Torsten Asmus

“The Empire strikes back!”

In the US, President Donald Trump’s January inauguration marked the start of a term with assertive trade policies. The administration implemented significant tariff hikes, including a 25% duty on Canadian steel and aluminium, a 25% tariff on European cars and a 30% levy on Chinese electronics. These moves intensified trade tensions, contributing to a 2.3% decline in the S&P 500 (SP500, SPX) and raising (short-term) recession concerns. The Federal Reserve kept interest rates at 4.5%, balancing inflation control with signs of economic slowdown.

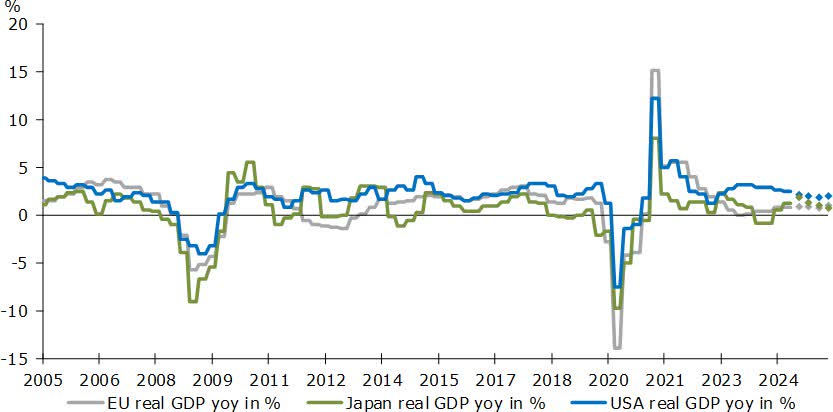

Chart 1: No recession in sight (so far)

Source: Alpinum Investment Management

Europe experienced a transformative geopolitical and economic shift, led by Germany’s landmark multi-hundred billion investment program, ending austerity. The euro surged to five-month highs, further supported by Ukraine’s acceptance of a proposed ceasefire, bolstering investor confidence. In China, authorities injected USD 200 billion into the financial sector to stabilize the property market and mitigate systemic risks. Despite these efforts, investor sentiment remained fragile, with the People’s Bank of China signalling further easing measures to support growth. The quarter underscored the fragility of the global economy, as trade disputes, policy uncertainties, and financial instability continue to weigh on growth prospects.

United States

In Q1 2025, the US economy exhibited notable resilience, buoyed by a robust labour market, with GDP growth maintaining a steady pace at 2.8% for 2024, marking the third consecutive year of expansion within the 2.5-3.0% range. Despite early signs of softening, the labour market remained a pivotal driver of consumption and crucial to economic growth. However, macroeconomic factors, including heightened policy uncertainty and escalating tariff risks, presented new challenges, particularly within manufacturing and trade sectors. The Trump administration’s imposition of a 25% tariff on steel and aluminium imports, with a potential 50% escalation for Canada, later deferred following negotiations, further strained trade relations. While tariffs on Canadian and Mexican goods were temporarily paused, the administration increased tariffs on Chinese imports to 20%, triggering retaliatory actions. The European Union also faced potential tariffs, signalling the intensification of trade conflicts.

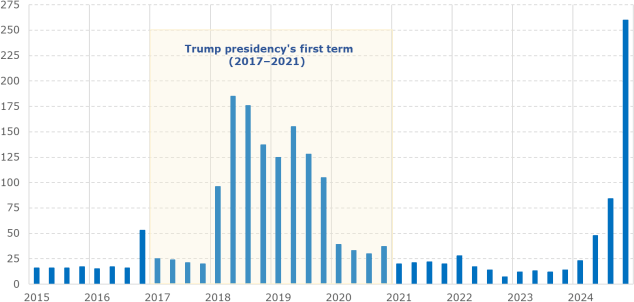

Chart 2: S&P 500 companies citing “tariffs” on earnings calls

Source: Alpinum Investment Management

Concurrently, the S&P 500 exhibited considerable volatility, driven by the surge in DeepSeek’s valuation in January, which spurred a recalibration of AI and tech stocks. Simultaneously, the aggressive tariff policy, combined with rising trade tensions, amplified market uncertainty. This led to a 2.3% decline in the index in the first quarter of the year as investors reassessed growth prospects amid escalating geopolitical risks and inflationary pressures. The US inflation remained persistent, with the CPI decelerating to 2.8% in February from 3.0% in January. In response to persistent inflation, particularly in non-housing services, the Federal Reserve adopted a cautious stance, signalling a“higher for longer” monetary policy, with two rate cuts anticipated in 2025, while maintaining the long-term policy rate in the mid-4% range.

Europe

The European economy expanded at a subdued pace, navigating a complex landscape of monetary stimulus, fiscal interventions and intensifying geopolitical tensions. The European Central Bank (ECB) executed a 25-basis-point reduction in its benchmark rate to 2.5%, marking the sixth consecutive cut within a year. This sustained monetary accommodation sought to counteract lacklustre economic activity, prompting the ECB to revise its 2025 GDP growth forecast downwards to 0.9% from 1.1%, while inflation was projected to average 2.3%. The labour market remained resilient, though wage growth moderated amid persistent economic uncertainties. Fiscal policy diverged across the region, with Germany unveiling a landmark multi-hundred billion investment program aimed at revitalizing its domestic economy, signaling a shift away from austerity, while potentially exerting broader inflationary and growth implications across the eurozone.

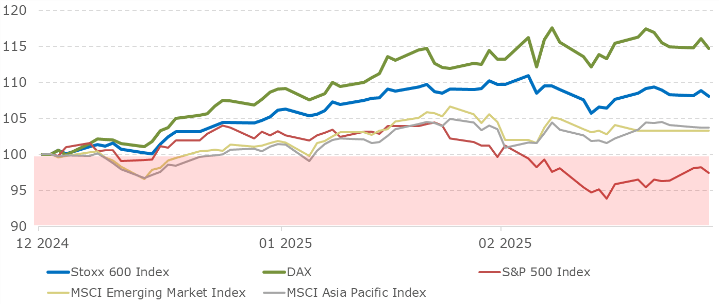

Chart 3: European equities outperforming in 2025

Source: Alpinum Investment Management

The political landscape was reshaped by the German federal election on 23 February, where the CDU/CSU secured 28.5% of the vote, emerging as the largest parliamentary bloc. The far-right AfD achieved an unprecedented 20.8%, underscoring a shift in voter sentiment and complicating coalition negotiations, with ramifications for both domestic and EU policy trajectories. Geopolitical tensions escalated as the United States imposed a 25% tariff on European steel and aluminium, prompting the EU to prepare retaliatory levies on USD 28 billion of US goods, effective April, amplifying trade war concerns. The US dollar (USDOLLAR,DXY) weakened to a five-month low. Equity markets staged a robust recovery, with the STOXX Europe 600 advancing 8.3% year-to-date, outpacing the S&P 500. European equities, trading at a forward P/E of 14x versus 22x for US stocks, benefited from favourable valuations and ECB support.

China and emerging markets (‘EM’)

China’s economic trajectory in Q1 2025 was shaped by a delicate balance between policy recalibration, persistent disinflationary trends, and heightened geopolitical risks. While GDP surpassed 130 trillion yuan (USD 17.82 trillion) for the first time, growing at 5% in line with official targets, underlying momentum remained fragile. The National Bureau of Statistics reported contracting manufacturing activity and subdued consumer sentiment, with January PMIs disappointing and servicesector expansion losing steam. External headwinds intensified as escalating trade frictions with the US and seasonal distortions, including the Lunar New Year, contributed to an unexpected decline in imports and weakening export momentum. The People’s Bank of China(PBoC) maintained a cautious monetary stance, prioritizing currency stability amid ongoing depreciation pressures, while inflation remained volatile, with a transient 0.5% rise in January followed by a sharp -0.7% contraction in February, reinforcing concerns over entrenched disinflation.

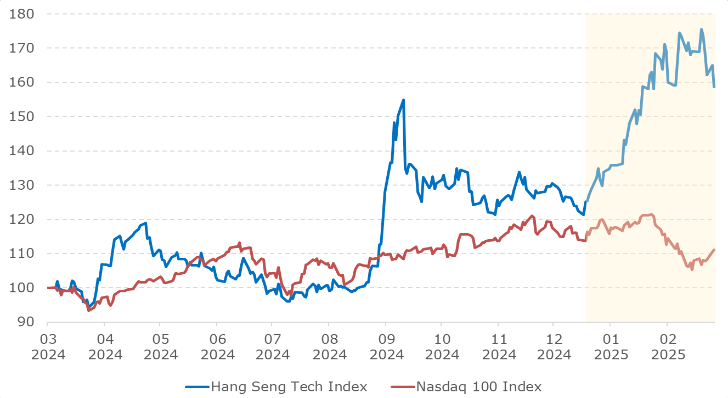

Chart 4: 1-year performance Hang Seng Tech vs Nasdaq 100

Source: Alpinum Investment Management

Equities rebounded on state intervention, led by a 24.7% YTD surge in the Hang Seng Tech Index, fuelled by President Xi’s corporate outreach and speculation over regulatory easing. Offshore equities remained vulnerable to geopolitical risks, while onshore markets displayed relative resilience. The PBoC’s suspension of bond purchases fuelled short-end volatility, flattening the yield curve. Geopolitical uncertainty loomed large, with the Trump administration’s tariff threats amplifying risks to China’s export-driven growth model. The yuan showed relative resilience, depreciating 0.5% YTD. Structural fragilities in the property sector, tepid private investment and constrained credit transmission mechanisms weighed on sentiment, reinforcing expectations that fiscal stimulus alone would prove insufficient to engineer a durable recovery.

Investment conclusions

The global economic landscape is undergoing a profound transformation, characterized by the dismantling of old structures and a realignment of power. Higher tariffs and increasing economic isolation are pushing up prices, resulting in long-term productivity losses and subdued growth prospects. Significant investments in defence and infrastructure provide a much-needed boost to stagnating regions like Europe, though this also creates delayed inflationary pressures. In response, markets are adjusting to higher risk premiums as rising debt levels compound the challenges. The US faces low growth, while the EU tries to break free from stagnation and China pursues its ambitious 5% growth target. Structural inflation, driven by de-globalization, tariffs and energy transition, intersects with geopolitical tensions and tighter financial conditions. Despite these challenges, large-cap technology stocks and the US housing market show resilience, while risk aversion permeates the broader market.

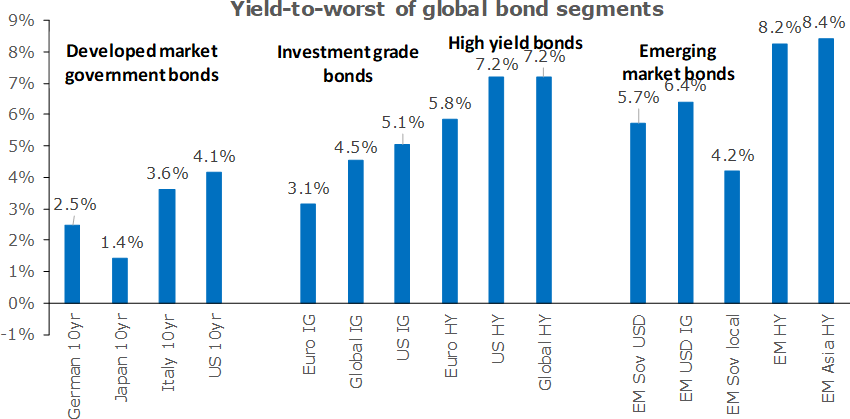

Chart 5: Yield-to-worst of global bond segments

Source: Alpinum Investment Management

Bonds: Fixed income offers compelling total return opportunities amid widening credit spreads and a steeper European yield curve. We favour short-duration high-yield and loans, while duration remains an effective portfolio diversifier.

Equities: Fiscal stimulus in Europe and China, alongside USD weakness, bolsters ex-US equities short-term. We maintain a positive equity bias with a blended style approach, acknowledging persistent volatility and limited upside in large-cap US equities.

The tactical approach emphasizes balance, with a slight preference for value and cyclicals amid resilient growth. Duration is neutral, maintaining a balanced view on IG bonds and USTs, while favouring short-term HY, loans and selective below-IG bonds and hybrids.