KanawatTH

Bitcoin (BTC-USD) is one of the most interesting financial assets in modern times to me. The asset is mired in controversy, with avid supporters who believe that its price is set to increase by many multiples in the future and strong detractors who oftentimes believe that Bitcoin isn’t worth anything at all.

Only a very small number of assets have such a high degree of deviation in what investors believe the asset should be trading for, and it reflects an inherent difficulty in answering the question of Bitcoin’s true value.

I personally fall into the camp that believes that Bitcoin and most cryptocurrency in general is currently of little to no intrinsic value. I believe this for a myriad of reasons, such as Bitcoin being easily copiable (many have easily launched their own cryptocurrencies with identical properties), as well as it being impractical for transactions without the use of a centralized entity. Furthermore, Bitcoin being the first cryptocurrency, is not as technologically advanced as its successors, which use concepts such as proof of stake.

That being said, if you took this stance at nearly any point since Bitcoin’s inception, it would’ve lost you money, so this view won’t feature in my analysis.

Instead, my analysis will focus on looking at supply/demand dynamics and analyzing the key factors which influence the supply and demand sides of the Bitcoin market. Looking back over the history of Bitcoin, I believe that taking this approach would’ve, in general, led to more accurate trading decisions than focusing solely on trying to determine an intrinsic value for Bitcoin, and then making investment decisions based on that.

Key Factors Influencing Bitcoin Demand:

The primary factors which influence the Demand for Bitcoin in my eyes are as follows:

- Media attention on Bitcoin/crypto: In both 2017 and 2021, media attention contributed significantly to Bitcoin’s run-up. Ads for various cryptocurrencies could be seen in airports, on public buses or in subways globally. This increased media attention led to increased buying, causing price increases, again garnering more attention. During these periods, it was common to hear people with otherwise little to no interest in finance talking about cryptocurrency, and celebrity promotion of cryptocurrency was widespread.

- Increased adoption: The recent Bitcoin rally comes at least in part as a result of the approval of Bitcoin ETFs, which are highly regulated and thus allow investors who are otherwise cautious of putting their money in Bitcoin to invest, as well as encouraging some degree of increase in institutional adoption.

- The integrity and reputation of the crypto ecosystem: Interestingly, when events occur which show that there can be consequences for nefarious actors in the crypto community, Bitcoin tends to rally. In some ways, this is a facet of increased adoption, since the rallies are likely based on removing fraudsters from the ecosystem being seen as good for long term investment/adoption. A recent example of this is when Bitcoin rallied in anticipation of the sentencing of Sam Bankman-Fried. This can also have a significant impact on supply, with news of fraud, pushing prices down.

- Sooner/faster than expected interest rate cuts, which tend to benefit risk-on assets.

Key Factors Influencing Bitcoin Supply:

Bitcoin supply is generally affected by two important factors:

- Bitcoin’s price relative to its recent history: A runup in price can lead to increases in investors looking to sell to lock in gains. Depending on the situation, this effect can however often be counteracted by even more demand to buy, as a result of seeing a runup and hoping it will continue.

- Bitcoin halving: Every time Bitcoin goes through a halving, the total amount of new Bitcoin awarded to miners decreases. Since miners sell Bitcoin to cover costs which they have to pay in fiat currency, less Bitcoin being awarded to miners restricts Bitcoin supply.

Analysis of Demand Factors:

Starting on the Demand side; it’s clear today that the amount of media attention surrounding Bitcoin and crypto as a whole is fairly minimal compared to the attention it garnered in the past, near the peaks of bull runs. In 2021, you couldn’t avoid hearing about or seeing ads for crypto if you tried. Today, that promotion is far more subdued.

In my assessment this can mean one of two things: Firstly, that we’re not yet at the top of a bull run, or secondly that after the immense hype surrounding cryptocurrency in 2021 and the number of people that lost money investing in it at the time, the broader public are apathetic towards crypto and Bitcoin, leading to the lower media attention we see today. My assessment is that the latter case is more likely.

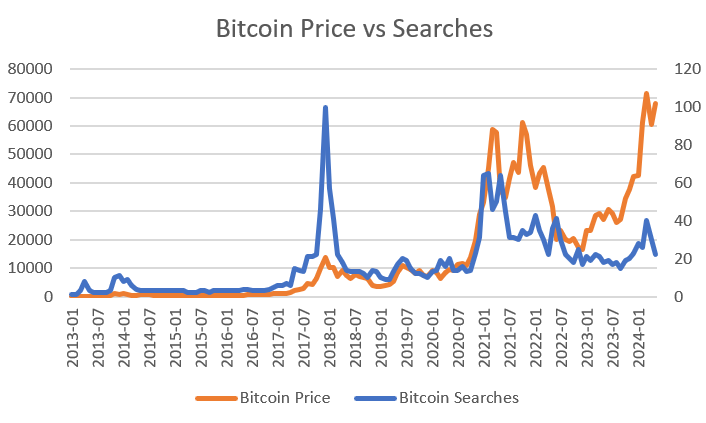

Bitcoin Price vs Searches Chart (Excel)

The above chart plotting Bitcoin price vs. Bitcoin Google searches (expressed as a percentage of their all time high figure achieved in 2017), lends evidence to the observation that Bitcoin isn’t gaining nearly as much attention as in the past. Furthermore, interest in Bitcoin has begun trending down sharply, whilst prices aren’t budging. In the absence of price appreciation, it’s difficult to identify a major driver of growth in media attention for Bitcoin.

Furthermore, it’s evident from the chart that previous periods of growth in the price of Bitcoin have occurred only in conjunction with increasing interest, and when price stagnated, alongside searches, that marked the end of the bull run.

In my view, this lends evidence to the case that Bitcoin has reached a near term peak and will begin to trend downwards.

Furthermore, in the near term, there don’t seem to be significant events on the horizon which would increase adoption. The Bitcoin ETFs obviously did lend themselves to this, but that’s already contributed to a large runup in price.

The approval and impending launch of Ethereum ETFs could help increase investment in Bitcoin ETFs, if they draw sufficient media attention to crypto ETFs as a whole. However, Ethereum (ETH-USD) does compete with Bitcoin as an investment and thus, the launch of Ethereum ETFs could also lead to a decrease in demand for Bitcoin ETFs, as investors use the Ethereum ETFs as a substitute instead. Hence, the net effect of the launch of these ETFs on demand for Bitcoin is blurry, but most likely neutral or moderately positive in the short term, but negative over the longer term, as the effect of media attention as a result of their launch dies down, leaving only a competitor for investment.

From an integrity standpoint, I believe that there are unlikely to be any major scandals in the cryptocurrency community in the next few months. The FTX and Binance cases are old news and essentially resolved. The remaining exchanges are generally of higher integrity. Coinbase is even listed on the stock exchange, and thus has far more incentive to operate conservatively and avoid pushing the boundaries of the law. This should have a marginally positive effect on buying and suppress selling.

Barring any anomalies, the current trajectory of rates expected by the market appears to be reasonable, and so I’m comfortable to assume that the effect of future fluctuations of interest rates is neutral in expectation.

Analysis of Supply Factors:

Bitcoin’s price is high relative to its recent history. Furthermore, the price is no longer rallying, which is likely to suppress buying from investors hoping to get in on a runup. The effect of this should be straightforward. This should increase selling pressure, as investors look to lock in gains and trim allocations to a volatile asset.

Furthermore, whilst the Bitcoin halving typically precedes a rally in the price of Bitcoin. This time, the price rallied prior to halving and has remained steady since then. I view this as a consequence of more sophisticated organizations such as hedge funds trading Bitcoin today, whereas in the past, Bitcoin trading was comprised largely of retail traders.

If the expectation is for the price to appreciate upon halving due to a reduction in supply as a result of miners selling, then the rational decision is to buy, prior to halving. If enough sophisticated investors come to the same conclusion, this would lead to a rally prior to halving, rather than after it, which is consistent with what we’ve seen in the market this time.

This leads me to believe that the halving is already priced in by investors, and Bitcoin traders can’t expect the old strategy of buying after halving to get in on a rally to work.

Bringing it Together:

Whilst there are some events on the horizon that are likely to cause marginal demand growth, the lackluster and declining media attention and interest in Bitcoin far outweighs the effects of these events in my eyes. Furthermore, the correlation between searches and price rallies has held strong in the past and significant rallies have only taken place in conjunction with climbing attention and interest, something which isn’t present currently.

The supply picture isn’t looking great for Bitcoin’s price either, with the restriction in supply due to halving seeming to be already accounted for, as evidenced by the pre-halving rally. Bitcoin’s relatively high price and stagnant rally also gives investors in the green a good chance to trim Bitcoin allocations, which I expect to add to selling pressure.

Combining both sides of the market, it looks as though the most likely outcome is that demand lags behind supply, which should result in a declining price. As a result, I’m initiating coverage on Bitcoin with a sell rating.