Meta Platforms Inc. (META), formerly known as Facebook Inc., is a multinational technology conglomerate that owns and manages social media sites including Facebook, Instagram, WhatsApp, and Messenger, among other products and services.

The company operates in two segments, Family of Apps and Reality Labs. Family of Apps overlooks its social media and connectivity apps, while Reality Labs focuses on Augmented Reality (AR) and Virtual Reality (VR) products.

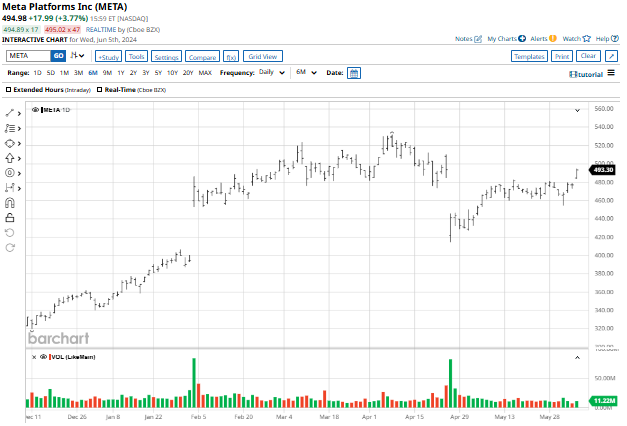

Valued at $1.25 trillion by market cap, Meta Platforms stock has easily outpaced its parent S&P 500 Index ($SPX) by gaining 40.6% this year and 83.6% over the past 52 weeks.

Meta Slides on AI Spending Concerns

Meta reported its Q1 results on April 24, with the company’s revenue of $36.46 billion edging out analysts’ estimates of $36.22 billion. Earnings per share (EPS) of $4.71 sailed past the market’s $4.32 estimate. Gross margin for the quarter improved to 81.8%, up from 78.3% in the same quarter last year.

The company reported free cash flow of $12.53 billion, and operating cash flow of $19.3 billion.

Despite the solid earnings report, the company’s weaker revenue guidance was a point of concern. Management expects revenue in the range of $36.5 billion to $39 billion for Q2, with the midpoint of $37.75 billion falling short of analysts’ $38.3 billion estimate.

Additionally, investors cast a skeptical eye on Meta’s capital expenditure plans. Alongside its soft revenue forecast, the company hiked its 2024 capex guidance to a range between $35 billion and $40 billion, saying it expects to invest aggressively in artificial intelligence (AI) and other product initiatives.

In response, META stock dropped 10% on April 25.

How Are Analysts Rating the Stock?

However, at least one analyst seems to think there’s no cause for capex concern. Meta stock remains a “Top Pick” for Mizuho Securities analyst James Lee, who said in a recent note that the social media giant could double its capital spending growth rate to 70% from 35% without impacting margins.

Additionally, amid recent concerns over a potential slowdown from major advertiser PDD (PDD), Lee wrote that product upgrades and special events should more than offset the loss of any ad revenues from China.

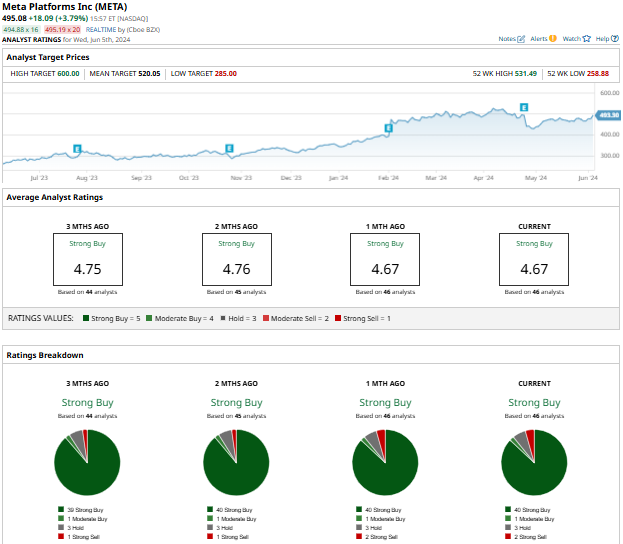

Among 46 analysts tracking the stock, 40 have a “Strong Buy” rating, 1 has a “Moderate Buy” rating, 3 have a “Hold” rating, and 2 have a “Strong Sell” rating for META.

The mean price target of $520.05 reflects an expected upside potential of 4.7% from current levels. As for Mizuho, Lee’s price target is set at $575, implying expected upside of 15.7%.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.