A look at the day ahead in European and global markets from Ankur Banerjee

The time for waiting is almost over as inflation reports from Europe and the U.S. headline the day’s agenda, with any kind of surprise likely to sway markets as investors weigh the shifting expectations over global rates.

First up will be the euro zone inflation reading, which is expected to come in at 2.5% for May after staying stable in the last couple of months at 2.4%, while core inflation is expected to be steady at 2.7%, according to a Reuters poll.

Investors will be parsing through the data to gauge the trajectory the European Central Bank is likely to take on rates. While a rate cut in June is all but certain, the focus is squarely on what comes after that.

And so, investors are likely to be extremely sensitive to even a small beat or a miss.

Markets are pricing in 60 bps of cuts from the ECB this year but a lot will depend on the inflation and wage growth readings over the coming months.

Futures indicate European bourses are set for a lacklustre opening, with the pan-European STOXX 600 index touching a more than three-week low on Thursday but on course for a 2% gain in the month.

A downward revision to U.S. GDP on Thursday stoked expectations that the Federal Reserve has room to cut rates this year, although investors for a change took the bad news (of weaker growth) as bad news, taking U.S. stocks, the dollar and Treasury yields lower.

Markets are pricing in 35 bps of cuts from the Fed this year, with a 50% chance of a rate cut in September.

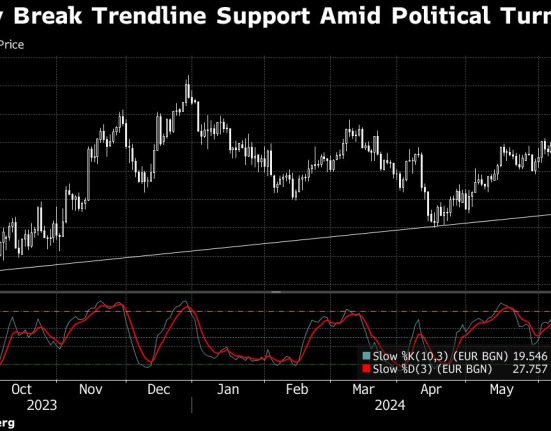

The ever-shifting expectations around U.S. rates has taken a toll on the dollar, which is set for a first monthly loss this year against the euro, Sterling, Aussie, kiwi and even the yen, although the yen’s miniscule gain is a result of the suspected intervention earlier this month.

In Asian hours, equities broadly gained, while the dollar regrouped. China stocks rose even as the data showed the nation’s manufacturing activity unexpectedly fell in May, according to an official factory survey.

Meanwhile, markets so far have shrugged off the Donald Trump verdict after he became the first U.S. president to be convicted of a crime on Thursday when a New York jury found him guilty of falsifying documents to cover up a payment to silence a porn star ahead of the 2016 election.

Shares of The Truth Social parent Trump Media & Technology Group, which is majority owned by Trump, dropped 6.5% late on Thursday after the verdict.

Key developments that could influence markets on Friday:

Economic events: May inflation report for euro zone and France, April retail sales data for Germany

(This story has been refiled to correct grammar of the word ‘headline’ in paragraph 2 and spelling of the word ‘Reserve’ in paragraph 8)

(Editing by Muralikumar Anantharaman)