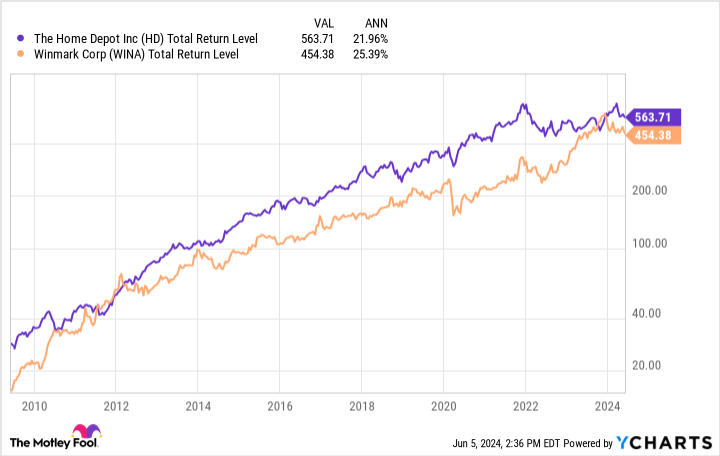

Sometimes, long-term outperforming stocks just have stunning stock performance charts. Two excellent examples are home improvement juggernaut The Home Depot (NYSE: HD) and resale goods franchisor Winmark (NASDAQ: WINA).

With annualized total returns of 22% and 25%, respectively, over the last 15 years, these two compounders have stock charts that border on art.

This unstoppable up-and-to-the-right movement of the stocks’ share price over time correlates nicely with each company’s slow-and-steady compounding ways. While these two businesses have only averaged mid-single-digit sales growth annually over the last decade, they have been fantastic investments thanks to their immense profitability, declining share counts, and increasing dividends.

Best yet for investors, despite Home Depot and Winmark’s incredible runs over the last 15 years, the stocks’ share prices are currently 16% and 22% below their 52-week highs. Following this recent dip, now is as good a time as any to consider buying and holding these magnificent compounders for decades.

Home Depot’s numerous outperformance indicators

Home Depot is the world’s largest home improvement retailer, generating over $151 billion in sales from its 2,337 stores last year. Despite its size, the company estimates that it only has a 17% share of its $1 trillion target addressable market across the United States, Mexico, and Canada.

As it gradually adds to its store counts of 138 and 182 in Mexico and Canada, respectively, Home Depot should have plenty of opportunity to continue pushing its market share higher. Similarly, the company plans to grow its share of the market further by focusing on specialty trade groups (think electricians, painters, plumbers, or roofers, for example) among its pro customers.

A clear example of this was Home Depot’s recent $18 billion acquisition of SRS Distribution, which serves professional roof, landscape, and pool contractors. By bringing in over $10 billion in annual sales, SRS will be a needle-moving acquisition right away for Home Depot, immediately expanding the company’s presence among pros in the specialty trade group.

In addition to the potential provided by growing its market share, the company has long-term megatrends working in its favor.

First, 53% of homes in the U.S. are 40 or more years old — up from 32% in 1995. Simply put, old houses need more upkeep, and Home Depot should inevitably capitalize on this notion. Second, the owner-occupied vacancy rate in the U.S. remains near 1% — its lowest level in 40 years. In an oversimplification, this means new home construction will increase at some point soon in America, and Home Depot will be there to serve the pros who do the building.

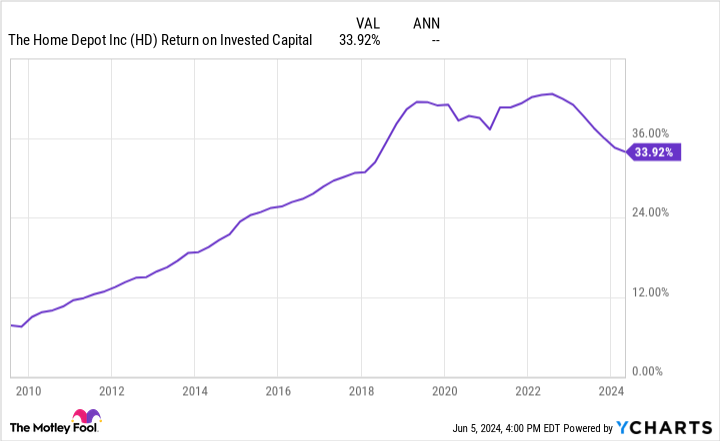

On top of these factors, the company has an array of financial indicators that often point to the potential for a stock to beat the market. With a 34% return on invested capital (ROIC), Home Depot generates outsize profitability compared to its debt and equity.

Historically, high-and-rising ROICs such as this have led to outperforming stocks.

Furthermore, Home Depot has raised its dividend for 14 consecutive years, now yielding 2.6% while only using 57% of its net income to fund these payments. But the shareholder returns don’t stop here. The company has also repurchased over 3% of its total shares outstanding annually since 2009, lowering its share count by 42% over that time. Companies with declining share counts and well-funded dividends, such as Home Depot, have also been proven to provide higher returns than the broader market over the long term, according to numerous studies.

Thanks to these promising financial indicators and the clear megatrends supporting Home Depot’s long-term growth, the company looks like a fantastic buy at a below-market valuation.

Winmark: Powering the circular economy megatrend

Home to over 1,300 resale franchises across its Plato’s Closet, Play It Again Sports, Once Upon A Child, Music Go Round, and Style Encore brands, Winmark is a shining example of the effect that circular economies can have on the world. Thanks to its operations, the company estimates that since 2010, it has put over 1.7 billion items back to good use, helping them avoid landfills, storage units, garages, or the top shelves of closets.

While this feel-good purpose alone makes Winmark an exciting stock, the company’s long-term partnerships with its franchisees could prove to be the true magic.

Since it’s thinking decades ahead (sometimes even multiple generations ahead), Winmark isn’t overly concerned with what happens quarter to quarter. What it wants to do is build a lasting legacy alongside its franchisees. Speaking to Jim Gilles with The Motley Fool, Chief Executive Officer Brett Heffes expounded upon this notion:

Because what happens, is our most successful franchisees, they understand that their business is a legacy asset in the community. They manage the business for themselves, the community, but more importantly, the next generation. This legacy mindset leads to continued investment on our part, whether it’s technology, whether it’s marketing, whether it’s operations, and it just allows us to fulfill our mission.

In operating over this generational time frame, Winmark takes a slow and steady approach to its growth, inching sales higher by 4% annually over the last decade. By taking its time to vet new franchisees and scout new potential store locations, the company has generated a ridiculous 188% ROIC and a free cash flow margin of 51%.

Armed with this cash generation, Winmark always looks to reward shareholders, as it typically pays out almost all excess cash to shareholders in the form of special dividends in many years. However, if Heffes deems the company’s shares to be trading below intrinsic value, he’ll also swoop in to repurchase shares, which led to a 4% annualized decline in share count since 2014.

With Statista projecting the circular economy to nearly double its sales between 2022 and 2026, Winmark is well-positioned to continue rewarding investors for decades — if not generations — to come.

Should you invest $1,000 in Home Depot right now?

Before you buy stock in Home Depot, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Home Depot wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $740,688!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 3, 2024

Josh Kohn-Lindquist has positions in Home Depot and Winmark. The Motley Fool has positions in and recommends Home Depot and Winmark. The Motley Fool has a disclosure policy.

2 Dividend Stocks to Double Up on Right Now was originally published by The Motley Fool