Tobacco giant Altria (NYSE: MO) provides a tremendously high dividend yield of 7%, which is well above the S&P 500 index average of 1.3%. But it comes with risks, as its business has been struggling to grow in recent years, and its rate of dividend increases has been modest.

Meanwhile, pharma company Eli Lilly (NYSE: LLY) offers a much lower yield of less than 1%, but its dividend growth rate has been far more impressive.

Which stock is the better buy if your priority is to collect a lot of dividend income?

Altria has an impressive streak of raising its dividend for 55 consecutive years. Eli Lilly’s current streak only goes back to 2015. But while Altria has a more impressive track record, that doesn’t necessarily make it a better dividend growth stock.

Prior to the Great Recession in 2008-09, Eli Lilly’s dividend growth streak spanned more than 40 consecutive years. And while it would pause its rate increases for multiple years, since it has resumed raising its dividend, its increases have been much higher than Altria’s.

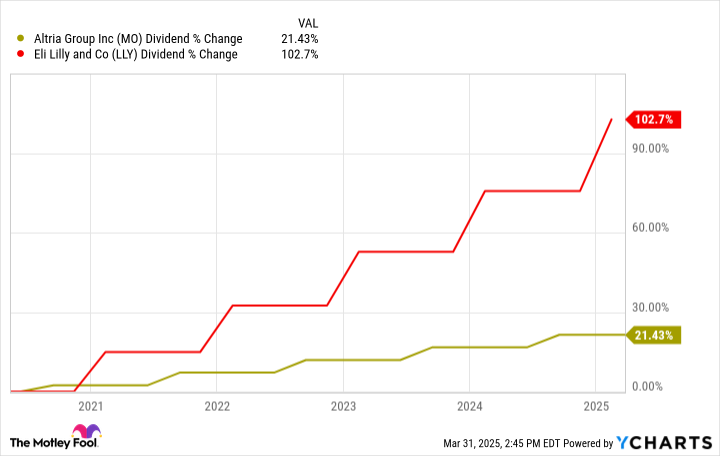

In the past five years, Altria’s dividend has risen by just over 21%, while Eli Lilly shareholders have seen their payouts double.

A big reason Eli Lilly’s dividend yield may not appear all that exciting is that the stock has been performing so well. In five years, the healthcare stock has climbed 476% in value while Altria has risen by around 52% (which lags the S&P 500’s returns of more than 116%). A soaring stock will see its yield fall since it becomes more expensive to collect its dividend, even amid generous increases.

And a big part of the reason why Eli Lilly’s stock has been such a hot buy is due to the tremendous growth it is achieving, and the growth opportunities it possesses in the GLP-1 weight loss market. Altria, meanwhile, faces an uncertain future ahead as tobacco use declines and it looks for a way to grow its business.

If you’re investing in a stock to collect a dividend from for just the next 12 months, then you might be tempted to go with Altria. But if you’re a long-term investor, then by going with the tobacco stock you risk the chance that the company may cut its dividend in the future if its profits decline due to slowing demand.

Eli Lilly’s stock exploded in the past five years, but with a more elevated valuation, it might not generate those types of returns in the future. Should its returns moderate and the company continue to make generous rate hikes, its yield could start to rise, which is why investors shouldn’t focus too much on just the current payout.