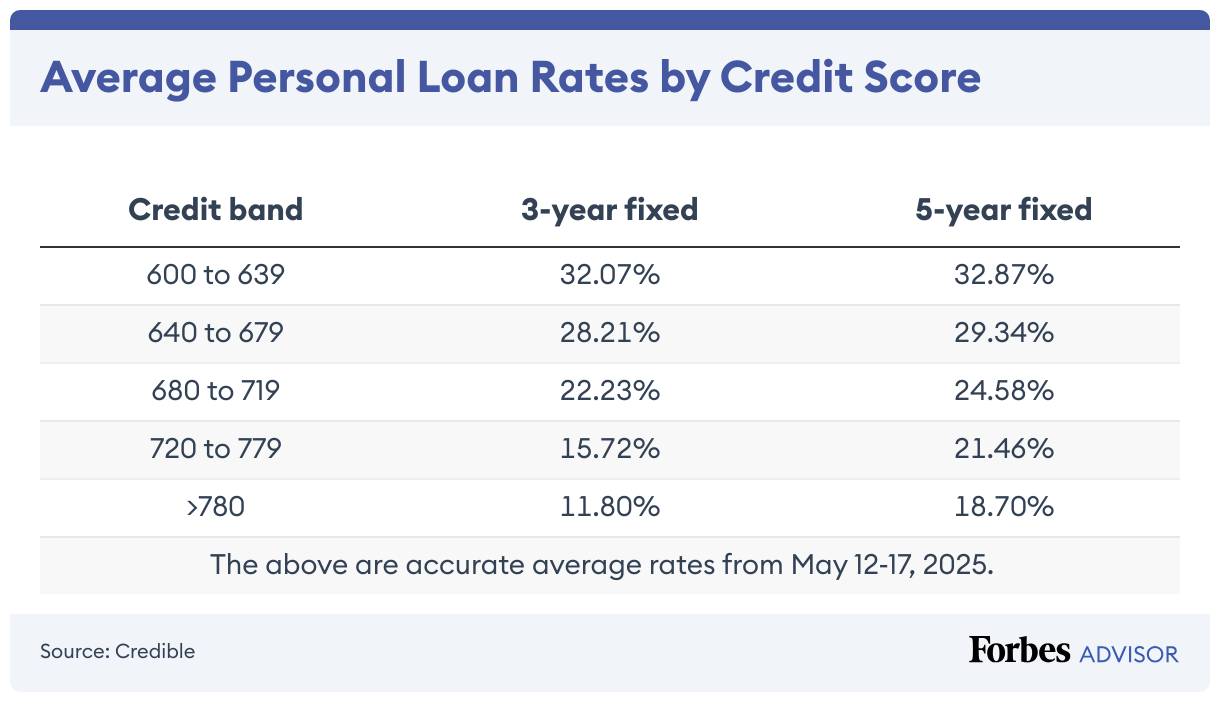

Average Personal Loan Interest Rates By Credit Score

Interest rates vary by lender, borrower qualifications and loan characteristics. However, interest rates are best predicted by a borrower’s credit score.

Personal Loan Rates for Excellent Credit

Personal Loan Rates for Good Credit

Personal Loan Rates for Fair Credit

Personal Loan Rates for Bad Credit

How Lenders Determine Personal Loan Rates

Lenders determine personal loan rates based on several factors, but the applicant’s credit score and overall credit profile are the most important. Many traditional and online lenders also look at the prospective borrower’s income and current outstanding debts to determine their debt-to-income ratio (DTI).

DTI is the ratio of a borrower’s monthly income to their monthly debt service and is used to evaluate an applicant’s ability to make on-time payments. The higher the DTI, the riskier the borrower—and the higher the interest rate they’ll likely receive.

When determining personal loan rates, some online and alternative lenders also look at a prospective borrower’s occupation and education to evaluate earning potential. Likewise, lenders may evaluate the risk posed by a borrower based on where they live.

Pro Tip

It’s always a good idea to prequalify for several loans before choosing one. Many lenders let you prequalify without a hard credit inquiry so you can check and compare rates. However, if you accept a loan offer, the full application process typically includes a hard credit check that may impact your score. Hard inquiries typically stay on your credit report for up to two years.

How To Get the Lowest Personal Loan Rates

The most competitive personal loan rates are typically reserved for the most creditworthy borrowers. However, other factors can impact rates, and it’s possible to get lower rates without a stellar credit profile. Follow these tips to get the best personal loan rates:

- Understand your credit report. Before prequalifying or applying for a personal loan, request a copy of your credit report from one of the three main credit bureaus—Equifax, Experian and TransUnion. You can get free weekly credit reports from AnnualCreditReport.com. Knowing your credit score can help you prequalify for a loan offer before committing to a hard credit inquiry.

- Calculate the best loan amount and term. Personal loan APRs are generally higher for larger loans and more extended repayment terms. That said, shorter repayment terms mean larger monthly payments. Use a personal loan calculator to determine how much monthly payment you can afford, and then opt for the shortest possible loan term.

- Apply with a co-signer or co-borrower. If you won’t qualify for a competitive APR based on your credit, consider applying with a co-borrower or co-signer who has a higher credit score. This approach can lead to higher approval odds and lower personal loan rates.

- Choose a secured loan. A secured personal loan is collateralized by a valuable asset, such as real estate. If a borrower defaults on a secured loan, the lender can seize the collateral. Because secured loans are less risky to lenders, they may be a better fit for borrowers who can’t qualify for a personal loan or a competitive APR.

- Take advantage of rate discounts. Many lenders offer rate discounts to borrowers who sign up for automatic payments during the loan application process. When comparing lenders, choose an option that offers autopay discounts or other savings opportunities.

- Opt for a fee-free lender. To remain competitive, some lenders moved to a fee-free structure that charges no origination, late payment, prepayment or other additional fees. Choosing a fee-free lender can reduce the overall cost of a loan, thereby reducing the APR.

Pros and Cons of Personal Loans

Before taking out a personal loan to consolidate debt or finance your next purchase, it’s a good idea to run through the pros and cons. Below are the advantages and disadvantages of personal loans you should be aware of.

Pros of Personal Loans

- Flexible loan amounts

- Unsecured loans typically require no collateral or down payment

- Fixed installment payments

- Can qualify for low interest rates

- Loan funding may happen in a week or less

- Funds can be used to pay for almost any type of legal personal expense

Cons of Personal Loans

- Loans may have origination fees

- Collateral may be required if you don’t have good credit

- Borrowers with less-than-perfect credit may qualify for higher interest rates

- Loans can damage your credit history if you don’t make on-time payments

- Late payment fees or prepayment penalties may increase the cost of the loan

Where To Get a Personal Loan

Various lenders offer personal loans and some may be better suited for you and your financial needs. Before accepting a loan, consider

How To Get a Personal Loan

Although the process can vary by lender, you’ll generally take these steps in order to get a personal loan:

- Check your credit. Before starting your search for lenders, check your credit score for free through your credit card issuer or another service. This will help you narrow down which lenders will be willing to work with you.

- Improve your credit. If your credit score is lower than 610, take steps to improve your credit score such as lowering your credit usage or paying off debts. This can help you qualify for a loan and, in some cases, a lower interest rate.

- Shop around for lenders. Determine how much money you need to borrow and which lenders whose qualification requirements you meet. Many lenders will let you pre-qualify before submitting a formal application, which allows you to see the rates you could qualify for without impacting your credit score.

- Submit an application. Once you find the lender that works best for you, submit an application. Depending on the lender, this can take hours or days.

Recap: Best Personal Loan Interest Rates of 2025

Methodology

We reviewed 31 popular lenders based on 16 data points in the categories of loan details, loan costs, eligibility and accessibility, customer experience and the application process. We chose the best lenders based on the weighting assigned to each category:

- Loan costs. 35%

- Loan details. 20%

- Eligibility and accessibility. 20%

- Customer experience. 15%

- Application process. 10%

Within each major category, we also considered several characteristics, including available loan amounts, repayment terms, APR ranges and applicable fees. We also looked at minimum credit score requirements, whether each lender accepts co-signers or joint applications and the geographic availability of the lender. Finally, we evaluated each provider’s customer support tools, borrower perks and features that simplify the borrowing process—like prequalification options and mobile apps.

Where appropriate, we awarded partial points depending on how well a lender met each criterion.

To learn more about how Forbes Advisor rates lenders, and our editorial process, check out our Personal Loans Rating & Review Methodology.

Frequently Asked Questions (FAQs)

How much can you borrow with a personal loan?

How large of a personal loan you can borrow depends on what the lender offers and your own creditworthiness. It’s possible to find lenders offering a wide range of loan amounts from a few hundred dollars up to $100,000.

When you apply with a lender, they’ll consider several different factors to figure out how much to approve you for. This could include your credit score, monthly income, other debt obligations and overall credit history.

How much will a personal loan cost?

The cost of a personal loan depends on the lender, type of loan and the borrower’s creditworthiness. Interest typically accrues on personal loans at a rate from 4% to 36%, with the lowest rates accessible to high-credit borrowers. In addition to interest, some lenders also charge origination fees between 1% and 8% of the total loan amount. Borrowers also may be subject to late payments fees and/or prepayment penalties, which can increase the total cost of the personal loan.

How does a personal loan affect your credit score?

A personal loan can have both a negative and positive impact on your credit score. To qualify for most personal loans, you’ll have to undergo a hard credit inquiry, which can temporarily impact your credit score. Once you begin repayment, most lenders will report your payment history to the credit bureaus. On-time payments can help improve your credit, while late payments can drop your credit score.

What’s the difference between APR and interest rate?

The main difference between APR versus interest rate is that the interest rate is the actual cost to borrow money. In contrast, a loan’s annual percentage rate includes the interest rate plus additional costs like finance charges as the annual cost over the life of the loan.

Can I negotiate personal loan rates with lenders?

In some cases, you may be able to negotiate with lenders to get a lower interest rate on your personal loan. Call and ask the lender if you can lower your interest rate, and if that doesn’t work, refinancing your loan may be the best option for securing a lower interest rate.

Can I get a personal loan with bad credit?

It is possible to get a personal loan with bad credit, but it is generally more difficult to qualify—especially for competitive rates. Less creditworthy applicants also face lower borrowing limits and higher interest rates than more qualified applicants. However, some lenders specialize in personal loans for borrowers with bad credit, instead basing lending decisions on alternative credit data.

What is a good interest rate on a personal loan?

Personal loan rates range from around 7% to 36%, with the average hovering around 12-15% for a 3-year loan. A good interest rate on a personal loan is one that is lower than the national average. However, borrowers with excellent credit scores may qualify for even lower rates.