Key takeaways

The French Finance Act for 2025 radically overhauled the tax and social security treatment of management packages.

The BSPCE regime is also subject to some amendments.

Key changes and features you need to be aware of:

- a new tax and social security regime has been established for all securities subscribed or acquired in consideration for employee or executive functions;

- as a general rule, the taxation of the net sale gain follows the standard salary rules (marginal tax rate of 59%, including a new specific employee social contribution), with no employer social security contribution applicable;

- as an exception, the net sale gain is taxed under the capital gains regime (marginal tax rate of 34% instead of 59%), subject to certain conditions and capped at a financial performance threshold for the employee or manager equal to three times the company’s financial performance multiple (corresponding in practice, to the “project multiple”);

- gains resulting from the exercise or acquisition of ‘founder stock warrants’ (“BSPCE”), stock options and free shares remain subject to their standard tax and social security regime; however, sale gains derived from these instruments are subject to the aforementioned new regime;

- securities subscribed to upon the exercise of BSPCE, as well as securities subscribed or acquired in consideration for employee or executive functions which fall under the new regime, may no longer be held in a PEA (plan d’épargne en actions);

- the portion of the gain taxed as salary pursuant to the new regime remains taxable in the context of a roll-over by the employee or manager, with no deferral or suspension of taxation applicable.

Chapter 1 – The new management package regime

The French Finance Act for 2025 radically overhauled the tax and social security treatment of management packages. Coming into force on February 15, 2025, this legislation, codified under Article 163 bis H of the French tax code, aims to resolve the uncertainties that have concerned private equity and venture capital professionals following the French Supreme Administrative Court’s rulings on July 13, 2021.

This new provision establishes the principle pursuant to which “the net gain realized on securities subscribed or acquired by employees or managers, or granted to them, is taxed according to the general salary rules when it is acquired in consideration for the duties of an employee or manager in the company issuing the securities“. By way of exception, and subject to certain criteria, the gain, up to a determined cap, may benefit from the tax and social security regime applicable to capital gains (the “Capital Gains Regime“), i.e., a flat tax of 34%1.

In principle, this regime applies to all employee shareholding schemes, whether governed by legal provisions (free shares, BSPCE, stock options) or not (ratchet shares, stock warrants, etc.). The French Finance Act for 2025 has legalized the prohibition of registering securities covered by this regime in a PEA / PEA-PME.

However, the application of this regime to a given individual will have to be analyzed on a case-by-case basis, depending on the type of instrument and the situation specific to each holder.

For instruments governed by a so-called legal regime, the eligibility for the Capital Gains Regime now requires a risk of loss of the acquisition or subscription cost to be supported by the employee / manager. For unregulated instruments, a risk of capital loss must also exist, together with a minimum two-year holding period.

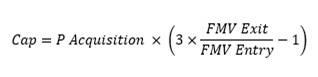

The main feature of this regime is that the Capital Gains Regime applies up to a specific cap determined by a financial performance multiple, which, in practice, should correspond to the project multiple.

The project multiple is defined as three times the ratio between (i) the company’s fair market value at the time of sale and (ii) the fair market value recorded when the shares were acquired or allocated, as such

With :

- 𝑷𝑨𝒄𝒒𝒖𝒊𝒔𝒊𝒕𝒊𝒐𝒏 Acquisition or subscription price of shares, acquisition value of free shares, or exercise price for BSPCE and stock options.

- 𝑭𝑴𝑽𝑬𝒙𝒊𝒕 Adjusted fair market value of the issuing company at the sale date or any other event under Article 150-0 B of the French tax code.

- 𝑭𝑴𝑽𝑬𝒏𝒕𝒓𝒚 Adjusted fair market value of the issuing company at the acquisition/subscription date or grant date for free shares, BSPCE, and stock options2.

In the case where securities are held through a “ManCo” or similar entity, a look-through approach must be applied, meaning the operational company’s fair market value will replace that of the “ManCo”.

The net sale is then taxed as follows:

- Gain < Cap: taxed under the Capital Gains Regime, i.e., flat tax of up to 34% (12.8% income tax3 and 17.2% social security levies); and

- Gain > Cap: taxed as salary income at a marginal rate of up to 59%, i.e., subject to income tax up to 49%4 as well as a new specific 10% employee contribution.

It should be noted that if the above eligibility conditions are not met, the entire gain will be taxed as salary income and be subject to the 10% employee specific contribution.

In addition, the portion of the gain taxed as salary income would remain taxable in the event of a roll-over, as no tax deferral or tax suspension would apply. In practice, this should have an impact on the quantum of reinvestment by employees/managers in LBO or venture capital transactions, as the tax will become due and payable upon reinvestment, even though no cash proceeds would have been realized from a sale.

Furthermore, in the event where prior to a transaction, an employee/manager proceeds with a donation of a portion of the shares held in a target company followed by a sale, the entire gain would remain taxable at the level of the donor upon the sale of the securities by the beneficiary. These tax impacts have given rise to controversy and a harsh lobbying from advisors and manager representatives. The French Tax Authorities’ administrative guidelines in this respect are eagerly awaited, practitioners are hoping for clarifications and potential adjustments.

As far as employers and sponsors are concerned, the entire gain recognized upon the sale of the shares is exempt from employer social security contributions. This is a key advantage, as it effectively eliminates the risk of application of French social security contributions to the instruments falling under this new regime.

Since the new regime requires a link between the acquisition or subscription of the instruments and employee or executive functions, it should allow for the a wider use of vesting mechanisms, good/bad leaver clauses, and references to non-compete clauses outside of the employment contract or social mandate, without necessarily negatively impacting the tax treatment of the management package.

Key uncertainties that still need to be clarified:

- the concept of “in consideration for their employee or executive functions” remains unclear and has yet to be defined;

- the definition of “risk of loss” remains uncertain, as does the impact of put and call options on the eligibility of the Capital Gains Regime, particularly when a floor price is set;

- the definition and calculation method of the “financial performance multiple” require further clarification, and in particular confirmation that the “project multiple” can be used;

- the methodology for computing the cap in the context of prior roll-over(s) benefiting from a tax deferral regime remains to be clarified; and

- for securities already registered in a PEA / PEA-PME when the law came into force, it will be necessary to confirm that the entire gain and not just the portion of the gain taxed as salary income will be excluded from the PEA / PEA-PME tax regime.

Although this legislation provides greater clarity in a previously uncertain tax and social environment, there are still several grey areas that need to be clarified by the French tax authorities in order to comfort venture capital and private equity professionals. It is also regrettable that this text has not been debated before the Parliament during the legislative process.

Chapter 2 – The reform of the BSPCE regime and its interaction with the new management package regime

With regard to BSPCE, the new Article 163 bis G of the French tax code, resulting from the French Finance Act for 2025, now distinguishes between (i) the exercise gain and (ii) the net sale gain from securities subscribed to after exercising the BSPCE. These provisions apply to securities subscribed from January 1, 2025, regardless of the date when the BSPCE were granted.

- The exercise gain, considered as an employee benefit, corresponds to the difference between (i) the value of the securities subscribed to on the day the BSPCE are exercised and (ii) the acquisition price of these securities. It is taxed during the year of disposal, sale, conversion to bearer form or lease of the securities subscribed to in exercise of the BSPCE, in accordance with the terms of the previous regime, i.e. taxation at the overall rate of 30% or 47.2% depending on the time the beneficiary was employed/worked for the company. This gain is not eligible for tax deferral.

- The gain on disposal corresponds to the difference between (i) the sale price of the securities subscribed to after exercising the BSPCE and (ii) the value of the shares on the day the BSPCE are exercised. It is taxed under the Capital Gains Regime, entitling it in particular to the benefit of tax deferral and tax suspension provisions. In practice, only this portion of the gain falls within the scope of the new regime.

In addition, BSPCE and securities subscribed to after exercising the of BSPCE may no longer be registered under a PEA / PEA-PME. This measure applies retroactively from October 10, 2024. For securities already registered under a PEA / PEA-PME prior to this date, the holder may withdraw them without consequence, provided certain conditions are met.

Note: in practice, the impact of this reform should be limited for BSPCE, as they are usually exercised as part of a liquidity event, thus limiting the carry of the securities. As the gain on disposal is nil, the new regime should not impact the tax treatment of the gain.

Chapter 3 – The coexistence of the new management package regime with stock option and free share regimes

With regards to stock options, the taxation of the gain on exercise of the option remains unchanged and is taxed based on the marginal income rate up to 49%5 as well as social security levies at a rate of 9.7%, plus a specific employee contribution of 10%. The capital gain realized upon disposal of the stock options is, in principle, taxable based on the capital gains regime, but will now fall within the scope of the new regime and its financial performance cap.

With regards to free share, taxation of the acquisition gain remains unchanged, i.e., up to a limit of €300,000 it is taxed based on the marginal income tax rate up to 49% after a 50% allowance is applied as well as social security levies at a rate of 17.2%. The portion of the gain exceeding €300,000 is taxed based on the marginal income tax rate up to 49%6 as well as social security levies at a rate of 9.7%, plus a specific employee contribution of 10%. The gain realized upon the disposal of the free shares is, in principle, taxable based on the capital gains regime, but will now also fall within the scope of the new regime and its financial performance cap.

References

- Including the exceptional contribution on high revenue up to 4%.

-

Although not covered by the law, in the case of BSPCE and stock options, the grant date of the instruments should be taken into account.

-

Including the exceptional contribution on high revenue up to 4%.

- Including the exceptional contribution on high revenue.

-

Including the exceptional contribution on high revenue.

-

Including the exception contribution on high revenue.

[View source.]