koto_feja

In May, I initiated coverage for MDA Space Ltd. (TSX:MDA:CA), (OTCPK:MDALF) with a buy rating. After the stock initially declined, it is now trading 12% higher, showing a better return than the S&P 500’s 7.5%. In this report, I will be discussing the most recent results and assess the continued appeal of the stock by updating my price target and rating.

Why Our MDA Space Analysis Matters To You As An Investor?

MDA Space is one of over 100 many names that I cover which benefit from a thorough qualitative and quantitative analytical process. With that analytical rigor, we analyze each and every company in our coverage portfolio and instead of comparing names, we developed an analytical model that uses a wide array of input variables to provide every name with a valuation and multi-year stock price target cadence based on an EV/EBITDA valuation against the company’s median EV/EBITDA multiple and the peer group multiple.

Apart from a multi-year price target based on these multiples, we also score each stock with a rating system that includes a combination of earnings growth, historical performance against the broader markets, and expected upside of stocks against the long-term historical index growth rate of stock markets. By doing so, the names in our coverage benefit from a unified approach towards determining ratings and calculating stock price targets, and we don’t have to compare all 100 names in our portfolio to figure out which name is more attractive.

MDA Space Sees Margin Pressure But Backlog And Income Growth Are Strong

MDA Space

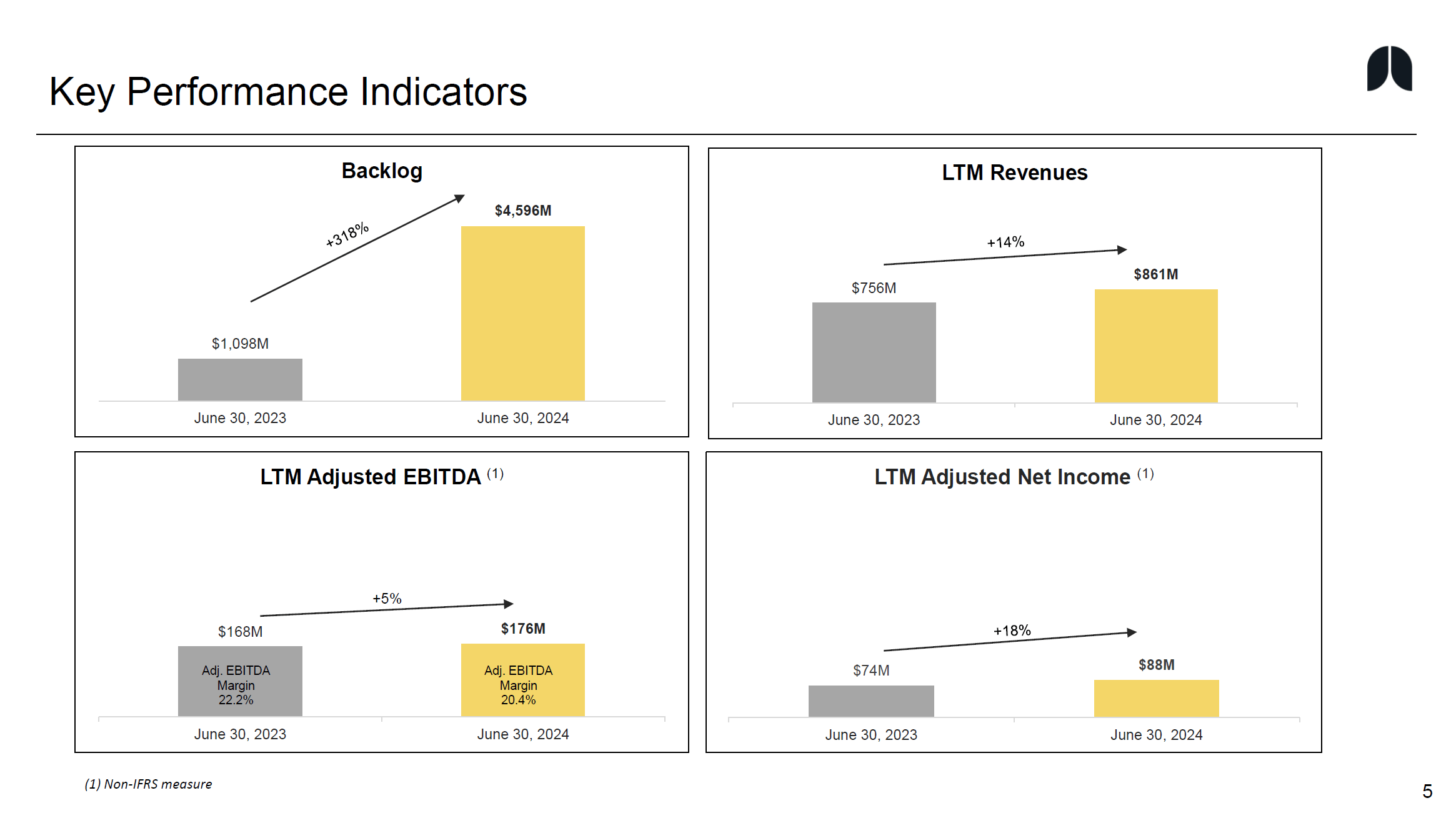

Measured over the past twelve months, backlog quadrupled, driven by a C$2.1 billion award in 2023 to build 198 satellites for Telesat and a C$1 billion contract for the Canadarm3 flight system. Revenues were up 14% and that is a good growth number. Adjusted EBITDA grew 5% to $176 million, with a 180-bps contraction in margins. That is a significant contraction, but the margins are still above the 20% that the company is aiming for. The lower adjusted margins are mostly reflective of mix and a higher depreciable asset base, which is included in the cost of sales. We should also note that in many space businesses, material and labour costs have significantly increased, which also pressure margins. Adjusted net income showed 18% growth, which exceeds the revenue growth. So, the adjusted net income margin actually improved.

MDA Space

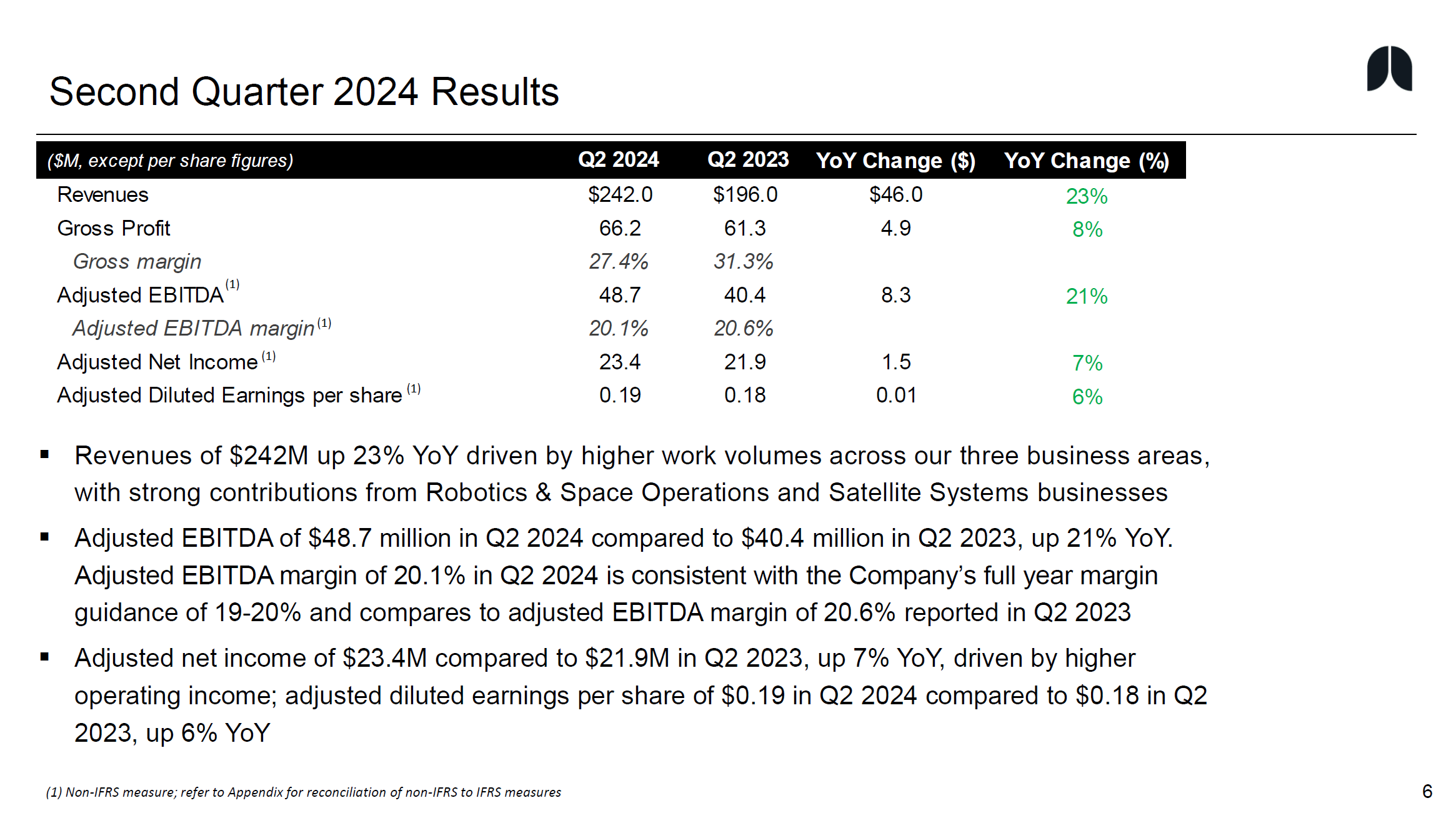

Looking at the quarterly numbers rather than the twelve-month trailing numbers show 23% growth to $242 million with a gross margin pressure due to mix and depreciation of assets. Adjusted EBITDA grew 21% to $48.7 million with a modest margin pressure while adjusted net income for the quarter grew by 7%. So, solely looking at the quarterly figures reflects the revenue growth in the business much better, while it also captures the reality of Adjusted EBITDA growth despite margin pressure.

Year-to-date, we see significant improvements in the free cash flow as free cash flow increased from negative $2 million to $95 million and when we exclude growth CapEx which provides us with a figure to assess the cash generation for a stable business the free cash flow increased from $79 million to $163 million.

MDA Space Increases Outlook For 2024 Is More Promising

MDA Space

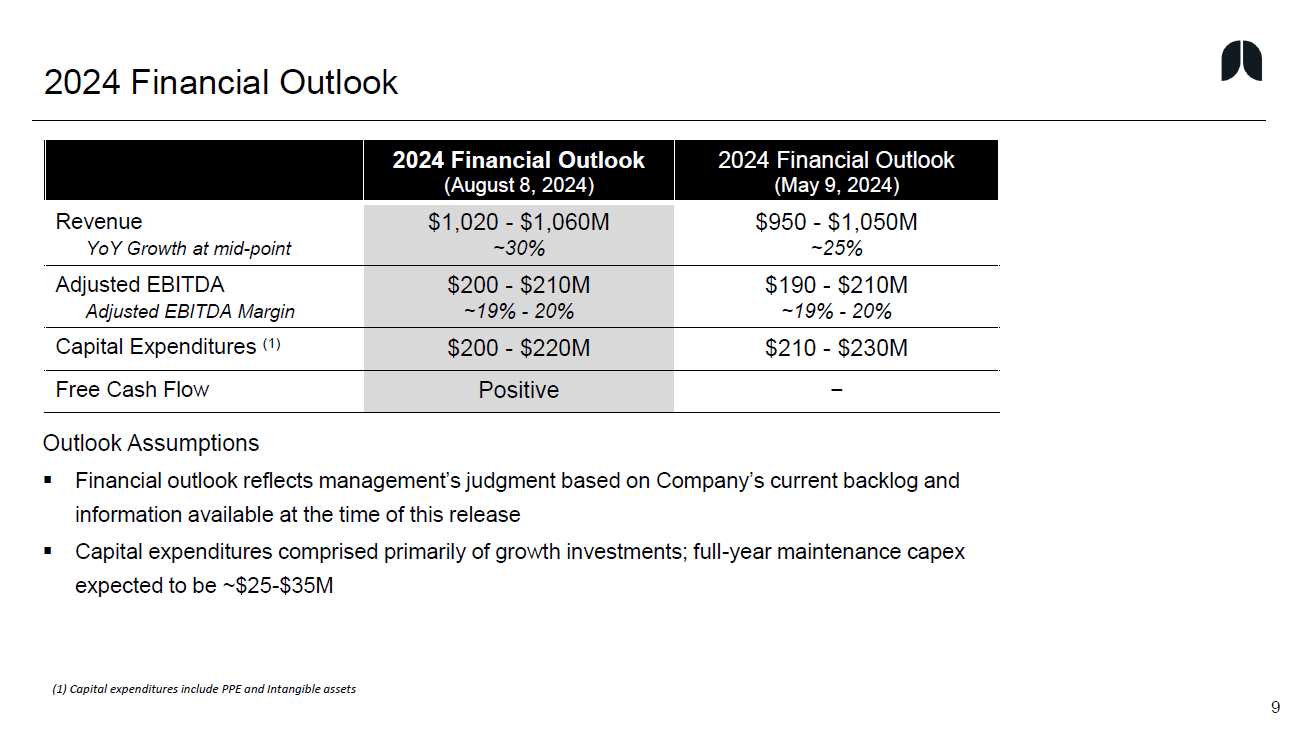

MDA Space has lifted its sales guidance by $70 million on the lower side and $10 million on the higher side, while adjusted EBITDA guidance has been lifted by $10 million on the lower side while CapEx has been guided $10 million lower. It is not a huge lift to the guidance. The higher sales guidance should drive around $14 million in EBITDA, and that is also what we see in the EBITDA lift. More promising is the free cash flow expected to be positive for the year, which is a year ahead of schedule. So, despite some margin pressure, the company is on track to deliver on its targets.

What Are The Risks And Opportunities For MDA Space?

The risk for MDA Space would seem to be margin pressure from higher labor and material costs. MDA Space is not the only company facing that pressure. Many companies with exposure to space and satellites see a higher cost base. While the margin pressure is evident, I believe there is more to like about MDA Space than to dislike. Space is gaining momentum and the segment is maturing, and MDA Space has presorted for that as it unveiled its Aurora and Skymaker product lines. The former aims to capitalize on a transition to digital space technology, while the latter provides space robotics products and services. Especially with the commercialization of space in mind, I believe space robotics could offer solid growth opportunities, and with the establishment of the product line, MDA Space is also positioning for this.

When we think about investing in space or space tech, many investors might think about SpaceX or young companies revolutionizing space. Many of the younger companies also carry some risks as their track record is not proven, although recent examples show that past performance is not an indicator for future success. However, what I do like is that MDA Space is not a new company. It was founded 55 years ago, with expertise in space dating back decades. As a public company, it is relatively new as it went public in 2021 after a consortium of firms bought it from Maxar Technologies, but that expertise in the field remains, and financially the company is also doing well with a growing space market, positive free cash flow expected this year and leverage coming down closer to historical levels.

MDA Space Stock Has Significant Upside

The Aerospace Forum

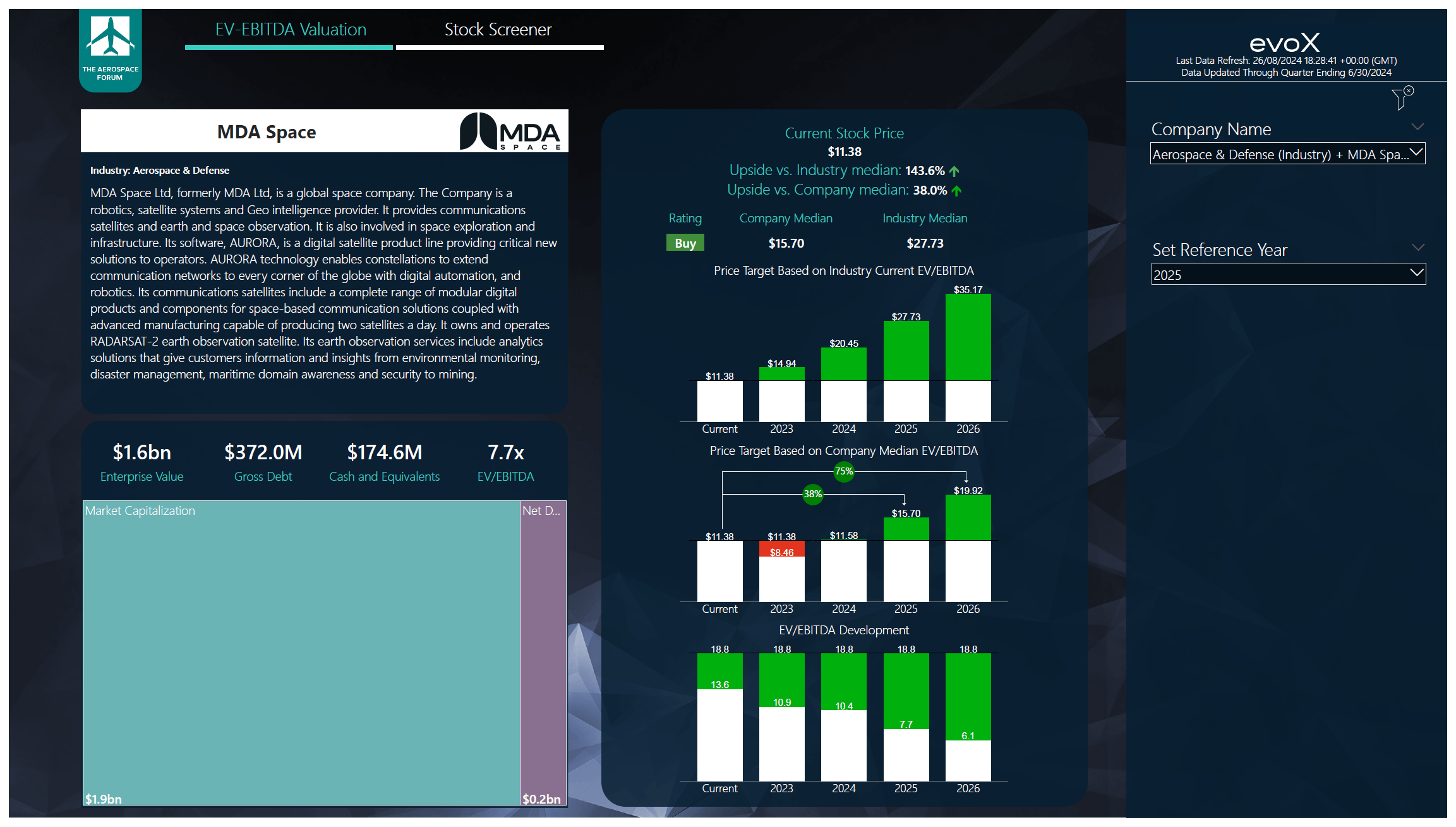

To determine multi-year price targets The Aerospace Forum has developed a stock screener which uses a combination of analyst consensus on EBITDA, CapEx and free cash flow along with the most recent balance sheet data, cash flow statements and my assumptions on debt repayment, share repurchases and dividends. Each quarter, we revisit those assumptions and update accordingly and if need be, we supplement our own estimates if key items such as for example, acquisitions are not reflected in estimates yet. The estimates are not bases on any guidance provided by the companies we cover, but by a strong combination of consensus and my own estimates.

MDA Space had a strong first half of the year and based on that, analyst estimates have gone up by around 3% for EBITDA while free cash flow generation is now expected to be around $100 million USD contrary to earlier expectations of a $21.5 million burn. It shows rather well how the growth that the company is putting on display is good, and in fact stronger than initially expected. With 2024 earnings in mind, the company is about fairly valued against its median EV/EBITDA multiple but has 38% upside to $15.70 USD without factoring any multiple expansion and more upsides towards 2026. The absolute positive is the outlook for positive free cash flow generation. MDA Space has a debt of around CAD $400 million maturing in 2027 and the positive free cash flow allows it to incrementally step down on the debt, thereby reducing interest income and improving its leverage. I continue to believe that the company will either refinance or extend the revolving credit facility, but with free cash flow generation, we also see opportunities to bring the gross debt down.

Conclusion: The Investment Case MDA Space Remains Compelling

Despite some pressures on the EBITDA margins, I believe that MDA Space offers a very compelling investment case. The space market is challenging, but growing, and with decades of experience and an attractive product and services portfolio, MDA Space is positioned well to capitalize while its free cash flow will likely improve its leverage in the years ahead. Consequently, I continue to mark the stock a buy and lift my price target from $13.12 to $15.70.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.