JOY PAN/iStock via Getty Images

Introduction

I still think there are interesting opportunities in the regional banking sector, and one of the smaller banks I have a long position in is Flushing Financial (NASDAQ:FFIC), a New York focused regional bank. Although the bank’s earnings are weaker than I would like, I have a long-term outlook for my investments and in the regional banking sector I’m mainly interested in the quality of the loan book to make sure the vast majority of the loans continue to perform as expected.

The earnings are definitely under pressure

In the first quarter of 2024, Flushing Financial saw its interest (and dividend income) increase by almost 20% to just under $110M but unfortunately that almost $18M increase was cancelled out by a $21.3M increase in the interest expenses. The verdict? A decrease of the net interest expenses by almost $3M to $42.4M.

FFIC Investor Relations

On top of that, the bank recorded a $0.8M loss related to the fair value adjustments of certain items, which wasn’t very helpful either as FFIC was able to record a $2.6M gain in that segment in Q1 2023. All these elements combined resulted in a decrease of the non-interest income to just $3.1M, while the non-interest expenses increased by almost 2% to $39.9M.

The silver lining is the substantial decrease of the loan loss provisions. As the income statement (shown above) shows, the total provision for credit losses decreased from $7.5M to $0.6M. And that definitely helped to avoid seeing the bank reporting a net loss. Indeed, the pre-tax income decreased to just $5M while the net profit was $3.7M for an EPS of $0.12. And that’s a very disappointing result as we can’t even point a finger at the FDIC payments as those increased to $1.65M in Q1 2024 compared to $1M in Q1 2023. Sure, that is an increase of $0.65M, but this wouldn’t have made a major difference in the greater scheme of things, although the company would have been able to report a pre-tax profit increase.

The weak result in the first quarter of the year also means the quarterly dividend was not covered. Flushing Financial is currently paying a quarterly dividend of $0.22 per share and although that dividend was covered in Q2-4 2023, it wasn’t covered in Q1 2024. That being said, a lower FDIC payment and avoiding the loss on fair value adjustments would already go a long way towards reporting a higher net profit in the next few quarters.

Keeping an eye on the quality of the loan book

As mentioned in the introduction, a bank’s earnings are only one reason why I would be interested in being a shareholder. In Flushing’s case, I was mainly attracted to the low LTV ratio in the bank’s real estate loan portfolio and when I added to my position in Q1 last year, the low LTV ratio was one of the main reasons for me to consider that long position in Flushing Financial.

The low loan loss provisions recorded in the first quarter were encouraging, and I hoped this meant the loan book didn’t cause any unexpected headaches. As you can see below, about 40% of the bank’s loan book consists of residential real estate (and about 50% if you’d also include mixed-use properties) with about 30% earmarked for commercial real estate.

FFIC Investor Relations

And as you can see below, only $37.3M of the total loan book was classified as ‘past due’. That’s a small decrease compared to the end of last year and although this represents in excess of 0.5% of the total loan book, I’m still not worried, mainly due to the low LTV ratio in the loan portfolio.

FFIC Investor Relations

First of all, the portfolio already contains about $40.8M in accumulated loan loss provisions. So even in the very unlikely event Flushing Financial wouldn’t recoup a single dollar of the total amount of the loans past due, the current amount of provisions are sufficient to cover the fallout.

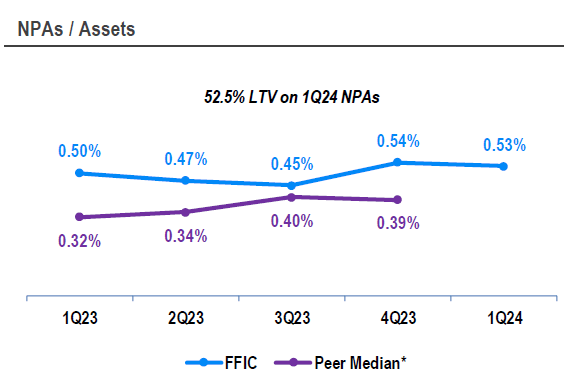

But again, I don’t expect Flushing Financial to record major losses on its loan portfolio. As the image below shows, the average LTV ratio on the non-performing assets was approximately 52.5%. So even if the bank would only get 50 cents on the dollar in a fire sale of the assets, it would keep its average losses limited to just a few million dollars as it would recoup 50/52.5 = 95.2% of its loan size.

FFIC Investor Relations

Another interesting feature is the fact that none (literally, zero percent) of the commercial real estate loans are currently past due, not even by 31 days. This means the bank should focus on managing its residential real estate loan book and keep a close eye on developments in that subset of the loan book.

FFIC Investor Relations

The total loan book has an average LTV ratio of just 36%, so I am still not worried about Flushing Financial’s loan book quality. In fact, as the bank is able to deal with the loans that are currently past due, it should restore the market’s confidence in its ability to manage the loan book and handle defaults.

FFIC Investor Relations

Also, important: none of the loans issued in the multiresidential and commercial real estate segment had an LTV ratio of in excess of 75%.

Let’s also not forget the bank should see an increasing net interest income as between now and the end of 2026, a total of $2.1B in loans will be repriced at an average of in excess of 200 bp. This means that by the end of this year alone the 212 bps mark-up on $583M of loans will represent an additional annualized interest income of $12.3M which would have a very positive impact on the bank’s bottom line.

FFIC Investor Relations

And by the end of next year, even assuming the $767M in loans up for repricing in 2025 are repriced at a 150 bps markup instead of 224 bps, that would add another $11.5M and likely $8M in after-tax profit.

Investment thesis

2024 won’t be a great year for Flushing Financial as the bank gets hit by the decreasing net interest margin. However, as $583M in loans will have to be repriced in the remainder of this year, followed by $767M in loans in 2025, I think we are nearing the end of the NIM compression.

Right now, I’m fine with Flushing temporarily posting weak earnings results, as long as the loan book remains in okay condition. And that appears to be the case, as the total amount of loans past due is stabilizing and the low LTV ratio means the bank should be able to keep loan losses – if any – pretty limited.

I have a long position in Flushing Financial, and I will add to my position in the coming week.