The rise of thematic and sectoral funds is no accident. It’s the product of a perfect storm of regulation, sales psychology, and market momentum.

| Photo Credit:

iStockphoto

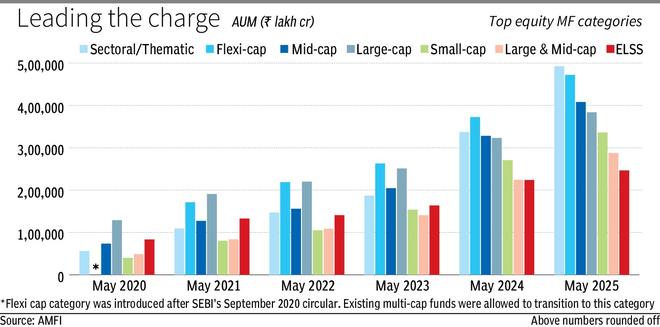

Just five years ago, the sectoral and thematic mutual fund category was nowhere near the top of the equity MF leader board. With ₹56,000 crore in assets under management (AUM) in May 2020 post the Covid crash, the category trailed large-cap, multi/flexi-cap, ELSS (Equity Linked Savings Scheme), and mid-cap funds. But that pecking order has been turned on its head.

Today, sectoral and thematic funds are the largest equity MF category in India, clocking a staggering ₹4.92 lakh crore in assets of total equity MF’s ₹32 lakh crore, according to May 2025 AMFI data. This puts it ahead of erstwhile leader flexi-cap funds (₹4.71 lakh crore), mid-cap funds (₹4.08 lakh crore), and large-cap funds (₹3.83 lakh crore). In half a decade, that’s a 7.8x jump in AUM, a 3.7x growth in folios (from 67 lakh to 3.1 crore), and doubling of the scheme count from 107 to 215 for thematic and sectoral funds. This isn’t a slow, organic climb. It’s a blitzkrieg.

Category explosion

The rise of thematic and sectoral funds is no accident. It’s the product of a perfect storm of regulation, sales psychology and market momentum.

One, SEBI’s one-fund-per-category rule, with a few exceptions, has nudged fund houses to launch aggressively in this category. Result? MF mart has seen a new launch every 2-3 weeks in the thematic and sectoral space, as focussed exposure and tactical upside in these offerings was marketed heavily. Sample this: Net inflow (funds mobilised minus redemptions) in this category has been a whopping ₹1 lakh crore in just the past 12 months.

Two, New Fund Offers (NFOs) sell well. The typical ₹10 NAV makes it feel cheap. Distributors love the narrative and investors love the novelty. No track record? No problem, because it’s a “new idea”. Trend-based themes are easier to market. Infrastructure, ESG, PSU, EV, consumption, business cycle, defence, manufacturing, digital: each new macro trend gave AMCs a reason to launch, and investors a reason to bite. Similarly, banking, IT, pharma, auto, commodities, energy, every sector got its moment in the sun, and fund houses wasted no time rolling out a scheme to match.

Three, the Indian stock market co-operated. Between May 2020 and May 2025, the Sensex jumped from 31,000 to 81,000 levels, a 5-year CAGR (Compounded Annual Growth Rate) of 21.2 per cent. Thematic and sectoral funds rode the wave: PSU funds and infra funds delivered a 5-year CAGR of 32-33 per cent, technology funds at 28 per cent, banking, consumption energy funds at 22-25 per cent. So, bets by investors, who turned to thematic and sectoral funds for higher returns, paid off.

The catch

Another striking trend in the sectoral/ thematic fund boom is the rise of low-cost passive offerings. In just the last six months, nearly 50 new passive thematic and sectoral funds have hit the market, as fund houses increasingly wrap trending narratives into low-cost, index-linked formats, while aligning with the broader shift towards passive investing.

Despite their popularity, thematic and sectoral funds come with a built-in concentration risk. For instance, cutting across fund houses, many of the best-performing thematic and sectoral funds have 50–90 per cent exposure to just their respective top 3 industries. In some of them, the top 5 stocks account for nearly half of the portfolio. This opens the door to the possibility of poor timing, or a policy reversal denting returns quickly.

Sectoral and thematic valuations are not exactly cheap either. According to data from Nifty Indices, while the Nifty 50 trades at a trailing price-to-earnings (P/E) of around 22.3x (as of May 2025), sectoral and thematic indices are priced far higher, signalling the premium investors are paying to hitch a ride. For e.g., the Nifty Consumer Durables commands lofty PE valuations of 69x, while Nifty Realty and FMCG trade at 47x and 44x, respectively.

Several thematic indices are also trading at astonishing valuations. The Nifty India Digital index leads the pack with a P/E of 97, followed by tourism (67x), non-cyclical consumption (64x), and defence (61x). Even themes like New Age Consumption and Capital Markets trade at 47-50x earnings. While some indices have more moderate valuations, the overall picture suggests that investors are pricing in a significant amount of future growth.

Investors should do well to treat these funds as satellite holdings, not core allocations. Plus, sectors and themes can be cyclical, turning return-rich funds into wealth traps.

Published on June 14, 2025